More than 30 percent of mortgage applicants in Australia turn to non-bank lenders when traditional banks set strict barriers. For many australian borrowers, accessing the right financial support can feel like a closed door, especially if they have unique income streams or recent credit issues. Understanding how non-bank lenders operate opens new pathways for people who need flexible loan options and faster approval times, especially when mainstream institutions fall short.

Table of Contents

- What Is A Non-Bank Lender?

- Types Of Non-Bank Lenders In New Zealand

- How Non-Bank Lending Works For Home Loans

- Eligibility Criteria And Application Process

- Benefits And Risks Of Non-Bank Lenders

- Non-Bank Lenders Versus Traditional Banks

Key Takeaways

| Point | Details |

|---|---|

| Non-Bank Lenders | Non-bank lenders offer flexible alternative financing solutions for borrowers who may not qualify for traditional bank loans, utilising diverse funding sources. |

| Types of Non-Bank Lenders | Non-bank lenders in New Zealand are categorised into deposit takers and non-deposit takers, each providing specific services like personal loans and property finance. |

| Flexible Eligibility Criteria | These lenders assess a broader range of financial circumstances, allowing for more accessible loan options for borrowers with unique financial situations. |

| Benefits and Risks | While non-bank lenders provide personalised solutions and faster approval, they may charge higher interest rates and have less regulatory oversight compared to traditional banks. |

What Is a Non-Bank Lender?

When traditional banks say no, non-bank lenders become a powerful alternative for borrowers seeking financial support. According to Reserve Bank of New Zealand, these financial institutions provide loans without relying on customer deposits, instead utilising diverse funding sources like wholesale markets and private investors.

Non-bank lenders operate differently from traditional banks, offering more flexible lending criteria that can benefit borrowers who might not qualify for standard bank loans. As Canstar explains, while these lenders must comply with the Credit Contracts and Consumer Finance Act, they have less regulatory restrictions, allowing for more innovative lending approaches.

Their financial products span various categories, including:

- Residential mortgages

- Personal loans

- Property development finance

- Low deposit home loans

- Bad credit loan options

By tapping into alternative funding sources and maintaining more adaptable assessment processes, non-bank lenders provide critical financial pathways for New Zealanders who might otherwise struggle to secure lending through conventional banking channels.

Types of Non-Bank Lenders in New Zealand

New Zealand’s non-bank lending sector comprises diverse financial institutions offering flexible alternatives to traditional banking. According to the Reserve Bank of New Zealand, these lenders are primarily categorised into two main groups: deposit takers and non-deposit takers.

Deposit takers include finance companies, credit unions, and building societies that accept public deposits. Non-deposit takers, by contrast, secure funding through alternative methods such as securitisation, equity funding, and bond issuance. Our guide on non-bank lenders that mortgage brokers use provides deeper insights into these funding mechanisms.

The non-deposit taking sector is particularly diverse, specialising in various financial services:

- Personal loans

- Residential mortgages

- Property development finance

- Specialised lending for unique borrower circumstances

These non-bank lenders often fill critical gaps in the lending market, offering tailored solutions for borrowers who might not meet traditional banking criteria. By providing more flexible lending policies, they play a significant role in supporting New Zealand’s diverse financial ecosystem.

How Non-Bank Lending Works for Home Loans

Non-bank home lending represents a flexible alternative to traditional bank mortgage processes, offering unique pathways for borrowers with diverse financial backgrounds. Non-bank lenders give you options when your bank says ‘no’, providing specialised mortgage solutions that mainstream banks might typically overlook.

The home loan process with non-bank lenders differs significantly from traditional banking approaches. While traditional banks rely heavily on standard credit scoring and rigid income verification, non-bank lenders employ more nuanced assessment strategies. They consider broader financial contexts, including self-employment income, recent credit history improvements, and unique employment scenarios that conventional lenders might dismiss.

Key characteristics of non-bank home lending include:

- More flexible credit assessment criteria

- Personalised lending approaches

- Faster application and approval processes

- Tailored solutions for complex financial situations

- Competitive interest rates for alternative borrower profiles

These lenders essentially fill critical gaps in the mortgage market, offering lifelines to borrowers who might otherwise struggle to secure home financing. By maintaining more adaptable lending standards, non-bank lenders create opportunities for home ownership that extend well beyond traditional banking constraints.

Eligibility Criteria and Application Process

Non-bank lenders offer a more flexible approach to assessing borrower eligibility compared to traditional banking institutions. Bad credit loans and non-standard loans are specialised offerings that demonstrate the unique assessment strategies these lenders employ when evaluating potential borrowers.

The eligibility criteria for non-bank home loans typically encompass a broader range of financial circumstances. Unlike traditional banks, these lenders consider factors beyond standard credit scores, including recent income stability, current financial health, and potential for future earnings. They are particularly adept at evaluating borrowers with:

- Self-employed income

- Fluctuating income streams

- Recent credit history improvements

- Complex employment arrangements

- Unique personal financial situations

The application process with non-bank lenders is generally more streamlined and personalised. Applicants can expect a more comprehensive financial review that looks beyond traditional metrics. This approach often involves a detailed consultation to understand the individual’s complete financial picture, allowing for more tailored lending solutions that align with the borrower’s specific circumstances and goals.

Benefits and Risks of Non-Bank Lenders

Navigating the landscape of home lending involves carefully weighing potential advantages and drawbacks. Bank alternatives for home loans in New Zealand offer unique opportunities that come with their own set of considerations for borrowers.

The primary benefits of non-bank lenders include unprecedented flexibility in lending criteria, faster application processes, and personalised financial solutions. Borrowers with complex financial backgrounds often find these lenders more accommodating, particularly those with:

- Irregular income streams

- Recent credit history challenges

- Self-employment

- Unique employment arrangements

- Limited traditional credit documentation

However, potential risks require careful evaluation. Non-bank lenders typically charge slightly higher interest rates to compensate for their more flexible assessment approaches. Borrowers should also understand that while these lenders offer more accessible pathways to financing, they might have less stringent regulatory oversight compared to traditional banking institutions. This means borrowers must conduct thorough due diligence, carefully review loan terms, and ensure they fully comprehend the financial commitment before proceeding.

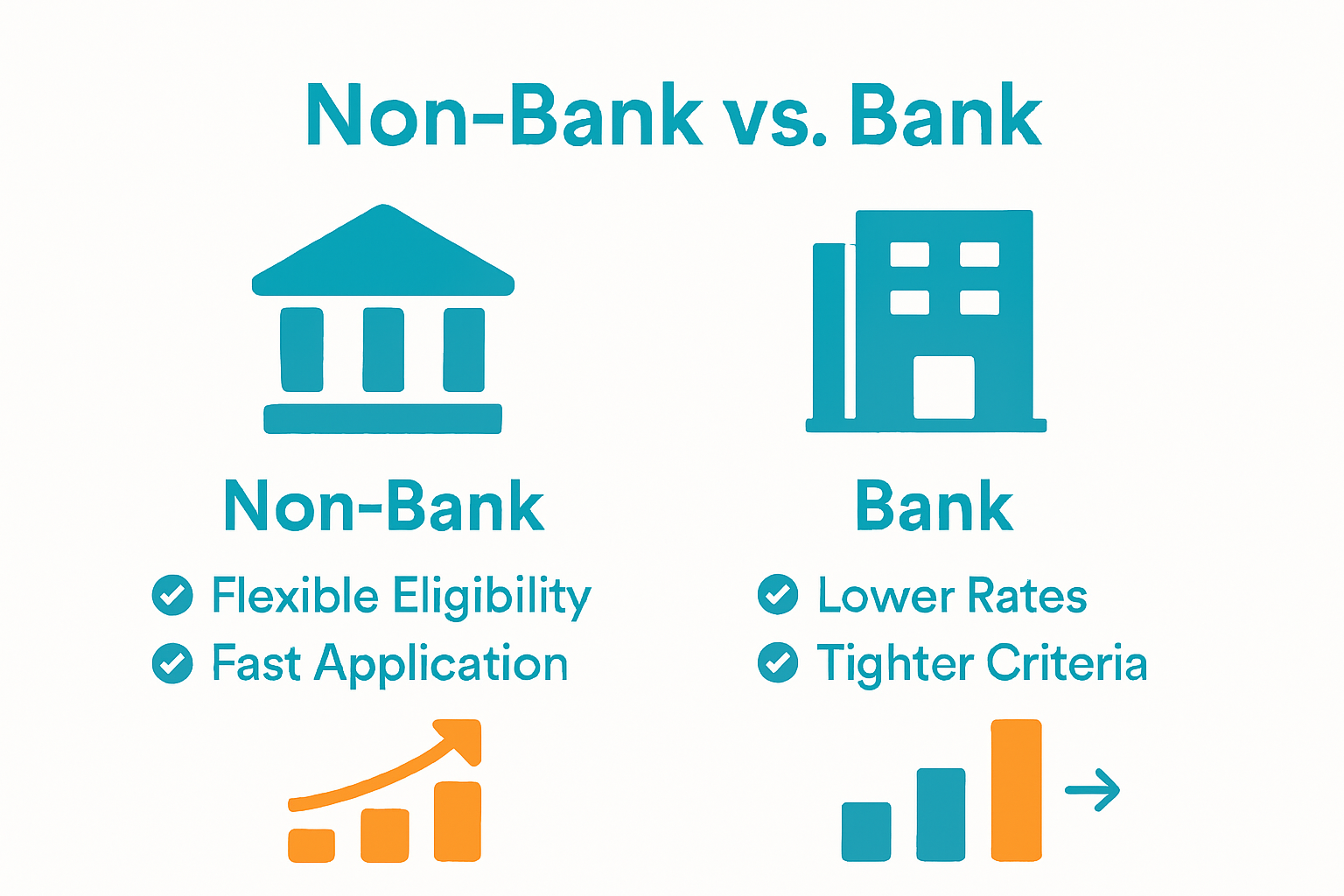

Non-Bank Lenders Versus Traditional Banks

Financial lending landscapes differ dramatically between non-bank lenders and traditional banks, each offering distinct approaches to borrower support. Banks are not the same, and mortgage brokers offer critical choice in navigating these complex financial pathways.

Traditional banks typically operate with rigid, standardised lending criteria that prioritise low-risk borrowers with extensive credit histories. In contrast, non-bank lenders adopt a more nuanced assessment approach, considering broader financial contexts and individual circumstances. Key differences include:

- Lending criteria flexibility

- Speed of application processing

- Range of acceptable income documentation

- Willingness to consider complex financial backgrounds

- Personalisation of lending solutions

While traditional banks offer lower interest rates and established reputations, non-bank lenders provide innovative solutions for borrowers who might not fit conventional lending moulds. This alternative approach creates financial opportunities for self-employed professionals, individuals with irregular income streams, and those recovering from past credit challenges, ultimately expanding access to home ownership and financial support.

Find the Right Home Loan with Expert Guidance on Non-Bank Lending

If you find yourself facing challenges securing a home loan from traditional banks due to complex financial situations or recent credit history issues non-bank lenders can offer valuable alternatives. The problem is navigating these flexible but less familiar lending options requires expert advice to ensure you get the best deal and avoid hidden risks. At Mortgage Managers we understand that every borrower has unique circumstances whether self-employed irregular income or bad credit and we specialise in connecting you with tailored solutions through trusted non-bank lenders.

When the usual banking criteria feel limiting we provide:

- Personalised financial assessments

- Access to a wide panel of non-bank lenders

- Clear guidance through a simplified application process

Ready to explore flexible lending options and secure your home loan with confidence? Visit Mortgage Managers for reliable mortgage advice designed to open doors when banks say no. Let our experienced mortgage advisers help you take control of your home buying journey today. Your path to home ownership is one conversation away.

Frequently Asked Questions

What is a non-bank lender?

Non-bank lenders are financial institutions that provide loans without relying on customer deposits. They utilise alternative funding sources such as wholesale markets and private investors to offer various lending products with more flexible criteria.

How do non-bank lenders differ from traditional banks?

Non-bank lenders operate with more flexible lending criteria and often assess borrowers’ financial situations in a more nuanced way. While traditional banks typically have strict requirements and common credit scoring methods, non-bank lenders consider a broader range of financial circumstances, including unique employment and income scenarios.

What types of loans can I get from non-bank lenders?

Non-bank lenders offer a variety of financial products, including residential mortgages, personal loans, property development finance, low deposit home loans, and options for borrowers with bad credit. Their offerings are designed to cater to individuals who might not qualify for standard bank loans.

What are the pros and cons of choosing a non-bank lender?

The benefits of non-bank lenders include flexible lending criteria, faster application processes, and tailored solutions for complex financial situations. However, they may charge higher interest rates and have less regulatory oversight than traditional banks, which means borrowers should conduct thorough due diligence before proceeding.