For many Auckland first home buyers, trying to secure a mortgage with a low deposit or imperfect credit can quickly feel overwhelming. Understanding how to approach banks and navigate financial obstacles is a challenge that leaves many unsure where to start. Mortgage advisers act as trusted financial supporters, connecting buyers with lenders, explaining loan options in plain language, and guiding each step of the process, making the dream of home ownership more realistic for those facing extra hurdles.

Table of Contents

- Defining Mortgage Advisers In Home Buying

- Different Types Of Mortgage Advice Available

- How Mortgage Advisers Support First Home Buyers

- Legal Responsibilities And Industry Regulation

- Fees, Costs And Common Pitfalls To Avoid

Key Takeaways

| Point | Details |

|---|---|

| Role of Mortgage Advisers | Mortgage advisers serve as crucial financial intermediaries for first-time home buyers, simplifying complex loan processes and providing tailored advice. |

| Types of Mortgage Advice | Various advice pathways include bank-direct, independent brokers, online platforms, and specialised services, each with different advantages and fee structures. |

| Support for First Home Buyers | Mortgage advisers assist first home buyers by assessing finances, guiding through government schemes, and matching them with suitable lenders. |

| Understanding Fees and Costs | Clients should be aware of different fee structures and potential hidden costs, ensuring transparency to avoid conflicts of interest. |

Defining Mortgage Advisers in Home Buying

A mortgage adviser plays a pivotal role in the home buying journey for Kiwi first-time homeowners, serving as a strategic financial intermediary between potential buyers and lending institutions. Mortgage advisers in New Zealand help clients navigate the complex landscape of home loan options, providing expert guidance tailored to individual financial circumstances.

These financial professionals perform several critical functions in the home buying process:

- Assess individual financial situations and borrowing capacity

- Research and compare loan products from multiple lenders

- Explain complex loan features and associated costs

- Assist with loan application documentation

- Provide strategic financial advice specific to home purchasing

The primary advantage of working with a mortgage adviser lies in their ability to simplify what can often be an overwhelming financial decision. They bring specialised knowledge about lending criteria, interest rates, and loan structures that most individual borrowers might not readily understand.

Mortgage advisers are not just intermediaries, but strategic partners who help transform home ownership dreams into achievable realities.

Financial expertise distinguishes mortgage advisers from direct bank representatives. While bank staff typically promote their institution’s products, mortgage advisers can provide independent recommendations drawing from a broader range of lending options.

Pro tip: Before engaging a mortgage adviser, request a clear breakdown of their service fees and confirm they are registered with the Financial Markets Authority.

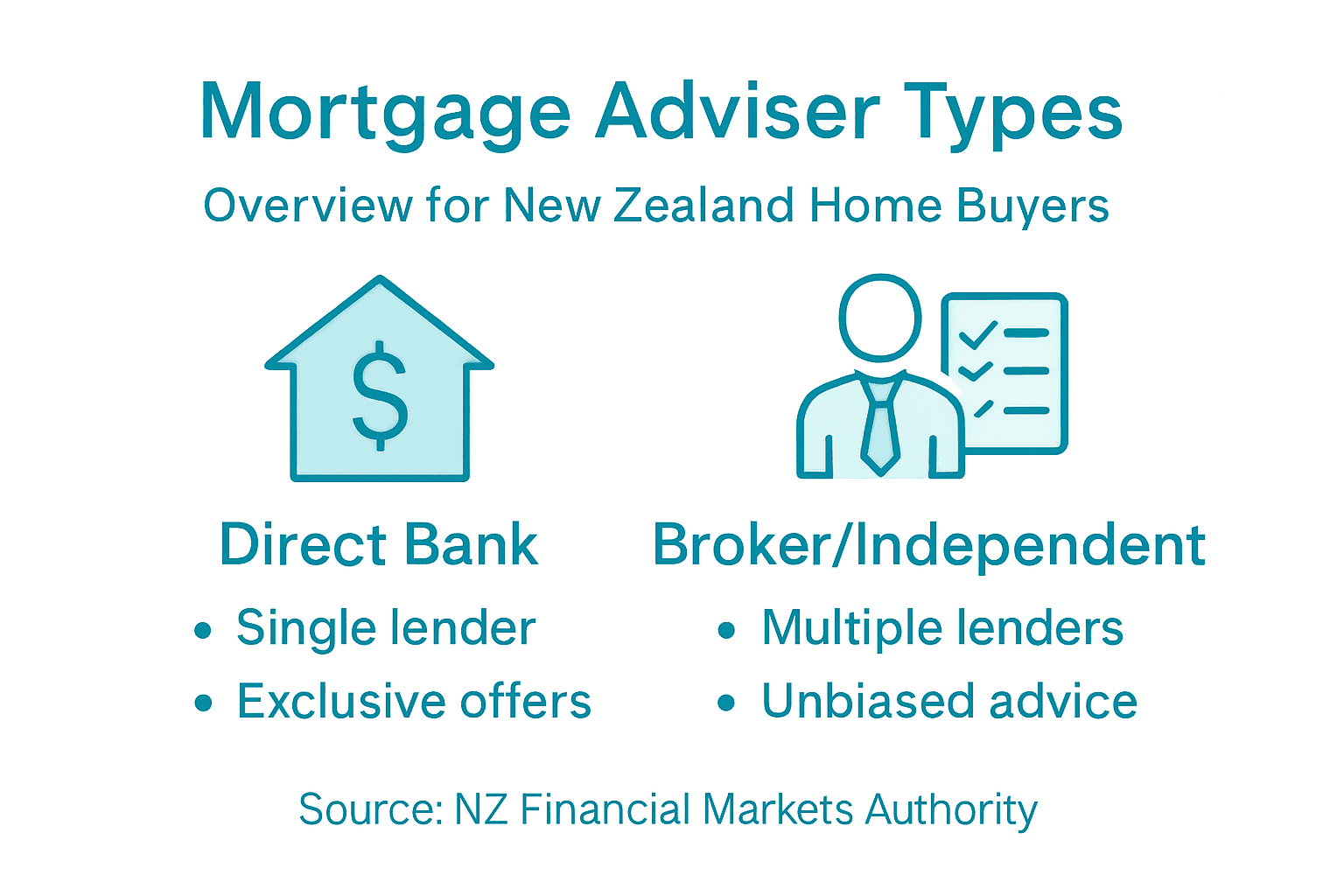

Different Types of Mortgage Advice Available

In the New Zealand mortgage landscape, home buyers have multiple pathways to obtaining financial guidance, each with unique characteristics and potential benefits. Mortgage advice services vary significantly, allowing buyers to choose an approach that best suits their individual financial circumstances and preferences.

The primary types of mortgage advice available include:

- Bank-Direct Advice: Consultation provided directly by banking institution staff

- Independent Mortgage Broker Advice: Guidance from registered professionals working across multiple lenders

- Online Mortgage Platforms: Digital services offering comparison and initial recommendations

- Specialised Financial Advisory Services: Comprehensive financial planning incorporating mortgage strategies

Each advice type presents distinct advantages. Bank-direct advisers provide in-depth knowledge of their institution’s specific products, while independent mortgage brokers offer broader market perspectives and potentially more flexible recommendations. Digital platforms increasingly provide quick, algorithmic comparisons that can help initial decision-making.

Here’s a side-by-side comparison of the main types of mortgage advice available in New Zealand:

| Advice Type | Scope of Recommendations | Access to Lenders | Typical Fees |

|---|---|---|---|

| Bank-Direct | Bank’s own products only | Single institution | Usually free, may have indirect costs |

| Independent Broker | Broad market selection | Multiple lenders | May earn commissions, sometimes client fees |

| Online Platform | Algorithmic product comparison | Several lenders | Free or small fixed fee |

| Financial Adviser | Full financial planning | Access varies | Client pays upfront advisory fees |

Independent mortgage advisers offer the most comprehensive view of available lending options, potentially saving buyers significant time and money.

The key differentiator between these advice types lies in their compensation structures. Some advisers receive direct commissions from lenders, while others charge clients upfront fees. This variance can potentially influence the objectivity of recommendations, making it crucial for home buyers to understand how their chosen adviser is compensated.

Pro tip: Always request a clear disclosure of your mortgage adviser’s fee structure and potential conflicts of interest before committing to their services.

How Mortgage Advisers Support First Home Buyers

First home buyers face numerous financial challenges, and mortgage advisers play a crucial role in simplifying their journey towards property ownership. First home buyer support services provide targeted guidance through the complex landscape of home financing, helping young Kiwis navigate their initial property investment.

Specifically, mortgage advisers support first home buyers through several key strategies:

- Financial Assessment: Comprehensive evaluation of borrowing capacity and financial readiness

- Government Scheme Navigation: Explaining eligibility for First Home Loans and grants

- KiwiSaver Withdrawal Guidance: Helping maximise savings and understanding withdrawal options

- Deposit Strategy Development: Creating realistic savings plans and investment approaches

- Lender Matching: Connecting buyers with most appropriate lending institutions

Mortgage advisers understand the unique challenges faced by first home buyers, particularly those struggling to accumulate substantial deposits or manage complex lending criteria. Financial complexity can be overwhelming, and these professionals provide a critical bridge between buyers’ aspirations and practical financial solutions.

Mortgage advisers are the strategic partners that transform home ownership from a distant dream into an achievable reality for first home buyers.

Beyond financial guidance, these professionals offer emotional support and confidence-building throughout the home buying process. They demystify technical jargon, explain intricate loan structures, and help buyers make informed decisions that align with their long-term financial goals.

Pro tip: Bring a comprehensive financial snapshot to your first mortgage adviser meeting, including income statements, existing savings, and current debt obligations.

Legal Responsibilities and Industry Regulation

Mortgage advisers in New Zealand operate within a stringent regulatory framework designed to protect consumers and ensure professional standards. Financial adviser regulations establish clear guidelines that govern professional conduct, transparency, and ethical practice in the financial services industry.

The key legal responsibilities for mortgage advisers include:

- Registration Requirements: Mandatory registration with Financial Markets Authority (FMA)

- Disclosure Obligations: Clear communication of fees, commissions, and potential conflicts of interest

- Professional Conduct Standards: Acting in clients’ best financial interests

- Confidentiality Protocols: Protecting client financial information

- Ongoing Professional Development: Maintaining current industry knowledge and qualifications

Regulatory compliance represents more than just a legal requirement; it’s a fundamental commitment to maintaining trust and integrity in financial services. Mortgage advisers must navigate complex legal landscapes, ensuring every recommendation meets strict professional standards and consumer protection guidelines.

Legal accountability transforms mortgage advisers from mere service providers into trusted financial guardians.

Consumers have multiple layers of protection through established complaint mechanisms and regulatory oversight. If an adviser fails to meet professional standards, clients can lodge formal complaints with the Financial Markets Authority or seek resolution through independent dispute resolution schemes.

Pro tip: Always request and verify an adviser’s current registration status with the Financial Markets Authority before engaging their services.

Fees, Costs and Common Pitfalls to Avoid

Navigating the financial landscape of mortgage advice requires a keen understanding of potential costs and hidden risks. Mortgage adviser fee structures can be complex, with various compensation models that directly impact the advice clients receive.

Common fee and cost structures for mortgage advisers include:

- Commission-Based Fees: Payments received from lending institutions

- Direct Client Fees: Upfront charges for advisory services

- Hybrid Fee Models: Combination of commissions and client-paid fees

- Performance-Based Fees: Compensation tied to successful loan placement

- Ongoing Service Fees: Charges for continued financial support

Financial transparency is crucial in preventing potential conflicts of interest. Some advisers might be tempted to recommend loans that generate higher commissions rather than those most suitable for the client’s specific financial situation.

The following table summarises common fee models for mortgage advisers and their impact on advice quality:

| Fee Structure | Client Cost | Impact on Recommendations | Transparency Level |

|---|---|---|---|

| Commission-Based | Usually zero upfront | May favour higher yields | Medium; disclosure required |

| Direct Client Fees | Fixed upfront charge | Objective, less influence | High; fully disclosed |

| Hybrid Model | Mix of fees | Potentially mixed incentives | Depends on disclosure |

| Performance-Based | Varies; contingent | May focus on quick approvals | Needs careful scrutiny |

Not all fees are created equal, and the cheapest option is rarely the most cost-effective in the long term.

Pitfalls to watch out for include accepting short-term incentives without considering long-term loan implications, failing to compare multiple lending options, and not fully understanding the total cost of borrowing. Clients should always request a comprehensive breakdown of all potential fees and charges before committing to any financial product.

Pro tip: Request a written fee disclosure document that outlines all potential costs, including hidden fees and commission structures, before signing any mortgage agreement.

Expert Mortgage Advice Tailored for Kiwi Home Buyers

Navigating the complex world of mortgage options and government schemes can leave many first home buyers feeling overwhelmed and uncertain. The article highlights how critical it is to work with mortgage advisers who understand your unique financial situation and can explain confusing loan features while helping you avoid costly pitfalls. At Mortgage Managers, we specialise in providing transparent, independent advice that aligns with your goals and supports you every step of the way.

Whether you are struggling to build a deposit, maximise government grants, or simply want the best loan for your needs, our Auckland-based team is here to simplify the process. We have the expertise to research multiple lenders, clarify fees and commissions, and protect your interests in a regulated market. Take control of your home buying journey with trusted advice from Mortgage Managers.

Don’t let financial uncertainty slow your dream of home ownership. Connect today with Mortgage Managers for personalised mortgage advice designed for Kiwis. Learn more about how our services can help you cut through complexity and get started now. Your future home awaits – make the move with confidence.

Frequently Asked Questions

What is the role of a mortgage adviser in the home buying process?

A mortgage adviser acts as a financial intermediary, helping potential buyers navigate home loan options, assess their financial situations, and guide them through the application process.

How can mortgage advisers help first home buyers?

Mortgage advisers support first home buyers by evaluating their borrowing capacity, explaining government schemes, assisting with KiwiSaver withdrawals, and developing deposit strategies to match them with suitable lenders.

What types of mortgage advice are available for Kiwis?

Various types of mortgage advice include bank-direct advice, independent mortgage broker advice, online mortgage platforms, and specialised financial advisory services, each offering different scopes of recommendations and access to lenders.

What should I consider when choosing a mortgage adviser?

It’s important to consider an adviser’s fee structure, their registration status with regulatory authorities, their ability to provide independent recommendations, and their experience in handling your specific financial situation.