Most Auckland first home buyers underestimate the impact mortgage clauses can have on their loan security and future property rights. The difference between a solid financial footing and unexpected stress often rests in the fine print of your agreement. With more australian lenders entering the New Zealand market, these legal terms matter more than ever. This guide breaks down what mortgage clauses really mean, dispels common myths, and highlights how understanding each detail helps you make confident, informed decisions before you sign your home loan.

Table of Contents

- Mortgage Clause Meaning And Common Myths

- Key Types Of Mortgage Clauses In New Zealand

- How Mortgage Clauses Work In Property Insurance

- Legal Framework And Rights Of Lenders And Buyers

- Risks, Costs, And Common Mistakes To Avoid

Key Takeaways

| Point | Details |

|---|---|

| Understanding Mortgage Clauses | Mortgage clauses define the terms protecting both lenders and borrowers; knowing them aids in informed property investment. |

| Common Myths Dispelled | Mortgage clauses don’t automatically lead to property seizure after a missed payment; they outline multiple notifications and opportunities to rectify situations. |

| Engage Professionals | Always seek explanations from financial advisers and legal counsel regarding mortgage clauses to fully understand implications before signing. |

| Watch for Hidden Costs | Borrowers often overlook additional expenses, which can significantly increase financial burdens; thorough assessments are critical before commitment. |

Mortgage clause meaning and common myths

A mortgage clause represents a critical legal provision embedded within home loan agreements, defining the specific terms and conditions that protect both lenders and borrowers in property financing transactions. Understanding these clauses can help Auckland home buyers navigate potential financial pitfalls and make more informed decisions about their property investment.

Contrary to popular belief, mortgage clauses are not uniform across different lending institutions. The Real Estate Authority’s guidance clarifies crucial misconceptions about how these legal mechanisms operate, particularly when financial challenges emerge. Most home buyers mistakenly assume mortgage clauses only protect lenders, but they actually serve as balanced contractual safeguards that outline rights and responsibilities for both parties.

Common myths surrounding mortgage clauses include the misconception that they automatically trigger property seizure upon a single missed payment. In reality, these clauses typically provide multiple notification stages and opportunities for borrowers to rectify financial situations before more drastic actions are considered. Lenders are generally required to demonstrate reasonable attempts to work with borrowers experiencing temporary financial difficulties.

Professional Tip: Always request a comprehensive explanation of mortgage clauses from your financial adviser before signing any home loan agreement, ensuring you fully understand the potential implications of each provision.

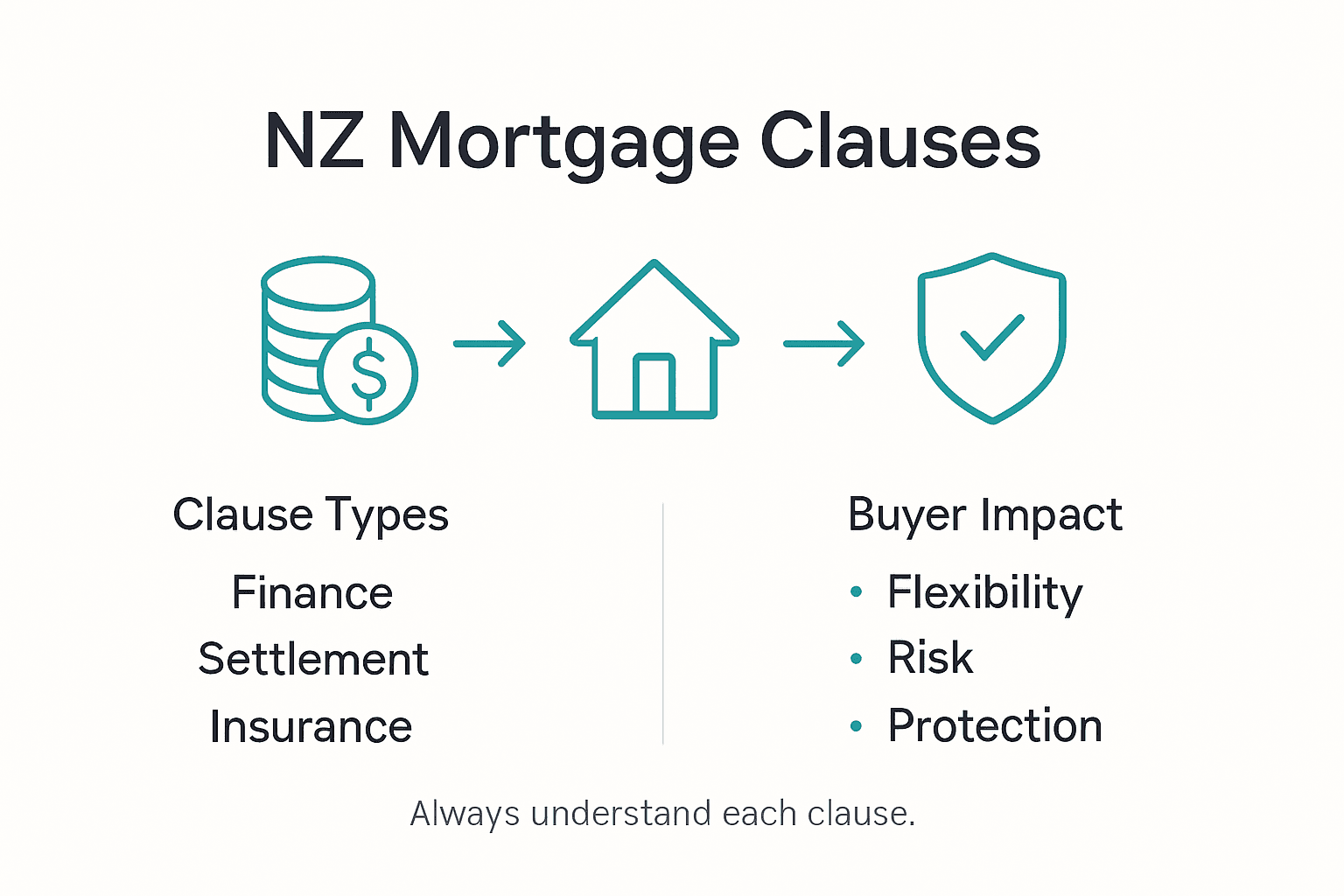

Key types of mortgage clauses in New Zealand

In the complex landscape of property financing, mortgage clauses serve as critical legal mechanisms that define the specific conditions and protections for both lenders and borrowers. The Real Estate Authority’s comprehensive guide outlines the primary types of mortgage clauses used in New Zealand property transactions, helping home buyers understand their contractual obligations and rights.

The primary mortgage clause types in New Zealand include finance clauses, due diligence clauses, settlement clauses, and default provisions. Finance clauses, for instance, provide buyers with protection by allowing them to withdraw from a property purchase if they cannot secure adequate loan funding. Due diligence clauses enable potential buyers to investigate property conditions, including building inspections, title searches, and council planning restrictions, before finalising the purchase.

Settlement clauses outline the specific timelines and conditions for property transfer, including deposit requirements, settlement date, and conditions under which either party can delay or cancel the transaction. Default provisions are particularly crucial, as they specify the exact circumstances under which a lender can take action if a borrower fails to meet their financial obligations, such as missed mortgage payments or breach of loan agreement terms.

Professional Tip: Always engage a qualified property lawyer to thoroughly review and explain each mortgage clause before signing any property purchase agreement, ensuring you fully understand your legal obligations and potential risks.

Here’s a summary of key mortgage clause types and their main purposes in New Zealand home lending:

| Clause Type | Main Purpose | Impact on Buyer |

|---|---|---|

| Finance Clause | Allows conditional withdrawal if funding fails | Reduces risk of losing deposit |

| Due Diligence Clause | Permits thorough property investigations | Empowers informed purchase |

| Settlement Clause | Sets timelines and transfer requirements | Clarifies payment obligations |

| Default Provision | Outlines consequences for missed obligations | Details steps before legal action |

How mortgage clauses work in property insurance

Property insurance represents a critical component of mortgage agreements, where insurance clauses serve as essential protective mechanisms for both lenders and homeowners. The Treasury’s comprehensive information sheet details how mortgage clauses directly influence property insurance requirements, establishing clear guidelines for risk management and financial protection.

Typically, mortgage insurance clauses mandate that homeowners maintain comprehensive property coverage that meets the lender’s specific requirements. These clauses specify minimum insurance standards, including total replacement value coverage, which ensures the property can be fully rebuilt or replaced in case of significant damage. The lender is usually named as the ‘interested party’ on the insurance policy, guaranteeing they have a legal claim to any insurance payouts that protect their financial investment.

The practical implementation of these clauses involves several key processes. When an insurance claim is lodged, the lender must be notified and may have rights to participate in claim settlement discussions. Insurance payouts are often structured to first satisfy the outstanding mortgage balance, with any remaining funds directed to the homeowner. This approach protects the lender’s financial interests while still providing necessary support to the property owner during challenging circumstances.

Professional Tip: Review your property insurance policy annually and ensure your mortgage clause requirements are consistently met, preventing potential contract breaches that could jeopardise your loan agreement.

Legal framework and rights of lenders and buyers

The legal landscape of mortgage agreements in New Zealand is complex, with detailed protections and obligations designed to balance the interests of both lenders and borrowers. Consumer Protection New Zealand provides comprehensive guidelines outlining the key legal duties of lenders under the Credit Contracts and Consumer Finance Act, establishing a robust framework for responsible lending practices.

Lenders have specific legal rights that include conducting thorough affordability assessments, requiring full financial disclosure, and maintaining the ability to enforce mortgage terms if borrowers default. These rights are counterbalanced by strict obligations to act transparently and ethically. Buyers are protected through mandatory disclosure requirements, which compel lenders to provide clear, comprehensible information about loan terms, interest rates, potential fees, and the implications of failing to meet contractual obligations.

The legal framework also establishes precise procedures for addressing potential disputes. If a borrower encounters financial difficulties, lenders must follow regulated processes that include providing formal notifications, offering potential restructuring options, and demonstrating reasonable attempts to work with the borrower before pursuing more drastic actions like mortgagee sales. These provisions ensure that borrowers are not arbitrarily penalised and have opportunities to rectify financial challenges.

Professional Tip: Obtain independent legal advice before signing any mortgage agreement to fully understand your rights, potential risks, and the specific legal protections available to you as a borrower.

Risks, costs, and common mistakes to avoid

Mortgage agreements involve substantial financial complexity, with numerous potential risks that can significantly impact home buyers. The Financial Markets Authority provides critical insights into the legal risks associated with mortgage contracts, highlighting the importance of understanding contractual obligations and potential financial consequences.

Common mistakes in mortgage agreements often stem from inadequate financial assessment and overlooking critical contractual details. Home buyers frequently underestimate the total cost of borrowing, failing to account for additional expenses like establishment fees, legal costs, and potential penalty interest rates. These hidden costs can dramatically increase the overall financial burden, transforming what seemed like an affordable mortgage into a challenging long-term commitment. Borrowers also frequently miscalculate their ability to maintain consistent repayments, particularly when facing potential changes in personal circumstances such as job loss or reduced income.

The most significant risks include defaulting on mortgage payments, which can lead to severe consequences like credit rating damage, mortgagee sales, and potential legal action. Other critical mistakes involve not fully understanding break fees for fixed-rate loans, neglecting to review interest rate structures, and failing to build sufficient financial buffers. Some buyers also mistakenly assume that verbal agreements or promises have the same legal standing as written contract terms, which can lead to unexpected complications and financial exposure.

The following table highlights typical risks, costs, and consequences in mortgage agreements:

| Risk/Cost | What It Means for Borrowers | Potential Long-term Effect |

|---|---|---|

| Establishment Fees | Upfront charges for setting up loan | Higher initial cash outlay |

| Break Fees (Fixed Loans) | Penalties for early repayment | Unexpected additional expenses |

| Penalty Interest Rates | Elevated rates after missed payments | Rapidly increasing debt burden |

| Underestimating Expenses | Misjudging true repayment ability | Increased likelihood of default |

Professional Tip: Always maintain a comprehensive financial buffer of at least three to six months of mortgage repayments, and conduct thorough independent financial assessments before committing to any mortgage agreement.

Navigate Mortgage Clauses with Confidence in Auckland Home Buying

Understanding your mortgage clauses can feel overwhelming but recognising their impact on your loan and home insurance is vital to protect your future. Key challenges like grasping finance clauses, default provisions, and insurance requirements can create uncertainty and risk for Auckland buyers. You deserve clarity, tailored advice, and support to avoid costly mistakes and secure your dream home with confidence.

Partner with Mortgage Managers, local Auckland mortgage advisers based in Hobsonville, who specialise in helping you decode complex mortgage terms and navigate every step smoothly. Our expert guidance ensures you fully understand your contractual rights and risks, so you make decisions that protect your investment and peace of mind. Start your journey to stress-free home ownership today by visiting Mortgage Managers for personalised advice. Discover how our trusted services cover West Auckland, The North Shore, and remote areas across New Zealand by learning more on our main site. Don’t wait until uncertainties cost you more get expert support now and move forward with confidence.

Frequently Asked Questions

What is a mortgage clause?

A mortgage clause is a key legal provision in home loan agreements that outlines the rights and responsibilities of both lenders and borrowers, protecting both parties in property financing transactions.

Do mortgage clauses only protect lenders?

No, mortgage clauses are designed to protect both lenders and borrowers by outlining contractual safeguards and specific terms that apply in various situations, including defaults and financial difficulties.

What should I know about default provisions in mortgage clauses?

Default provisions specify the circumstances under which a lender can take action if a borrower fails to meet financial obligations, providing a structured process that typically involves notifications and opportunities to rectify situations before drastic actions are taken.

How do mortgage clauses affect my property insurance requirements?

Mortgage clauses often require homeowners to maintain specific insurance coverage that meets the lender’s standards, ensuring that the property is sufficiently protected and that any insurance payouts prioritize the lender’s financial interests.