TL;DR:

- FHA loans are US federal programs not available to New Zealand residents, so borrowers there must seek local options.

- Most lenders require higher credit scores and charge more fees for low-credit applicants, even if FHA guidelines permit lower scores.

FHA loans are defined as US federal mortgage programmes insured by the Federal Housing Administration, and they set the most widely cited credit score thresholds in home lending globally. If you want to apply for FHA loan bad credit situations, the minimum qualifying score is 500, though most lenders impose stricter standards than federal guidelines allow. For New Zealand borrowers, this distinction matters enormously. FHA loans are not available to NZ residents, so understanding the framework helps you recognise what local bad credit home loans should look like and what standards to hold lenders to.

What credit scores and down payments do you need to apply for FHA loans with bad credit?

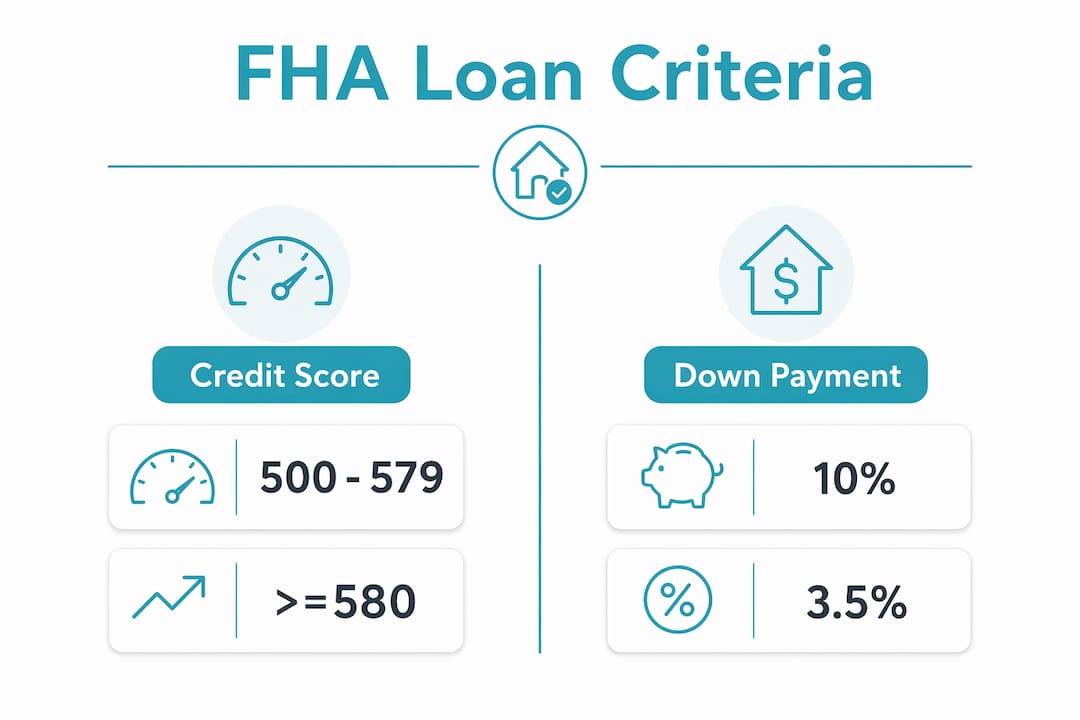

The FHA sets two distinct credit score tiers, and each carries a different down payment requirement. Borrowers with scores between 500 and 579 must put down at least 10%. Those with scores of 580 or above qualify for the 3.5% minimum down payment. Applicants below 500 are ineligible under current FHA guidelines entirely.

The gap between FHA rules and real lender behaviour is where most borrowers get caught out. Most lenders impose overlays requiring minimum scores of 580 to 620, even though FHA technically allows down to 500. Lenders avoid manual underwriting when possible because it costs more and takes longer. This means a score of 510 may technically qualify under FHA rules but still get rejected by nearly every participating lender.

Cost is the other factor that catches borrowers off guard. Less than 4% of borrowers with credit scores below 620 secured mortgage loans in 2025. Those who did succeed paid higher origination fees of 0.5%–1% of the loan amount, plus underwriting fees of $500–$1,000 or more. That cost premium is not a penalty. It reflects the genuine risk lenders carry when approving low credit applicants.

Your debt-to-income ratio matters just as much as your credit score. FHA guidelines assess your total monthly debt against your gross monthly income, and applicants with foreclosure within the last 3 years are automatically excluded. Recent payment history carries significant weight too. A score of 580 with 12 months of clean payments looks very different to a lender than a score of 600 with a default six months ago.

- Credit score 500–579: Minimum 10% down payment required

- Credit score 580 and above: Minimum 3.5% down payment required

- Credit score below 500: Ineligible under FHA guidelines

- Lender overlays: Most require 580–620 regardless of FHA minimums

- Debt-to-income ratio: Assessed alongside credit score for full picture

- Recent defaults or foreclosure: Can disqualify even borderline-eligible applicants

Pro Tip: Check your credit report from all three major bureaus before approaching any lender. Errors on credit files are common and correcting even one inaccuracy can shift your score enough to move you into a better lending tier.

How to prepare and apply for an FHA loan with bad credit

Preparation separates approved applicants from rejected ones. Lenders reviewing bad credit mortgage options want to see a complete, honest financial picture. Gaps in documentation or inconsistencies between stated income and bank statements raise red flags that no credit score can overcome.

-

Gather your core documents first. Collect two years of tax returns, recent payslips, three months of bank statements, and your full credit report. Employment history matters too. Lenders want to see stable, continuous income rather than frequent job changes.

-

Get preapproval from multiple lenders. A single rejection does not define your options. Working with multiple lenders or advisers consistently produces better outcomes than accepting the first offer. Credit score alone is insufficient to guarantee approval. Lenders weigh income, reserves, and debt ratios together.

-

Understand manual underwriting before you apply. If your credit score is low or your debt-to-income ratio is high, manual underwriting is triggered. This process requires 12–24 months of rental history, written explanations for any credit blemishes, and detailed documentation of all income sources. It results in slower approvals than automated underwriting, so build extra time into your plans.

-

Demonstrate recent positive payment behaviour. Lenders reviewing bad credit applications look for signs of recovery. Six to twelve months of on-time payments on existing debts signals that your credit challenges are in the past, not the present. This single factor can shift a lender’s decision more than a marginal score improvement.

-

Write clear credit explanations. For every negative item on your credit file, prepare a brief, factual written explanation. Medical debt, redundancy, or relationship breakdown are all understandable circumstances. Lenders respond better to honest context than to unexplained gaps.

Pro Tip: If you are working toward rebuilding your credit before applying, focus on reducing credit card balances below 30% of their limits. This single action often produces the fastest score improvement.

Common pitfalls to avoid when applying with bad credit

The biggest risk for borrowers with poor credit is not rejection. The biggest risk is accepting a loan that makes your financial situation worse. Mortgage experts warn that rushing to apply with bad credit often leads to high interest rates and elevated default risk. Waiting to improve your credit first frequently produces better financing terms than quick approval on a costly product.

“Improving credit before applying is often wiser than accepting the first approval you receive. The cost difference over a 30-year loan can be tens of thousands of dollars.”

Watch for these specific traps:

- Guaranteed approval offers: These are frequently scams or predatory products that worsen your credit situation. No legitimate lender guarantees approval before reviewing your full financial profile.

- Multiple credit applications in a short period: Each hard inquiry reduces your score slightly. Cluster your lender comparisons within a 14-day window so credit bureaus treat them as a single inquiry.

- Ignoring lender overlays: Always ask a lender directly what their minimum credit score requirement is, not just what FHA allows. The gap between the two can cost you a wasted application and an unnecessary hard inquiry.

- Underestimating total loan costs: Origination fees, mortgage insurance premiums, and higher interest rates all compound over the life of a loan. Request a full loan estimate and compare the total cost, not just the monthly repayment.

- Incomplete or inconsistent disclosure: Lenders verify everything. Overstating income or omitting debts creates legal risk and guarantees rejection once the discrepancy surfaces.

Reading a bad credit loan mistakes guide before you approach any lender is time well spent. The mistakes most borrowers make are predictable and avoidable with the right preparation.

What are the alternatives to FHA loans for New Zealand borrowers with bad credit?

FHA loans are a US federal programme. They are not available to New Zealand residents under any circumstances. NZ borrowers must work within the local lending market, which has its own set of options for those with impaired credit histories.

The NZ home loan market divides broadly into two categories for bad credit borrowers.

| Loan type | Key features |

|---|---|

| Major bank home loans | Stricter credit criteria, lower interest rates, require clean credit history |

| Non-bank lenders | More flexible credit assessment, higher interest rates, shorter loan terms |

| First Home Grant (Kāinga Ora) | Government grant for eligible first home buyers, income and property price caps apply |

| Low deposit home loans | Available through some lenders with as little as 5%–10% deposit, subject to credit assessment |

| Mortgage adviser access | Advisers access multiple lenders simultaneously, including non-bank options not available directly |

Non-bank lenders fill the gap that major banks leave for borrowers with defaults, missed payments, or limited credit history. They assess applications more flexibly, but this flexibility comes at a cost. Interest rates from non-bank lenders are typically higher, and loan terms are often shorter, which means you should treat them as a stepping stone rather than a permanent solution.

The First Home Grant through Kāinga Ora provides eligible buyers with financial assistance toward a deposit. Income caps and property price limits apply, and your credit history still factors into the overall application. Working with a mortgage adviser gives you access to the full picture of what you qualify for across both bank and non-bank options.

Improving your credit score before applying remains the most effective way to access better terms. Practical steps include paying down existing debt, correcting errors on your credit file, and avoiding new credit applications in the months before you apply. A guide on improving your credit score can help you build a realistic timeline. Even a modest score improvement can shift you from non-bank to bank lending territory, saving thousands over the life of your loan.

Key takeaways

Borrowers with bad credit can access home loans in New Zealand, but success requires understanding lender requirements, preparing thorough documentation, and choosing the right loan type for your credit profile.

| Point | Details |

|---|---|

| FHA loans are US-only | New Zealand borrowers cannot access FHA loans and must use local bank or non-bank lenders. |

| Credit score tiers matter | FHA requires 500 minimum with 10% down, or 580 with 3.5% down, but most lenders require 580–620. |

| Manual underwriting adds time | Low credit or high debt triggers manual review requiring 12–24 months of documentation. |

| Predatory offers are a real risk | Guaranteed approval claims are a warning sign of scams or high-cost products that worsen credit. |

| Advisers improve your options | Working with a mortgage adviser gives you access to multiple lenders and better loan matching. |

What I have learned from years of bad credit mortgage cases

The borrowers who succeed with bad credit applications share one trait. They treat the process as a preparation project, not a speed race. Every client I have worked with who rushed into the first approval they received ended up paying more than necessary, sometimes significantly more over the life of their loan.

The uncomfortable truth about bad credit home loans in New Zealand is that the market rewards patience. A borrower who spends six months fixing their credit before buying often qualifies for a bank loan at standard rates. The borrower who applies immediately with a poor score frequently ends up with a non-bank loan at a higher rate, which stretches their budget and leaves less room for error.

I have also seen borrowers make the mistake of assuming that a mortgage adviser is only useful once their credit is clean. The opposite is true. Getting advice early, before you apply anywhere, gives you a clear picture of where you stand, what lenders are likely to approve you, and what specific steps will move the needle fastest. That early conversation often saves months of wasted effort and unnecessary credit inquiries.

The NZ lending market is more nuanced than most borrowers realise. Non-bank lenders are not a last resort. For the right borrower at the right moment, they are a practical bridge to homeownership while credit improves. The key is knowing which lender suits your exact profile, and that is where expert advice earns its value.

— Stuart

How Mortgagemanagers helps NZ borrowers with bad credit

Mortgagemanagers works with New Zealanders across a wide range of credit situations, including those who have been declined by major banks or are carrying defaults and missed payments on their record.

As mortgage advisers based in Hobsonville, Auckland, the Mortgagemanagers team accesses both bank and non-bank lenders to find the loan that fits your actual financial situation, not just your credit score. Whether you need help understanding your current options, preparing your application, or building a credit improvement plan before you apply, the team provides clear, honest guidance at every step. Reach out to Mortgagemanagers to get a realistic picture of what is possible for you right now.

FAQ

Can you get an FHA loan with bad credit in New Zealand?

FHA loans are a US federal programme and are not available to New Zealand residents. NZ borrowers with bad credit must use local bank or non-bank lenders instead.

What is the minimum credit score to apply for an FHA loan?

The FHA minimum credit score is 500 with a 10% down payment, or 580 with a 3.5% down payment. Most participating lenders require 580–620 due to their own internal standards.

What documents do you need for a bad credit home loan application?

Lenders typically require two years of tax returns, recent payslips, three months of bank statements, and written explanations for any negative credit items. Manual underwriting may also require 12–24 months of rental history.

How do I improve my chances of getting a bad credit home loan in NZ?

Pay down existing debts, correct errors on your credit file, maintain six to twelve months of clean payment history, and work with a mortgage adviser who can match you to lenders suited to your profile.

Are guaranteed approval home loans legitimate?

Guaranteed approval offers are a warning sign. Legitimate lenders always assess your full financial profile before approving any loan. Offers that promise approval without a credit check are frequently scams or high-cost products that worsen your financial position.