TL;DR:

- A second mortgage is an extra home loan secured against your property without replacing your original loan. It is subordinate to your first mortgage, meaning the primary lender gets paid first if your home is sold. This can help homeowners access equity for large expenses while keeping their existing mortgage terms intact.

A second mortgage is an additional home loan secured against your property while your original mortgage remains in place. It does not replace your primary loan. Instead, it sits alongside it as a separate debt with its own repayment schedule. For New Zealand homeowners who have built up equity in their property, a second mortgage offers a way to access that equity for major expenses or investments without refinancing and losing the terms you already have.

What is a second mortgage and how does it differ from your first?

A second mortgage is subordinate to your first mortgage, meaning the primary lender gets paid first if your property is ever sold under enforcement. This lien position is the defining feature that separates a second mortgage from your original home loan. It shapes everything from the interest rate you are offered to the risk the lender carries.

The key difference from refinancing is equally important to understand. Refinancing replaces your first mortgage with a new one, often at a different rate or term. A second mortgage adds a separate loan on top of your existing one. You end up with two loans, two repayment schedules, and two sets of obligations running at the same time.

This distinction matters for New Zealand homeowners who have locked in a competitive rate on their primary mortgage. Refinancing to access equity could mean breaking that rate and paying break fees. A second mortgage lets you tap your equity while keeping your original loan untouched.

Repayment priority and enforcement

Both repayments must be made each month, and missing either carries serious consequences. If you default and your property is sold, the first mortgage lender is paid in full before the second mortgage lender receives anything. This is why second mortgage lenders price their risk higher and why rates are steeper than your primary loan.

- You carry two separate monthly repayments from the moment the second mortgage settles.

- Default on either loan and both lenders can take action, though the first mortgage lender holds priority.

- The second mortgage lender accepts more risk, which is reflected in their lending criteria and rates.

- A second mortgage is not a cash-out refinance. Confusing the two leads to poor financial decisions.

Pro Tip: Before applying, calculate what both repayments will cost you each month. If the combined figure stretches your budget, a second mortgage may not be the right tool right now.

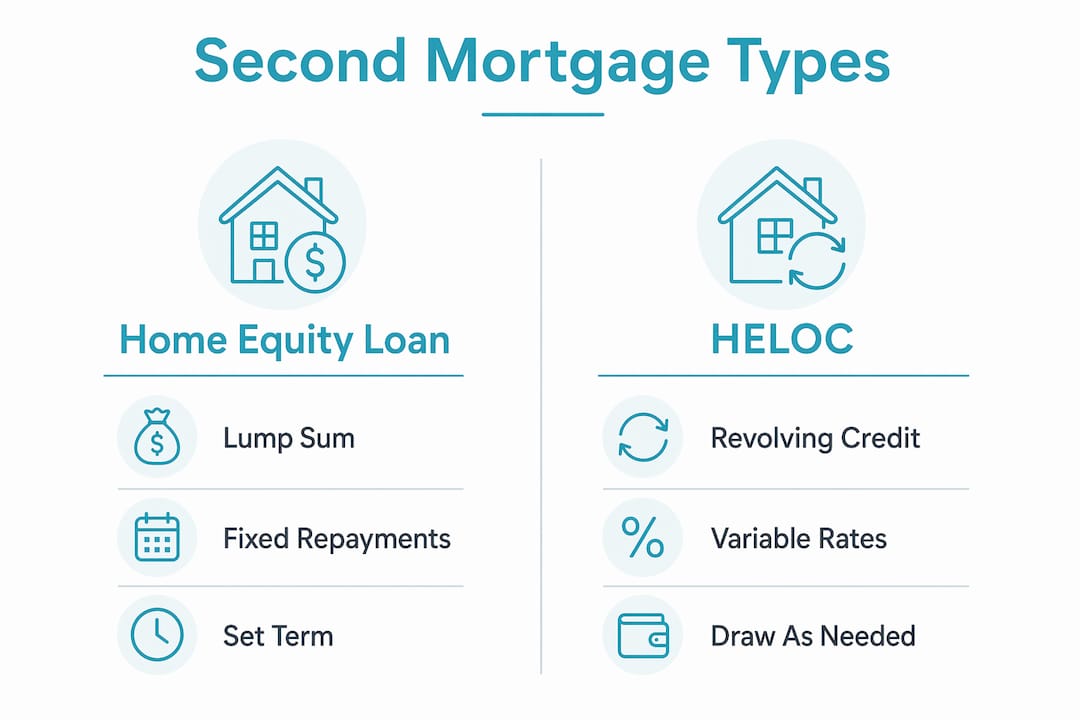

What types of second mortgages are available?

The two main types are home equity loans and home equity lines of credit, commonly called HELOCs. Each suits a different borrowing need, and choosing the wrong one can cost you more than necessary.

A home equity loan delivers a lump sum upfront with fixed repayments over a set term. You know exactly what you owe each month. This suits homeowners funding a single large expense, such as a renovation, a business investment, or consolidating high-interest debt. A HELOC works more like a credit card secured against your home. You draw funds as needed up to an approved limit, repay, and draw again during the draw period. Rates are typically variable, which means your repayments can shift with the market.

Home equity loans offer predictable fixed payments, while HELOCs offer flexible withdrawals at variable rates. The right choice depends on whether you need funds in one go or in stages over time.

| Feature | Home equity loan | HELOC |

|---|---|---|

| Funds delivery | Lump sum upfront | Draw as needed up to limit |

| Interest rate | Fixed | Variable |

| Repayment type | Fixed monthly payments | Varies with balance and rate |

| Best for | Single large expense | Ongoing or staged costs |

| Predictability | High | Lower |

| Risk | Foreclosure if unpaid | Foreclosure if unpaid |

A third option worth knowing about is the piggyback loan, where a second mortgage is taken out at the same time as the first to avoid lenders mortgage insurance. This is a different use case from accessing equity after purchase and is less common in the New Zealand market.

Pro Tip: Choosing between a home equity loan and a HELOC comes down to one question: do you need all the money now, or in stages? Answer that honestly before you apply.

What are the benefits and risks of a second mortgage?

The primary benefit is access to your home equity without disturbing your existing mortgage. For many New Zealand homeowners, this is a significant advantage, particularly if the primary mortgage carries a rate that would be expensive to break. You keep what you have and add what you need.

Common uses for a second mortgage include:

- Home improvements: Renovations that add value to the property and may increase equity further.

- Debt consolidation: Paying off high-interest personal loans or credit card debt at a lower mortgage rate.

- Investment: Funding a business, shares, or a deposit on an investment property.

- Education costs: Covering tuition or training fees for yourself or family members.

- Large one-off expenses: Medical costs, legal fees, or other significant financial events.

The risks are real and should not be minimised. Your home secures the additional loan, which means failure to repay can lead to foreclosure. Carrying two loans increases your total debt and your monthly obligations. If your income drops or your circumstances change, servicing both loans becomes harder. The higher interest rate on a second mortgage also means you pay more over time compared to your primary loan.

Budgeting for dual repayments is not optional. It is the foundation of responsible second mortgage borrowing. Many homeowners focus on what they can access and underestimate what they must repay.

How do you qualify for a second mortgage in New Zealand?

Lenders assess your ability to service both loans, not just the new one. Approval depends more on repayment capacity than on available equity alone. This surprises many homeowners who assume that having equity is enough.

The typical qualification process in New Zealand involves these steps:

- Assess your equity position. Lenders look at your loan-to-value ratio across both mortgages. The more equity you hold, the stronger your application. Reaching 20% equity is a meaningful threshold in the New Zealand market.

- Review your credit history. A clean credit record signals lower risk to lenders. Missed payments or defaults on existing debts will reduce your options.

- Calculate your debt-to-income ratio. Lenders want to see that your total debt obligations, including both mortgages, sit within a manageable range relative to your income.

- Prepare your documentation. Expect to provide recent payslips, bank statements, tax returns if self-employed, and details of all existing debts and assets.

- Demonstrate serviceability. Lenders run stress tests to confirm you can meet repayments if interest rates rise. Your income stability and employment type both factor into this assessment.

Working with a mortgage adviser gives you a clearer picture of where you stand before you apply. Advisers who understand second mortgage lenders in New Zealand can match your profile to the right lender from the outset, saving time and protecting your credit record from unnecessary enquiries.

How do second mortgage rates compare to primary mortgage rates?

Second mortgages carry higher interest rates than first mortgages because the lender takes on greater risk. If the property is sold under enforcement, the second mortgage lender is paid only after the first mortgage is cleared. That subordinate position commands a rate premium.

What this means in practice:

- Fixed rate home equity loans offer repayment certainty but may not benefit if rates fall.

- Variable rate HELOCs can start lower but expose you to rate increases over the draw period.

- The gap between your primary mortgage rate and your second mortgage rate reflects lender risk, not just market conditions.

- Shopping around matters. Different lenders price second mortgage risk differently, and a mortgage adviser can access options you may not find directly.

The total cost of a second mortgage is not just the rate. Establishment fees, legal costs, and valuation fees add to the upfront expense. Factor these into your comparison when weighing a second mortgage against other options like a personal loan or refinancing.

Key takeaways

A second mortgage gives New Zealand homeowners access to home equity without refinancing, but it adds a separate loan, higher rates, and dual repayment obligations that require careful budgeting.

| Point | Details |

|---|---|

| Subordinate lien position | The second mortgage lender is paid only after the first mortgage is cleared in a forced sale. |

| Two loan types available | Home equity loans offer fixed lump sums; HELOCs offer flexible, variable-rate credit lines. |

| Qualification is serviceability-focused | Lenders assess your ability to repay both loans, not just your available equity. |

| Rates are higher than primary mortgages | Greater lender risk means second mortgage rates sit above your primary mortgage rate. |

| Budgeting for dual repayments is non-negotiable | Missing repayments on either loan can lead to foreclosure, as both are secured against your home. |

My honest view on second mortgages after years in NZ mortgage advising

The homeowners who use second mortgages well are the ones who treat them as a tool with a specific job, not as a general source of funds. I have seen clients use a home equity loan to consolidate $60,000 in credit card debt and genuinely improve their financial position. I have also seen clients draw on a HELOC for lifestyle spending and find themselves in a worse position two years later.

The question I always ask is: what is this money doing? If the answer is funding something that builds value, whether that is a renovation, an investment, or clearing expensive debt, a second mortgage can make real sense. If the answer is vague, the risk is real.

One thing that catches people off guard is the rate difference. Homeowners sometimes assume a second mortgage will be priced close to their primary loan. It is not. The subordinate lien position means lenders price in their risk, and that cost compounds over the life of the loan. Running the numbers on total repayment cost, not just monthly repayments, is something I always do with clients before they commit.

My advice is to get clear on your purpose, model both repayment scenarios, and speak with an adviser who knows the New Zealand lender market. Mortgage brokers suggest second mortgages when they genuinely fit the client’s situation, not as a default recommendation. That distinction matters.

— Stuart

How Mortgagemanagers can help you access your home equity

Deciding whether a second mortgage suits your situation takes more than reading about it. It takes a clear view of your equity, your income, your existing loan terms, and the lender options available to you in New Zealand right now.

Mortgagemanagers is a locally owned mortgage advisory business based in Hobsonville, Auckland, with advisers who work with clients across West Auckland, the North Shore, and remotely throughout New Zealand. The team specialises in matching homeowners with the right lender and loan structure for their specific needs, including second mortgages. Whether you are weighing a home equity loan against a HELOC or want to know if you qualify, speaking with a mortgage adviser gives you a tailored answer rather than a general one. Reach out to Mortgagemanagers to get a clear picture of your options.

FAQ

What is a second mortgage in simple terms?

A second mortgage is an additional loan secured against your home that sits behind your primary mortgage. It lets you borrow against your home equity without replacing your existing loan.

How does a second mortgage work with repayments?

You make separate repayments on both your first and second mortgage each month. If you default and your property is sold, the first mortgage lender is paid before the second mortgage lender receives anything.

What is the difference between a home equity loan and a HELOC?

A home equity loan delivers a fixed lump sum with set monthly repayments. A HELOC is a revolving credit line you draw on as needed, typically at a variable interest rate.

Can I get a second mortgage in New Zealand?

Yes, provided you have sufficient home equity and can demonstrate the ability to service both loans. Lenders assess your income, credit history, and debt-to-income ratio, not just your available equity.

Are second mortgage rates higher than primary mortgage rates?

Second mortgage rates are higher because the lender carries greater risk due to their subordinate lien position. Rates may be fixed or variable depending on the loan type you choose.