TL;DR:

- VA home loan rates are currently below conventional rates, offering significant savings for eligible veterans.

- Lenders set these rates based on market conditions and individual financial profiles, not the VA itself.

The VA home loan rate is the interest charged on mortgages guaranteed by the U.S. Department of Veterans Affairs, and it typically runs lower than conventional mortgage rates. Veterans and active service members gain access to this benefit without needing a down payment or private mortgage insurance, making it one of the most powerful home financing tools available. Understanding how these rates are set, what moves them, and how your personal financial profile affects your offer puts you in a far stronger position at the negotiating table.

What are the current VA home loan rates in 2026?

The national average rate for a 30-year fixed-rate VA mortgage sits at 5.75% as of june 21, 2026, with an average APR of 5.96%. That figure is 9 basis points lower than the week prior and 50 basis points lower than the same time last year. The downward movement reflects a broader easing trend that has played out across the first half of 2026.

VA mortgage interest rates have trended downward from around 7.1% at the start of the year to the mid-5% range by june. The primary drivers are Federal Reserve policy shifts and changes in mortgage-backed securities spreads. When the Fed signals rate cuts or bond markets rally, VA loan rates tend to follow.

To put the current numbers in context, the average conventional loan rate was 6.89% in april 2026, compared to 5.83% for VA loans in the same period. That gap of more than 1 percentage point translates to meaningful savings over a 30-year term.

| Loan type | April 2026 average rate | Key feature |

|---|---|---|

| VA 30-year fixed | 5.83% | No PMI, zero down payment |

| Conventional 30-year fixed | 6.89% | PMI required under 20% down |

| FHA 30-year fixed | Varies by lender | Mortgage insurance required |

Daily fluctuations are real. Mortgage-backed securities pricing and Federal Reserve announcements cause VA loan rate offers to shift from one business day to the next. Locking your rate at the right moment matters more than most veterans realise.

How do personal factors influence the VA home loan rate you are offered?

The VA does not set your mortgage rate. Lenders set their own rates based on their own pricing strategies and your individual financial profile. Two veterans applying on the same day can receive meaningfully different offers from the same lender.

Several borrower-specific factors shape the rate you see:

- Credit score. Borrowers with scores above 720 typically receive the lowest VA loan rates. Scores in the 580–620 range may attract higher rates or stricter conditions. Lenders apply their own thresholds on top of VA guidelines, so a score that qualifies you for the loan does not guarantee the best pricing.

- Debt-to-income ratio (DTI). A high DTI signals greater repayment risk to lenders. Keeping your DTI below 41% is the standard VA guideline, though lenders often prefer lower figures when pricing competitive rates.

- Loan amount and term. Larger loan amounts and shorter repayment terms affect how lenders price risk. A 15-year VA loan generally carries a lower rate than a 30-year term.

- Loan type. Purchase loans, Interest Rate Reduction Refinance Loans (IRRRLs), and cash-out refinances each carry different rate profiles. IRRRLs often attract the most competitive rates because the VA streamlines the approval process.

Pro Tip: Spend three to six months before applying improving your credit profile. Pay down revolving balances, dispute any errors on your credit report, and avoid opening new accounts. Even a 20-point lift in your score can shift your offered rate by a meaningful margin.

Understanding how lender overlays affect your rate is equally important. Lenders layer their own credit score and DTI thresholds on top of VA guidelines. A borrower who meets the VA minimum may still face higher rates or a denial from a lender with tighter internal standards.

VA home loan rate vs conventional loan: what is the real cost difference?

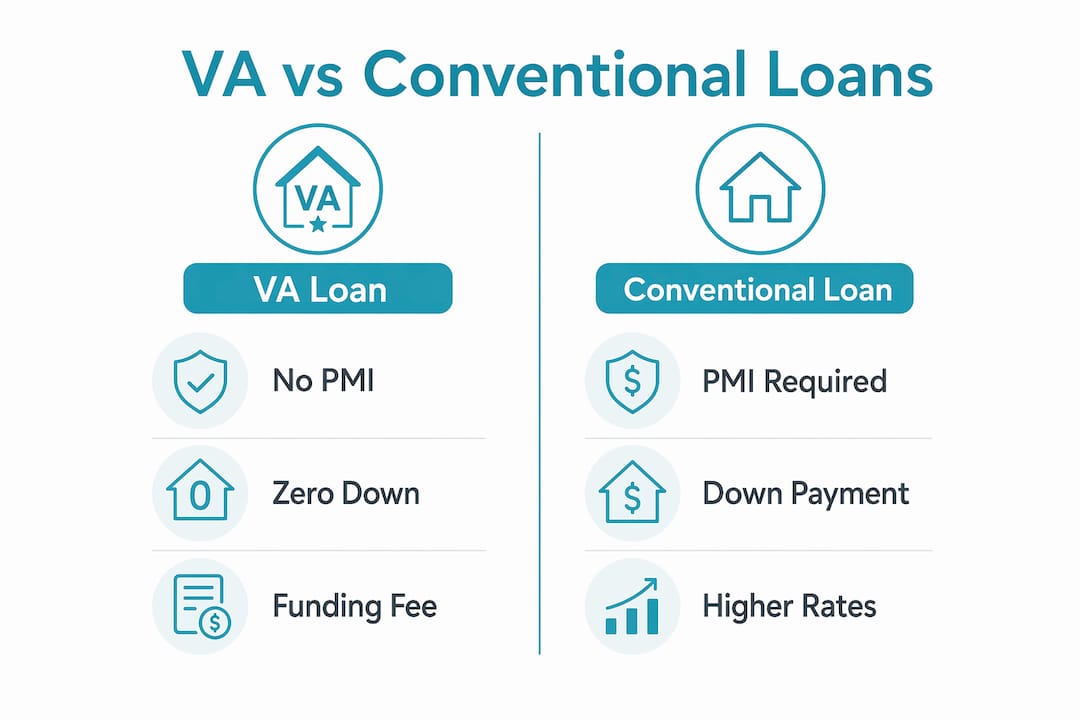

The interest rate is only one piece of the total cost picture. VA loans allow zero down payment and no PMI, which changes the monthly payment and the life-of-loan cost dramatically compared to a conventional loan.

Private mortgage insurance on a conventional loan typically adds a noticeable monthly cost for borrowers who put down less than 20%. No monthly PMI is one of the most significant financial advantages of the VA programme. Over a 30-year loan, that saving compounds into a substantial figure.

The VA funding fee is the one upfront cost unique to VA loans. It varies based on your down payment amount, whether you are a first-time or subsequent VA loan user, and your service type. The fee can be financed into the loan amount, so it does not require cash at closing. Veterans with a service-connected disability rating are exempt from the funding fee entirely.

| Cost factor | VA loan | Conventional loan (under 20% down) |

|---|---|---|

| Interest rate (april 2026) | 5.83% | 6.89% |

| Monthly PMI | None | Required |

| Down payment | Zero required | Typically 5%–20% |

| Funding fee | Applies (can be financed) | None |

| Overall monthly cost | Generally lower | Generally higher |

Pro Tip: Ask your lender to run a side-by-side Loan Estimate comparing your VA loan against a conventional option at the same purchase price. The total cost difference over five years is often far larger than the rate difference alone suggests.

Even if a VA loan rate were slightly higher than a conventional rate in a given market, the absence of PMI and the zero down payment requirement frequently make the VA option cheaper in total. Total loan cost, not just the headline rate, is the number that matters.

What practical steps help veterans secure the best VA home loan rate?

Shopping around is the single most effective action you can take. Getting quotes from at least 3–4 lenders significantly improves your odds of securing the best available rate and terms. The VA loan market is competitive, and lenders price risk differently.

Follow these steps to approach the process with confidence:

- Pull your Certificate of Eligibility (COE) first. Confirm your VA entitlement before approaching lenders. It signals to lenders that you are a serious, qualified borrower.

- Request Loan Estimates from multiple lenders. A Loan Estimate is a standardised document that shows the interest rate, APR, closing costs, and monthly payment. Compare APR across lenders, not just the interest rate, because APR includes fees and gives a truer cost picture.

- Look at points and origination fees. Some lenders offer a lower rate in exchange for upfront discount points. Calculate how long it takes to recoup that cost through monthly savings before deciding whether to pay points.

- Work with a mortgage adviser familiar with VA loans. A broker who regularly works with VA borrowers knows which lenders are currently pricing VA loans aggressively. That knowledge saves you time and often money. Mortgagemanagers specialises in exactly this kind of comparison work for borrowers navigating complex loan options.

- Lock your rate at the right moment. Because daily market movements shift VA loan rate offers, locking when rates dip is worth the attention. Ask your lender about float-down options if you want protection against further rate drops after locking.

Pro Tip: Use a VA loan rate calculator to model different rate scenarios before you speak to lenders. Knowing your numbers going in makes you a far more confident negotiator.

For veterans looking to get the lowest fixed rate, preparation and comparison are the two levers that deliver the most consistent results. Reviewing tips for shopping mortgage rates before you start the process gives you a clear framework for evaluating every offer you receive.

Key takeaways

VA home loan rates consistently run below conventional mortgage rates, and veterans who combine a strong credit profile with disciplined lender comparison can secure the most favourable terms available in the current market.

| Point | Details |

|---|---|

| Current VA rate | The 30-year fixed VA rate averaged 5.75% as of june 21, 2026, well below conventional averages. |

| Rate is lender-set | The VA does not set rates; shopping at least 3–4 lenders is the most effective way to find the best offer. |

| Credit score matters | Scores above 720 access the lowest rates; improving your score before applying delivers real savings. |

| Total cost beats rate alone | No PMI and zero down payment make VA loans cheaper overall, even when rates are similar to conventional options. |

| Funding fee awareness | The VA funding fee affects total cost but can be financed into the loan; exempt for veterans with disability ratings. |

My honest view on VA home loan rates after years in mortgage advice

Veterans often walk into the rate conversation fixated on the headline number. I understand why. A lower rate feels like a clear win. But the most costly mistake I see is choosing a lender based on the rate alone without reading the full Loan Estimate.

The variation between lender quotes on VA loans is genuinely surprising. Two lenders quoting on the same day for the same borrower can differ by 0.25% or more on the rate, and even more when you factor in origination fees and points. That gap is not small. On a $400,000 loan over 30 years, a quarter-point difference in rate adds up to tens of thousands of dollars.

My strongest advice is to treat the funding fee and the absence of PMI as part of your rate calculation, not as separate considerations. A veteran comparing a 5.9% VA loan against a 5.7% conventional loan needs to factor in the PMI cost on the conventional side before concluding the conventional option is cheaper. Most of the time, it is not.

Prepare your financial profile before you apply. Pay down debt, check your credit report for errors, and avoid large new purchases in the months before you seek pre-approval. The veterans I have seen secure the best rates are the ones who treated the preparation phase as seriously as the application itself.

— Stuart

How Mortgagemanagers helps veterans find the right home loan rate

Comparing VA loan offers across multiple lenders takes time and expertise that most veterans simply do not have while managing careers and family commitments.

Mortgagemanagers works as your personal mortgage shopper, comparing lender offers, reviewing Loan Estimates, and identifying the options that deliver the best total cost for your situation. The team understands how lender overlays, funding fees, and credit profiles interact to shape your final rate. Whether you are purchasing your first home or refinancing an existing VA loan, Mortgagemanagers brings the lender knowledge and comparison experience that turns a complex process into a clear decision. Reach out to the team at Mortgagemanagers to get started.

FAQ

What is the current VA home loan rate in 2026?

The national average VA loan rate for a 30-year fixed mortgage is 5.75% as of june 21, 2026. Rates vary by lender, credit score, and loan type.

Does the VA set mortgage interest rates?

The VA does not set mortgage rates. Lenders set their own rates based on market conditions and individual borrower profiles, which is why comparing multiple lenders is so important.

Are VA loan rates lower than conventional loan rates?

VA loan rates are generally lower than conventional rates. The average VA rate was 5.83% in april 2026, compared to 6.89% for conventional loans in the same period.

What credit score do I need for the best VA loan rate?

Borrowers with credit scores above 720 typically access the lowest available VA rates. Scores in the 580–620 range may result in higher rates or stricter lending conditions.

Is the VA funding fee worth paying?

The VA funding fee is a one-time cost that replaces the ongoing PMI required on conventional loans. For most veterans, the total savings from no PMI over the life of the loan outweigh the upfront funding fee, particularly when the fee is financed into the loan amount.