Most first home buyers in Hobsonville discover that over 60 percent of australian applicants with limited credit history face strict lending criteria in Auckland. Understanding how your credit score shapes the home loan process can make the difference between securing your dream house or staying stuck in rental cycles. This guide reveals practical steps and common pitfalls, helping you take control of your financial reputation so lenders view you as a reliable borrower.

Table of Contents

- What Is A Credit Score In Home Loans

- How Lenders Assess Credit In New Zealand

- Requirements And Minimum Scores For First Home Buyers

- Common Credit Mistakes And Their Consequences

- Steps To Improve Your Credit Score Fast

Key Takeaways

| Point | Details |

|---|---|

| Credit Score Importance | A credit score is crucial for home loan approvals and influences interest rates offered by lenders. Scores above 700 are generally viewed as excellent. |

| Lender Evaluation Process | Lenders in New Zealand assess credit through comprehensive evaluations of financial history, income, and employment stability before determining loan eligibility. |

| Common Credit Mistakes | First home buyers should avoid missed payments and high credit card balances, as these can lead to increased interest rates and difficulty in securing loans. |

| Improving Your Credit Score | To boost your credit score quickly, make timely payments, keep credit card balances low, and regularly check credit reports for inaccuracies. |

What Is A Credit Score In Home Loans

A credit score represents a numerical rating that financial institutions use to evaluate your potential reliability as a borrower, particularly when you’re seeking a home loan. This three-digit number summarises your entire financial history, distilling years of financial behaviour into a single, powerful indicator that lenders use to assess risk.

In the Australian context, your credit score is calculated based on various financial activities, including payment history for debts and loans. Credit reporting agencies like Centrix, Equifax, and Illion compile detailed reports tracking everything from mortgage repayments to credit card transactions. These reports capture both positive and negative financial behaviours, meaning consistently paying bills on time can boost your score, while missed payments or defaults can significantly damage your rating.

The typical credit score ranges from zero to 1200, with higher numbers indicating lower lending risk. Lenders use this score to determine not just whether they’ll approve your home loan, but also the interest rates and terms they’ll offer. A score above 700 is generally considered excellent, potentially unlocking more favourable borrowing conditions. Conversely, a low score might result in higher interest rates or even loan rejection.

Pro tip: Request a free credit report annually and review it carefully to identify and correct any potential errors that could negatively impact your home loan application.

How Lenders Assess Credit In New Zealand

Lenders in New Zealand employ a comprehensive approach to assessing credit, focusing on multiple dimensions of a borrower’s financial profile. Regulatory requirements under the Credit Contracts and Consumer Finance Act mandate that financial institutions conduct thorough evaluations to ensure responsible lending practices and protect consumers from potential financial hardship.

The credit assessment process involves several critical components. Lenders meticulously review an applicant’s credit history, income stability, existing debt levels, and overall financial capacity. They analyse credit reports from major agencies, examining patterns of past financial behaviour including payment consistency, outstanding debts, and any previous defaults. Income verification plays a crucial role, with lenders calculating debt-to-income ratios to determine whether a borrower can comfortably manage additional financial obligations.

Beyond numerical metrics, New Zealand lenders also consider contextual factors that provide deeper insights into an individual’s financial reliability. This might include employment stability, length of current residence, and evidence of consistent savings behaviour. The goal is to build a holistic understanding of the borrower’s financial responsibility, moving beyond simplistic credit score calculations to make nuanced lending decisions that balance risk management with fair assessment.

Below is a quick guide comparing how lenders in New Zealand assess key areas when evaluating home loan applications:

| Assessment Factor | Why It Matters | Typical Evidence Required |

|---|---|---|

| Credit history | Reflects repayment reliability | Recent credit report, bill statements |

| Income stability | Ensures regular loan repayment | Payslips, tax returns |

| Debt-to-income ratio | Assesses risk of over-borrowing | List of current debts, income details |

| Employment status | Shows earning consistency | Employment contract, reference letter |

Pro tip: Prepare a comprehensive financial portfolio before applying for a home loan, including proof of income, consistent savings records, and a clear explanation of any past credit challenges.

Requirements And Minimum Scores For First Home Buyers

First home buyers in New Zealand face specific credit and financial requirements that can seem complex but are essential to understand. Government initiatives like the First Home Loan program offer pathways to homeownership with more flexible entry requirements. Typically, buyers must be New Zealand citizens or permanent residents, with income restrictions varying based on individual circumstances.

While there’s no universal minimum credit score, lenders assess creditworthiness through multiple dimensions. Most financial institutions look for credit scores above 650, though this can vary. Key criteria include consistent income, stable employment history, and a demonstrated ability to manage existing financial obligations. First home buyers should aim to maintain a clean credit history, showing regular bill payments, minimal outstanding debts, and responsible financial management.

Specific eligibility requirements often include income caps that differ based on household composition. For single buyers without dependants, the typical income threshold is around $95,000, while combined household incomes for multiple buyers can reach $150,000. Lenders will also scrutinise debt-to-income ratios, typically preferring applicants whose total monthly debt payments do not exceed 40% of their gross monthly income. This ensures borrowers can comfortably manage mortgage repayments without financial strain.

Pro tip: Start building a strong credit history at least 12 months before applying for a home loan by maintaining a consistent record of on-time bill payments and keeping credit card balances low.

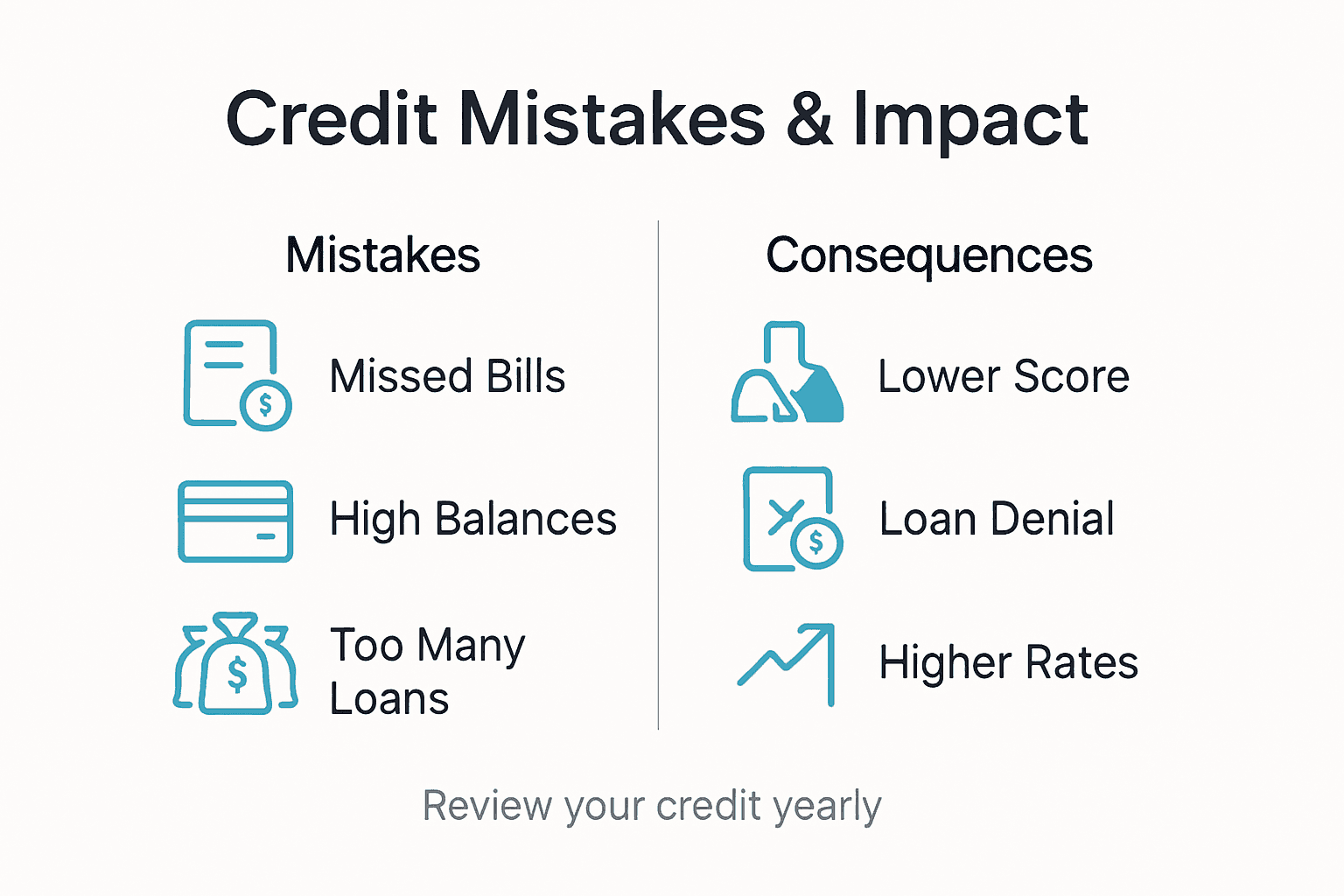

Common Credit Mistakes And Their Consequences

First home buyers often make critical credit mistakes that can significantly impact their long-term financial prospects. Government research highlights several key errors that can derail home loan applications, with missed bill payments and unmanaged debt standing out as primary culprits. These seemingly minor oversights can create lasting challenges in securing affordable financing.

Multiple financial missteps can trigger severe consequences for potential homeowners. Accumulating high credit card balances, frequently applying for new credit, and failing to maintain consistent payment histories can dramatically reduce credit scores. Each late payment potentially drops credit ratings by 50-100 points, making lenders view applicants as high-risk. Moreover, defaults or bankruptcy records can remain on credit files for up to seven years, creating substantial barriers to obtaining home loans or securing competitive interest rates.

The most damaging credit mistakes include ignoring bill notifications, defaulting on existing loans, and maxing out credit limits. Lenders meticulously examine an applicant’s financial behaviour, treating each missed payment as a red flag. Unexpected financial challenges can quickly escalate into long-term credit problems, with debt collection actions potentially leading to legal judgments that further compromise credit standings. First home buyers must proactively manage their financial reputation, understanding that every financial decision carries potential long-term implications.

Here is a summary of common credit mistakes and their potential long-term consequences:

| Credit Mistake | Immediate Impact | Long-Term Consequence |

|---|---|---|

| Missed bill payments | Score drops 50-100 points | Difficult loan approval |

| High credit card balances | Increased risk profile | Higher interest rates |

| Multiple credit applications | Temporary score decrease | Seen as risky behaviour |

| Bankruptcy/defaults | Record stays up to 7 years | Limited borrowing options |

Pro tip: Obtain a free credit report annually and review it thoroughly, addressing any errors or discrepancies immediately to maintain a clean financial record.

Steps To Improve Your Credit Score Fast

Improving your credit score requires strategic and consistent financial management. Government guidelines recommend a systematic approach to credit repair that focuses on creating positive financial habits and addressing potential errors in your credit history. Understanding the nuanced factors that influence your credit rating is the first critical step towards meaningful improvement.

The most effective strategies involve multiple targeted actions. Prioritise making all bill and loan repayments consistently and on time, as payment history represents the most significant factor in credit score calculations. Reducing credit card balances to below 30% of your credit limit can dramatically improve your score. Additionally, avoid opening multiple new credit accounts in quick succession, as each application generates a hard inquiry that can temporarily lower your credit rating.

Careful credit management also involves proactive monitoring and dispute resolution. Request free credit reports from major New Zealand agencies like Centrix, Equifax, and illion at least annually. Meticulously review these reports for any inaccuracies, such as incorrect personal information, unrecognised accounts, or outdated negative entries. Promptly dispute any errors with the relevant credit reporting agency, providing supporting documentation to substantiate your claim. This approach not only helps clean up your credit file but also demonstrates responsible financial behaviour to potential lenders.

Pro tip: Set up automatic bill payments and calendar reminders to ensure you never miss a payment deadline, which can help maintain a consistently strong credit profile.

Take Control of Your Home Loan Journey with Expert Mortgage Advice

Understanding the impact of your credit score on securing a home loan is crucial, especially for first home buyers facing the challenges of meeting minimum credit requirements and avoiding common credit mistakes. If you feel overwhelmed by managing your credit history, income stability, and debt-to-income ratios it is essential to get tailored guidance that simplifies these complex factors.

At Mortgage Managers, based in Hobsonville, our experienced Auckland mortgage advisers specialise in helping you navigate the lending criteria used by New Zealand lenders. We focus on empowering you to improve your credit profile and present your financial situation in the best possible light so you can access competitive home loan options.

Get personalised support to build a strong credit record and secure your first home with confidence Visit Mortgage Managers today to start your journey Our team is ready to help you prepare a comprehensive application that meets lending requirements and keeps you informed every step of the way Learn more about credit score tips and home loan strategies and take the first step towards your dream home now

Frequently Asked Questions

What is a credit score and how does it impact home loans?

A credit score is a three-digit number that represents your financial reliability as a borrower. It affects home loan approvals, interest rates, and terms offered by lenders; higher scores usually lead to better borrowing conditions.

How can first home buyers improve their credit score quickly?

First home buyers can improve their credit score by consistently making on-time bill payments, reducing credit card balances to below 30% of their limits, and avoiding multiple credit applications in a short timeframe.

What common credit mistakes should first home buyers avoid?

Common credit mistakes include missing bill payments, accumulating high credit card balances, applying for multiple credit accounts at once, and having defaults or bankruptcies on record. These can significantly lower credit scores and hinder loan approval.

What are the typical credit score requirements for first home buyers?

While there is no universal minimum credit score, most lenders prefer scores above 650 for first home buyers. Key criteria also include stable income, employment history, and managing existing financial obligations responsibly.