Searching for your first home in Auckland often means facing a maze of mortgage offers, each with its own rules, rates, and promises. For buyers with a low deposit, the challenge goes beyond the headline interest rates and digs into comparing hidden fees, approval criteria, and real affordability. By understanding why lender comparison is more than just rate shopping, you can avoid costly mistakes and find a mortgage partner that truly supports your journey to home ownership.

Table of Contents

- What Comparing Lenders Really Means

- Types of Mortgage Lenders in New Zealand

- How Interest Rates, Fees and Terms Differ

- Low Deposit Options and Special Programs

- Risks, Pitfalls and How to Maximise Savings

Key Takeaways

| Point | Details |

|---|---|

| Comprehensive Lender Comparison | Assess various lenders by focusing on interest rates, fees, conditions, and customer service to find the best mortgage for your needs. |

| Diverse Lending Options | Explore multiple types of lenders, including traditional banks, non-bank lenders, credit unions, and specialists, to meet specific borrowing profiles. |

| Understand Costs and Risks | Evaluate all potential fees and interest rate structures to avoid hidden costs and ensure affordability in the long term. |

| Utilise Low Deposit Solutions | Consider government-backed low deposit schemes and consult a mortgage broker to navigate these options effectively. |

What Comparing Lenders Really Means

Comparing lenders isn’t just about finding the lowest interest rate. It’s a strategic process of evaluating multiple home loan options to secure the most suitable mortgage for your unique financial situation. When you approach mortgage comparison systematically, you’re essentially performing a comprehensive financial health check on potential lending pathways.

The core of lender comparison involves thoroughly examining multiple dimensions beyond surface-level interest rates. This includes scrutinising home loan conditions and fees that can significantly impact your long-term financial commitment. Successful borrowers analyse elements like establishment costs, ongoing fees, repayment flexibility, fixed versus floating rate options, and potential penalties for early loan termination.

Beyond numerical comparisons, comparing lenders also means understanding each institution’s lending criteria, approval processes, and customer service reputation. Some lenders specialise in first home buyers, while others might have more stringent requirements or offer more flexible terms for self-employed individuals. This nuanced approach helps Auckland homebuyers identify not just an affordable loan, but the right lending partner aligned with their specific financial goals.

Pro tip: Consider engaging a mortgage broker who can efficiently compare multiple lenders simultaneously and provide tailored recommendations based on your individual financial profile.

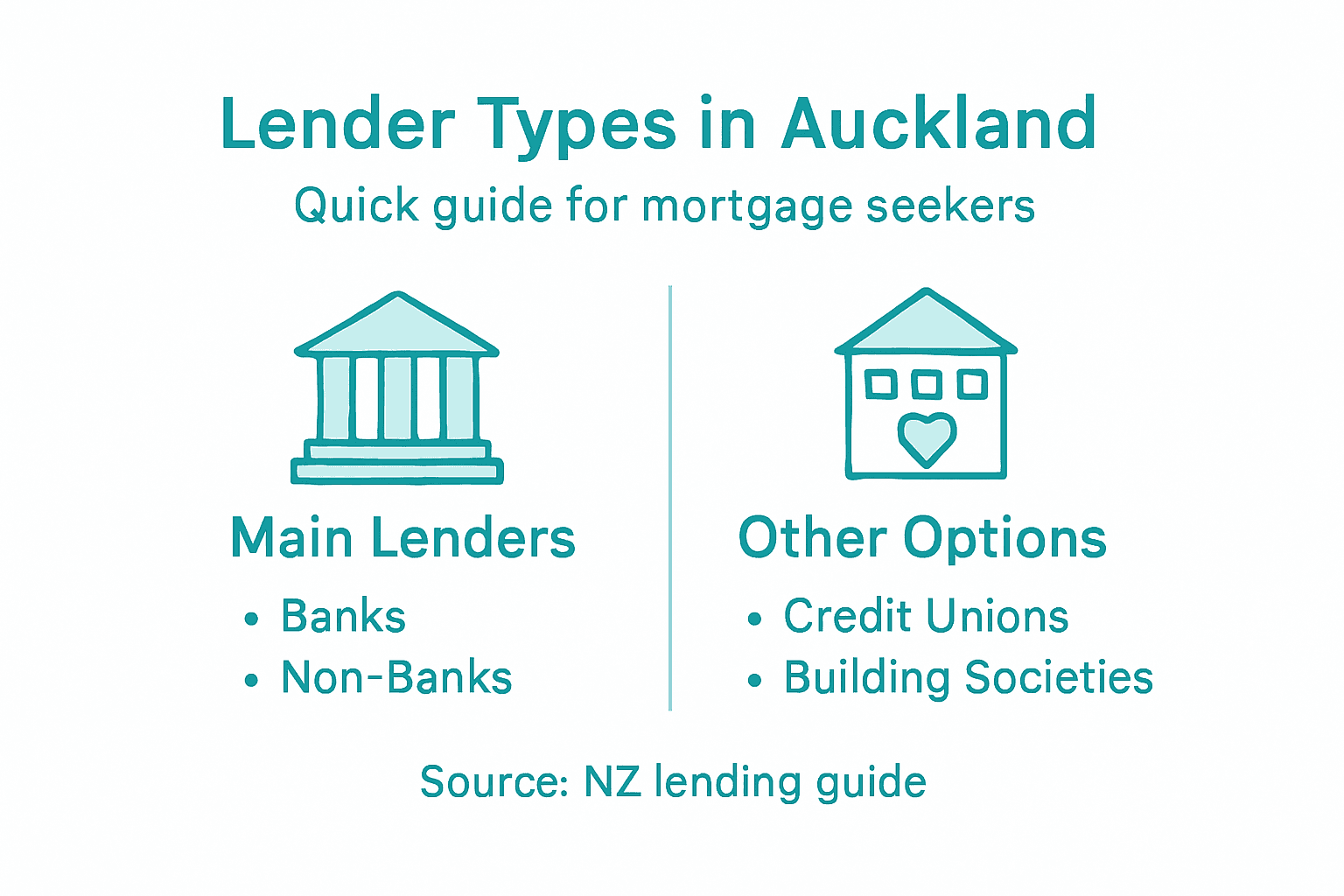

Types of Mortgage Lenders in New Zealand

The New Zealand mortgage lending landscape is diverse and complex, featuring multiple types of financial institutions that offer home loan products to potential borrowers. While traditional banks remain the most prominent lenders, the market has evolved to include a range of alternative financing options designed to meet varying financial needs and circumstances.

Traditional banks represent the primary mortgage lenders in New Zealand, offering standardised home loan products with relatively consistent credit assessment processes. However, mortgage brokers recognise the increasing importance of non-bank lenders who provide more flexible lending criteria. These non-bank institutions often specialise in serving borrowers who might not meet strict bank requirements, such as self-employed professionals, contract workers, or those with non-traditional income streams.

Beyond banks and non-bank lenders, the New Zealand mortgage market also includes credit unions, building societies, and specialist mortgage providers. Each of these institutions has unique lending approaches, with some focusing on specific geographic regions or particular borrower profiles. For Auckland homebuyers, this means having access to a wide range of lending options that can be tailored to individual financial situations, from first-time buyers to property investors seeking specialised financing solutions.

Here’s a summary of major mortgage lender types and how they differ in New Zealand:

| Lender Type | Typical Borrower Profile | Flexibility & Criteria | Key Distinctions |

|---|---|---|---|

| Traditional Banks | Salaried, stable income | Standard criteria, moderate | Widest product range, strict rules |

| Non-Bank Lenders | Self-employed, contractors | Flexible, tailored assessments | Accepts varied income sources |

| Credit Unions | Community focused, diverse | Regional or membership criteria | Often lower fees, local expertise |

| Building Societies | Regional buyers, niche needs | Specialised loans, specific info | Small scale, personal approach |

| Specialists | Unique or complex cases | Custom programmes, assessments | Targets investors or first-home |

Pro tip: Always consult with a mortgage broker who can navigate the complex landscape of lenders and help you identify the most suitable mortgage option for your specific financial circumstances.

How Interest Rates, Fees and Terms Differ

Navigating the mortgage landscape means understanding the nuanced differences between lenders’ interest rates, fees, and loan terms. Each financial institution approaches these elements uniquely, creating a complex ecosystem where seemingly small variations can translate into substantial financial implications for borrowers.

Interest rates represent the most visible point of comparison, with lenders offering different fixed and floating rate options. Fixed rates provide stability and predictability, locking in an interest percentage for a specific period, while floating rates fluctuate with market conditions. Mortgage rate strategies can significantly impact your long-term financial planning, with some lenders offering more competitive introductory rates or relationship-based pricing for existing customers.

Beyond interest rates, borrowers must carefully evaluate establishment fees, ongoing administration charges, and potential penalty costs for early repayment or loan restructuring. Different lenders impose varying fee structures that can substantially affect the total cost of borrowing. Some institutions might offer lower upfront fees but higher ongoing charges, while others provide more transparent, streamlined pricing models. Auckland homebuyers should meticulously compare these financial details, understanding that the cheapest headline rate doesn’t always represent the most cost-effective mortgage solution.

Compare fixed and floating interest rate mortgages in New Zealand at a glance:

| Rate Type | Key Benefit | Main Trade-Off | Best For |

|---|---|---|---|

| Fixed Rate | Predictable repayments | Less flexibility | Budget-conscious buyers |

| Floating | Adaptable to rate drops | Can rise unexpectedly | Those seeking flexibility |

Pro tip: Request a comprehensive breakdown of all potential fees and charges from each lender, ensuring you understand the complete financial commitment before making a final decision.

Low Deposit Options and Special Programs

Home ownership can seem challenging for first-time buyers with limited savings, but New Zealand’s mortgage market offers a range of innovative low deposit options designed to help Auckland residents overcome traditional financial barriers. These specialised programs recognise the increasing difficulty young professionals face when attempting to enter the property market.

Low deposit home loan strategies have become increasingly sophisticated, enabling borrowers to secure mortgages with deposits as low as 5-10% instead of the traditional 20% requirement. Government-backed schemes play a crucial role in this landscape, providing guarantees and support mechanisms that enable lenders to offer more accessible financing options. Some programs specifically target first-home buyers, offering reduced interest rates, shared equity arrangements, or additional financial support to help overcome initial deposit challenges.

Different lenders approach low deposit lending with unique criteria, creating a diverse ecosystem of opportunities. Some institutions require mortgage insurance for loans under 20% deposit, while others have developed specialised lending products that mitigate their risk through alternative assessment methods. Auckland homebuyers should carefully evaluate these options, understanding that each low deposit program comes with specific eligibility requirements, potential additional costs, and varying approval processes.

Pro tip: Consult a mortgage broker who specialises in low deposit options to help you navigate the complex range of programs and identify the most suitable pathway for your specific financial situation.

Risks, Pitfalls and How to Maximise Savings

Mortgage borrowing represents a significant financial commitment that demands careful navigation and strategic planning. While home ownership is an exciting prospect, potential borrowers must understand the complex landscape of risks and opportunities inherent in selecting the right lending pathway.

Mortgage cost management strategies involve more than simply selecting the lowest advertised interest rate. Hidden costs and potential financial pitfalls can dramatically impact long-term affordability. Borrowers must consider factors like establishment fees, potential break fees, interest rate fluctuations, and the implications of different loan structures. Some risks include variable interest rates that can unexpectedly increase, complex loan terms that might include penalty clauses, and lending conditions that could restrict financial flexibility.

Maximising savings requires a proactive and informed approach. Strategic techniques include making more frequent repayments, exploring opportunities to refinance at more competitive rates, and maintaining a comprehensive understanding of your loan’s specific terms. Auckland homebuyers should also consider building a financial buffer, understanding how extra repayments can reduce overall interest costs, and regularly reviewing their mortgage against current market conditions to ensure they’re not overpaying.

Pro tip: Create a detailed spreadsheet tracking all potential mortgage costs, including both obvious and hidden expenses, to gain a comprehensive view of your true borrowing expenditure.

Find the Best Auckland Mortgage by Comparing Lenders With Expert Help

Navigating Auckland’s mortgage market can feel overwhelming with all the variations in interest rates, fees and lending criteria discussed in the article. You want more than just the lowest rate you want a mortgage tailored to your unique financial situation including low deposit options flexibility and transparent costs. This is where Mortgage Managers make a real difference. As local mortgage advisers based in Hobsonville, we specialise in comparing a wide range of lenders to find the best fit for you whether you are self-employed a first-home buyer or an experienced investor.

Take control of your home loan journey now by tapping into our expert knowledge and personalised approach. Our Auckland mortgage advisers can help you understand all the fine details so you avoid costly pitfalls and maximise savings. Don’t wait weeks stressing over confusing loan terms start your mortgage comparison with Mortgage Managers today and get tailored guidance from professionals who know the local market. Check out how we compare lenders for you at our website and make your home loan decision with confidence.

Frequently Asked Questions

Why is it important to compare lenders when considering a mortgage?

Comparing lenders helps you find the most suitable mortgage for your financial situation, not just the lowest interest rate. It allows for a thorough evaluation of loan conditions, fees, and lender reputations, which can significantly impact your long-term financial commitment.

What factors should I consider when comparing mortgage lenders?

Key factors to consider include interest rates, establishment fees, ongoing charges, repayment flexibility, fixed versus floating rate options, and the lender’s customer service reputation and approval process.

How can a mortgage broker help in comparing lenders?

A mortgage broker can efficiently compare multiple lenders simultaneously and provide tailored recommendations based on your individual financial profile, helping to identify the loan products that best meet your needs.

What are the benefits of using non-bank lenders compared to traditional banks?

Non-bank lenders often offer more flexible lending criteria that can accommodate borrowers with non-traditional income sources or those who may not meet strict bank requirements. They can provide tailored lending options for specific financial situations, such as self-employed individuals or first-home buyers.