TL;DR:

- A second mortgage is a secured loan using your home equity as collateral, allowing access to funds without refinancing your first mortgage. Approval depends on meeting criteria such as 80% LVR, a credit score above 620, and manageable debt-to-income ratios, with proper documentation speeding up the process. Choosing between lump-sum loans, revolving credit, or top-ups depends on your project purpose, and working with a mortgage adviser can simplify application and secure the best solution.

A second mortgage is a secured loan that uses your existing home equity as collateral while your first mortgage remains active. For New Zealand homeowners, this means you can access funds for renovations, investment properties, or debt consolidation without selling your home or refinancing your entire loan. The process requires meeting specific criteria around equity, credit, and income, and understanding the local lending context makes the difference between a smooth approval and a frustrating knockback. This guide walks you through every stage, from qualifying requirements to the full application process.

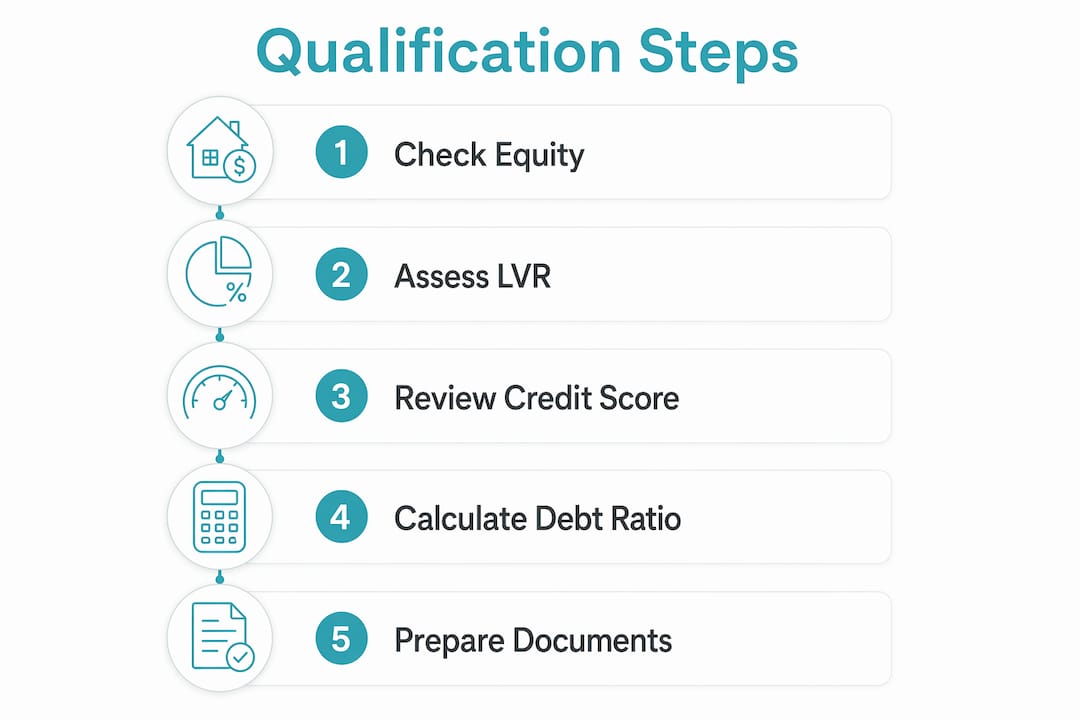

How to get a 2nd mortgage: what you need to qualify

Before you apply, your lender will assess several financial factors. Meeting these criteria upfront saves you time and protects your credit file from unnecessary enquiries.

Equity and loan-to-value ratio (LVR)

Most lenders cap total borrowing at 80% of your property’s value across both loans combined. So if your home is worth $900,000 and you owe $500,000 on your first mortgage, your maximum combined borrowing is $720,000, leaving you with $220,000 of potential equity to access. Lenders typically require a minimum 15% to 20% equity buffer to remain after both loans are settled. Two borrowers with similarly valued homes can access very different amounts depending on their existing loan balances and lender-specific LVR caps, which is why calculating your usable equity precisely matters.

Credit score and debt-to-income ratio

A minimum credit score of 620 is the typical threshold, though many lenders prefer scores above 700 to offer competitive rates. Your debt-to-income (DTI) ratio must generally sit below 43%, and some NZ lenders apply stricter serviceability stress tests on top of that. Because second mortgages carry higher risk for lenders due to their subordinate position behind the first mortgage, approval criteria tend to be tighter than for primary loans.

Income and documentation

Stable, verifiable income is non-negotiable. Lenders want to see payslips, tax returns, or financial statements for the self-employed, along with proof of existing debts and assets. NZ banks, specialist lenders, and mortgage brokers each assess these documents differently, so knowing which lender suits your profile is worth researching before you apply. Understanding NZ bank approval criteria can help you target the right institution from the start.

- Home equity must support combined LVR of 80% or less

- Credit score of 620 minimum, with 700+ preferred for best rates

- DTI ratio below 43%, subject to NZ serviceability stress tests

- Stable income with full documentation: payslips, tax returns, bank statements

- Existing mortgage statements and property valuation may be required

Pro Tip: Pull your credit report from Equifax or Centrix before applying and dispute any errors. A single incorrect default can drop your score enough to push you into a higher interest rate tier or trigger a decline.

Step-by-step: how to apply for a second mortgage

The second mortgage process involves equity calculation, document preparation, lender comparison, formal application, appraisal, underwriting, and settlement. In New Zealand, this typically takes two to four weeks from application to funding, though complex cases can run longer.

-

Calculate your usable equity. Subtract your current mortgage balance from 80% of your property’s estimated value. This gives you the maximum you can borrow before factoring in lender-specific minimums. Use a registered valuation for accuracy rather than an online estimate.

-

Gather your financial documents. Collect your last three months of payslips or two years of tax returns if self-employed, your most recent mortgage statement, bank statements for the past three months, a list of all debts and liabilities, and a valid form of ID. If your purpose is renovation, detailed project documentation such as builder quotes and plans can significantly speed up approval.

-

Compare lenders and loan products. NZ banks, credit unions, and non-bank lenders each have different criteria and products. Mortgage brokers can access a wider panel of lenders and often identify options you would not find independently. Compare interest rates, fees, loan terms, and repayment flexibility before committing.

-

Submit your application. Most major NZ banks accept applications online or in-branch. Non-bank lenders often work through brokers. Be thorough and accurate. Incomplete applications are the most common cause of delays, and well-prepared documentation directly reduces processing time.

-

Attend the property appraisal. Your lender will order a registered valuation to confirm your property’s current market value. This is the figure used to calculate your LVR, so the outcome directly affects how much you can borrow.

-

Navigate underwriting. The lender’s credit team reviews all documentation, verifies income, and assesses serviceability. They may request additional information such as a letter of explanation for a credit enquiry or updated bank statements. Respond promptly to keep the process moving.

-

Settle the loan. Once approved, you will receive a loan offer and disclosure documents to review and sign. Settlement typically follows within a few business days. Funds are either deposited directly or drawn down as needed depending on the loan type.

Pro Tip: Assign one person at your brokerage or bank as your point of contact and check in every two to three business days during underwriting. Proactive communication cuts average processing time noticeably.

What are the types of second mortgages available in New Zealand?

Choosing the right loan type affects your repayment flexibility, interest costs, and cashflow, making product selection one of the most consequential decisions in the process.

A home equity loan delivers a lump sum at a fixed interest rate, repaid over a set term. This suits defined projects like a kitchen renovation or a deposit on an investment property, where you know the total cost upfront. A revolving credit mortgage (the NZ equivalent of a HELOC) works like an overdraft secured against your home. You draw funds as needed and pay interest only on what you use. This suits ongoing cash needs or staged renovation projects. Understanding the difference between these products is covered in detail in this revolving credit mortgage guide.

In New Zealand, mortgage top-ups are the most common alternative to a registered second mortgage. A top-up increases your existing loan balance with your current lender and requires a fresh serviceability assessment, still subject to the 80% LVR limit. Many NZ homeowners find top-ups simpler because they avoid the consent and legal costs of registering a separate second mortgage. For those whose first lender will not consent, some NZ non-bank lenders use caveats instead of registered mortgages, which sidesteps the consent requirement entirely.

| Feature | Home equity loan | Revolving credit mortgage |

|---|---|---|

| Disbursement | Lump sum | Draw down as needed |

| Interest rate | Fixed | Variable |

| Repayment structure | Fixed instalments | Flexible, interest-only option |

| Best suited for | Defined projects, debt consolidation | Staged renovations, ongoing cash needs |

| Interest cost | Predictable | Lower if managed well |

What mistakes should you avoid when getting a second mortgage?

Many applications fail or result in poor outcomes not because of bad credit, but because of avoidable errors in preparation and product selection.

Overestimating your equity. Online property estimates can be 10% to 15% off the registered valuation figure lenders actually use. Basing your borrowing expectations on an inflated estimate leads to disappointment at appraisal. Always use a conservative figure and confirm with a professional valuation early.

Ignoring the serviceability stress test. NZ lenders assess your ability to repay at rates higher than the current market rate, typically 2% to 3% above the loan rate. If your combined debt repayments consume too large a share of your income at the stressed rate, you will not qualify regardless of your equity position. Second mortgage approval rates hinge on equity and DTI more than credit score alone, and many denials come down to excess existing debt rather than poor credit history.

Choosing the wrong loan structure. A lump-sum loan for a staged renovation project means paying interest on the full amount from day one, even if you spend the funds over twelve months. A revolving credit facility in that scenario saves meaningful interest. Conversely, a revolving credit line for a one-off debt consolidation can tempt re-borrowing and undermine the original purpose. Align the structure with the purpose.

- Do not apply with multiple lenders simultaneously. Each credit enquiry affects your score.

- Do not omit debts from your application. Lenders verify independently and undisclosed liabilities trigger declines.

- Do not skip professional advice when your situation is complex, such as self-employment, multiple properties, or existing defaults.

- Do not assume your current bank will offer the best rate. Non-bank lenders and specialist lenders often provide more flexibility.

Pro Tip: If your main bank declines your application, ask specifically why before approaching another lender. A mortgage broker can then target lenders whose criteria match your actual profile rather than applying broadly and accumulating credit enquiries.

Exploring your home loan top-up options before committing to a full second mortgage registration can also save you legal fees and processing time.

Key takeaways

Getting a second mortgage in New Zealand requires sufficient home equity within an 80% combined LVR, a credit score above 620, a manageable DTI ratio, and a well-prepared application matched to the right loan product.

| Point | Details |

|---|---|

| Equity is the foundation | Calculate usable equity using 80% LVR minus your existing mortgage balance before applying. |

| Credit and DTI both matter | A score above 620 and DTI below 43% are the minimum thresholds most lenders apply. |

| Match product to purpose | Use a lump-sum loan for defined costs and a revolving credit facility for staged or ongoing needs. |

| Top-ups are often simpler | NZ mortgage top-ups avoid second mortgage registration costs and are the most common local approach. |

| Preparation speeds approval | Complete documentation, including project plans or debt schedules, reduces underwriting delays significantly. |

What I have learned about second mortgages after years in NZ lending

Over the years working with Auckland homeowners and clients across New Zealand, I have noticed a consistent pattern: the people who struggle most with second mortgage applications are not those with the weakest finances. They are the ones who arrive without a clear picture of their equity position or a defined purpose for the funds.

Lenders have tightened their criteria noticeably since 2022. The 80% LVR cap is applied more strictly, and serviceability stress tests have become more demanding as interest rates shifted. What worked three years ago does not always work today. I have seen clients with strong credit scores declined because their combined debt repayments, when stress-tested, exceeded the lender’s threshold by a small margin.

My honest observation is that renovation-driven applications tend to fare better when the borrower presents a builder’s quote and a staged drawdown plan. It signals to the lender that the funds have a defined purpose and a clear exit. Vague applications for “general purposes” attract more scrutiny and slower processing.

The trend toward mortgage top-ups over registered second mortgages is real and practical for most NZ homeowners. The legal costs and consent requirements of a registered second mortgage add friction that a top-up avoids entirely, provided your existing lender will approve it. When they will not, non-bank lenders using caveats as alternative security are worth exploring through a broker who knows that market well.

My recommendation is always to start with a clear equity calculation, match your loan structure to your actual cashflow needs, and talk to a mortgage adviser before you approach any lender directly. The right preparation makes the process far less stressful than most people expect.

— Stuart

How Mortgagemanagers can help you secure your second mortgage

Accessing a second mortgage is straightforward when you have the right guidance from the start.

Mortgagemanagers is a locally owned Auckland-based team of mortgage advisers who specialise in helping New Zealand homeowners assess their equity, match their profile to the right lender, and manage the full application process. With access to a wide panel of banks and specialist lenders, including non-bank options for complex situations, the team can find solutions that a single bank simply cannot offer. Whether you are funding a renovation, consolidating debt, or building an investment portfolio, Mortgagemanagers handles the documentation, lender negotiations, and follow-up so you can focus on what matters. Reach out to the team at Mortgagemanagers for a no-obligation conversation about your options.

FAQ

What is a second mortgage?

A second mortgage is a secured loan registered against your property behind your existing first mortgage, allowing you to borrow against your accumulated home equity. It is separate from a mortgage top-up, which increases your existing loan balance with the same lender.

How much equity do I need to qualify for a second mortgage?

Most lenders require your combined loans to remain within 80% of your property’s value, with a minimum 15% to 20% equity buffer retained after both loans are accounted for.

What credit score do I need for a second mortgage in New Zealand?

The typical minimum credit score is 620, though lenders prefer scores above 700 for the most competitive interest rates. Your DTI ratio and income stability carry equal weight in the assessment.

How long does the second mortgage application process take?

The process from application to settlement typically takes two to four weeks in New Zealand, provided your documentation is complete and the property appraisal proceeds without complications.

Can I get a second mortgage if my bank says no?

Yes. Non-bank lenders and specialist lenders in New Zealand offer second mortgage products, and some use caveats as alternative security rather than a registered mortgage, which removes the need for your first lender’s consent.