Struggling to keep up with rising mortgage payments is a reality for many first home buyers in Hobsonville, Auckland. As living costs climb and monthly repayments jump by $200 to $600 for some households, the pressure can feel overwhelming. For local families, this financial strain means tough choices and constant worry. Discover practical steps and proven options that can help you manage mortgage stress and secure a more affordable path to homeownership.

Table of Contents

- Mortgage Stress Defined For New Zealanders

- How Mortgage Stress Manifests In Auckland

- Major Causes: High Costs And Refixing Rates

- Who Is Most At Risk In Hobsonville

- Strategies To Manage Or Reduce Mortgage Stress

Key Takeaways

| Point | Details |

|---|---|

| Mortgage Stress Impact | Many New Zealand households experience significant financial pressure, with mortgage payments consuming over 30% of pre-tax income. |

| Auckland Mortgage Challenges | Homeowners face unexpected payment increases due to mortgage refix shock, adding significant strain to budgets. |

| Vulnerable Demographics | Young professionals, first-time buyers, and Māori communities are particularly at risk of mortgage stress in Hobsonville. |

| Financial Management Strategies | Developing robust budgeting techniques and exploring refinancing options can help mitigate mortgage stress effectively. |

Mortgage Stress Defined For New Zealanders

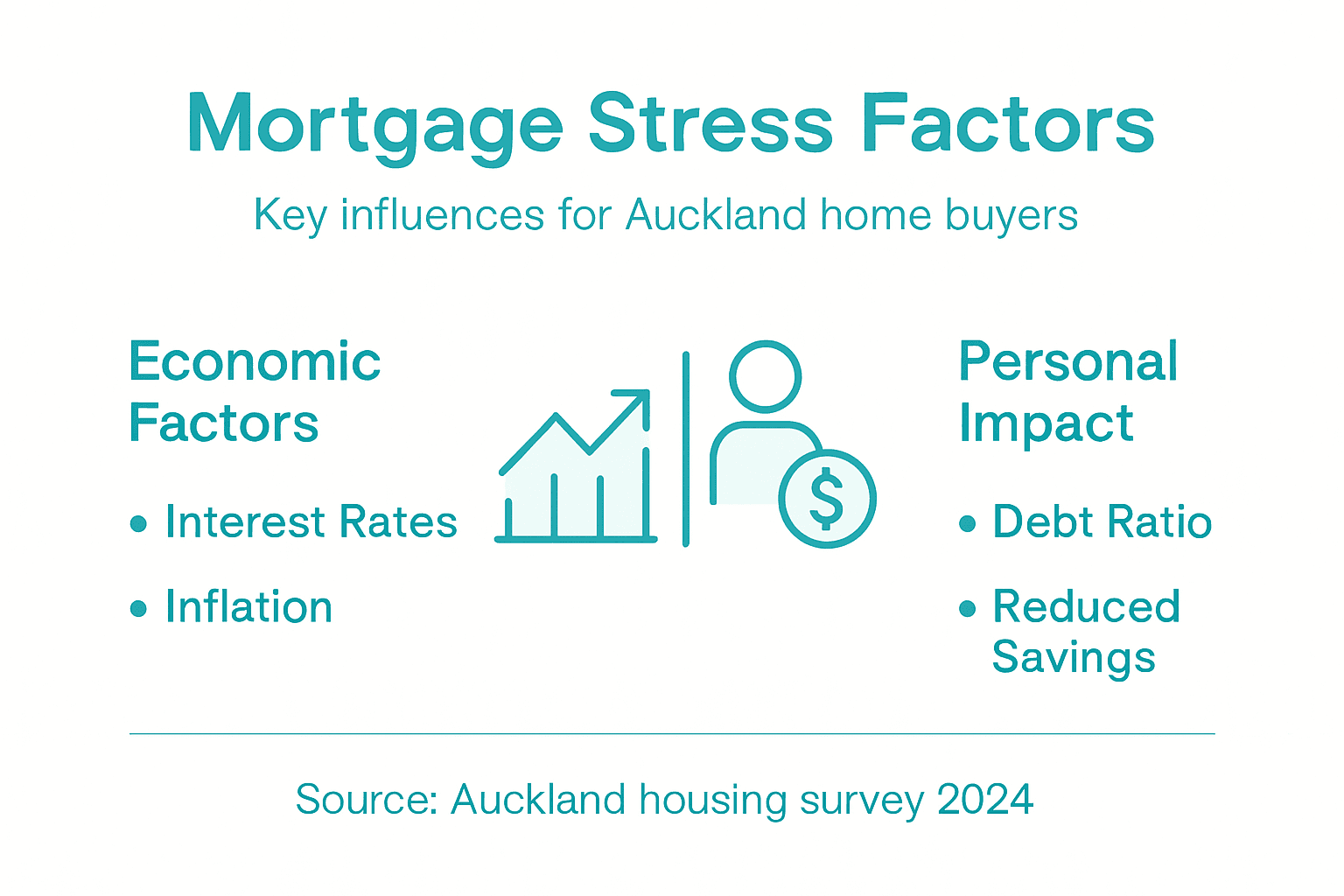

Mortgage stress represents a significant financial challenge for New Zealand households, characterised by the intense pressure of housing expenses overwhelming personal income. Housing cost statistics reveal that households are experiencing unprecedented financial strain, with mortgage payments consuming an increasingly larger portion of their disposable earnings.

In practical terms, mortgage stress occurs when homeowners spend more than 30% of their pre-tax income on housing expenses, creating substantial financial vulnerability. The economic landscape in New Zealand has witnessed a dramatic shift, with over half the population reporting ongoing money worries, particularly among women and Māori communities who face disproportionate financial challenges.

The primary drivers of mortgage stress include rising interest rates, inflation, and stagnant wage growth. Households find themselves trapped in a challenging economic environment where mortgage payments have increased by 8.7%, forcing many to make difficult financial trade-offs. This stress extends beyond mere monetary concerns, impacting mental health, relationships, and overall quality of life for New Zealand families.

Pro tip: Regularly review your mortgage structure and explore refinancing options to potentially reduce your monthly repayment burden and mitigate mortgage stress.

How Mortgage Stress Manifests In Auckland

Auckland homeowners are experiencing profound mortgage stress through dramatic increases in monthly loan repayments. Mortgage refix shock creates substantial financial pressure, with many households facing unexpected monthly payment jumps between $200 and $600, significantly disrupting household budgets and financial planning.

The local property market demonstrates complex stress indicators, where housing affordability remains challenging despite recent market shifts. Home affordability continues showing mixed signals, with many Auckland borrowers dedicating an unsustainable proportion of their income towards mortgage payments. This financial strain emerges from historically high property values, substantial loan balances, and wage growth that consistently lags behind housing expenses.

Mortgage stress in Auckland typically manifests through several key indicators: increasing debt-to-income ratios, reduced discretionary spending, delayed major life decisions, and heightened financial anxiety. Younger homeowners and first-time buyers are particularly vulnerable, often stretching their financial resources to maximum capacity just to maintain homeownership in this competitive market. The psychological toll can be significant, with ongoing financial pressure impacting mental health and overall quality of life.

Pro tip: Consider consulting a mortgage adviser to explore potential loan restructuring or refinancing strategies that could help reduce your monthly repayment burden and mitigate mortgage stress.

Major Causes: High Costs And Refixing Rates

Mortgage stress in New Zealand stems primarily from the dramatic shifts in lending environments, with mortgage interest payments surging dramatically, increasing nearly 50% in a single year. This substantial rise creates significant financial pressure for homeowners, particularly those facing loan refixing at substantially higher interest rates.

The primary mechanisms driving mortgage stress include several interconnected factors. Large loan balances resulting from peak housing prices, combined with extended loan terms, exponentially increase interest exposure. Homeowners who secured mortgages during historically low interest periods are now confronting a harsh financial reality, with mortgage refix shock causing substantial monthly payment increases ranging between $200 and $600, effectively destabilising household budgets.

Additionally, broader economic pressures compound these challenges. Stagnant wage growth, persistent inflation, and increased cost of living create a perfect storm for financial strain. Younger homeowners and first-time buyers are particularly vulnerable, often stretching their financial resources to maximum capacity just to maintain homeownership. The psychological impact extends beyond mere financial calculations, affecting mental health, relationship dynamics, and long-term life planning strategies.

Here’s a summary of key differences in mortgage stress impacts across New Zealand regions:

| Region | Main Mortgage Stress Trigger | Typical Increase in Payments | Most Affected Group |

|---|---|---|---|

| Auckland | Mortgage refix shock | $200–$600 per month | Young homeowners, first buyers |

| Hobsonville | High prices & low buffers | High upfront loan balances | Newly established families |

| Nationwide | Inflation and stagnant wages | 8.7% overall payment rise | Women and Māori households |

Pro tip: Consider negotiating with your current lender or exploring refinancing options to potentially reduce your monthly mortgage burden and mitigate financial stress.

Who Is Most At Risk In Hobsonville

In the Hobsonville housing market, first home buyers face significant financial vulnerability, with specific demographic groups experiencing heightened mortgage stress. Young professionals, newly established families, and lower to middle-income households are particularly exposed to economic pressures that can quickly destabilise their financial foundations.

Mortgage Risk Profiles include several key vulnerable groups:

- First-time homeowners with limited financial buffers

- Young couples purchasing their initial property

- Families with single or unstable income streams

- Recent migrants establishing themselves in the Auckland region

- Professionals working in emerging or volatile industries

Home affordability challenges continue impacting buyers, with Māori and Pasifika populations experiencing disproportionate financial strain. These communities often lack generational wealth or established support networks, making mortgage repayments substantially more challenging. The combination of high house prices, substantial borrowing requirements, and limited income growth creates a precarious financial landscape for these vulnerable populations.

Pro tip: Develop a comprehensive financial emergency plan that includes at least three months of mortgage payments in a separate, easily accessible savings account to provide a critical financial buffer.

Strategies To Manage Or Reduce Mortgage Stress

Improving financial management skills represents the primary strategy for combating mortgage stress among New Zealand homeowners. This involves developing robust budgeting techniques, carefully tracking expenses, and creating flexible financial plans that can adapt to changing economic circumstances.

Key Stress Reduction Strategies:

- Conduct a comprehensive household budget review

- Identify and eliminate non-essential expenditures

- Build an emergency savings fund

- Explore additional income streams

- Negotiate better rates with current lenders

Microfinance options offer alternative support for households struggling with mortgage repayments. By accessing tailored financial education and affordable credit options, homeowners can develop more sustainable approaches to managing their mortgage obligations. Professional financial advisers can provide personalised guidance, helping to restructure loans, consolidate debts, and develop long-term financial resilience.

The table below compares the most effective strategies to manage mortgage stress:

| Strategy | Main Benefit | Suitable For |

|---|---|---|

| Comprehensive budget review | Identifies cost-saving options | All homeowners |

| Emergency savings fund | Provides financial buffer | Risk-prone households |

| Refinancing or loan restructure | Potential payment reduction | High-debt or stressed owners |

| Microfinance support | Access to affordable credit | Low-income borrowers |

Pro tip: Create a dedicated spreadsheet tracking all mortgage-related expenses and potential savings opportunities, reviewing it monthly to identify potential areas for financial optimization.

Take Control of Mortgage Stress in Auckland Today

Mortgage stress caused by rising mortgage payments and refixing rate shocks can feel overwhelming for Auckland home buyers. If you are feeling the pressure of managing high repayments or uncertain about how to restructure your loan to ease the burden, you are not alone. Many homeowners in Hobsonville and surrounding areas face the challenge of mortgage stress impacting their finances and wellbeing.

At Mortgage Managers, a trusted team of Auckland mortgage advisers based in Hobsonville, we specialise in helping you navigate these exact difficulties. We offer personalised advice aimed at reducing your monthly repayments through refinancing or loan restructuring options that suit your unique situation. Don’t wait until mortgage stress affects your future plans. Discover practical solutions tailored for Auckland homeowners by visiting Mortgage Managers now and start your path towards financial relief.

Explore expert insights and personalised support designed to help you manage mortgage stress at Mortgage Managers Home. Take the first step to regain peace of mind and control over your mortgage payments today.

Frequently Asked Questions

What is mortgage stress?

Mortgage stress occurs when homeowners spend more than 30% of their pre-tax income on housing expenses, leading to significant financial strain and vulnerability.

How does mortgage refixing affect borrowers in Auckland?

Mortgage refixing can lead to substantial monthly payment increases, often between $200 and $600, causing unexpected financial pressure and disrupting household budgets.

What are the main causes of mortgage stress among home buyers?

The primary causes of mortgage stress include rising interest rates, inflation, stagnant wage growth, and high property values, all of which increase the financial burden on homeowners.

What strategies can help manage mortgage stress?

Effective strategies include conducting a comprehensive budget review, building an emergency savings fund, exploring additional income streams, and negotiating better rates with lenders.