More than 60 percent of australian home buyers rely on mortgages to secure their dream property, yet many feel lost when navigating the choices. Understanding how mortgages work and the options available can make the difference between lasting financial security and costly mistakes. This guide unpacks the key mortgage concepts, local requirements, and the hidden costs to help you approach every step of the process with confidence.

Table of Contents

- Mortgage Basics and Core Concepts Defined

- Types of Mortgages in New Zealand

- How the Mortgage Process Works Locally

- Eligibility, Deposit, and Documentation Needed

- Costs, Risks, and Key Obligations Explained

Key Takeaways

| Point | Details |

|---|---|

| Understanding Mortgages | A mortgage allows individuals to purchase property by borrowing money, using the property as security. Key components include principal, interest rate, loan term, and security. |

| Types of Mortgages | New Zealand offers various mortgage options including fixed-rate, floating-rate, revolving credit, and interest-only loans, each catering to different financial needs. |

| Mortgage Process | The mortgage application process involves financial assessment, pre-approval, and property valuation, requiring careful evaluation of financial readiness. |

| Costs and Risks | Mortgages involve ongoing costs such as monthly repayments and insurance, alongside risks like interest rate fluctuations and potential job loss, necessitating robust financial strategies. |

Mortgage Basics and Core Concepts Defined

A mortgage is a financial instrument that enables individuals to purchase property by borrowing money from a lender while using the property itself as security. According to Settled, a mortgage is a loan secured against a property, allowing people to buy homes by borrowing funds and repaying them over time with interest.

Understanding the core components of a mortgage is crucial for potential homebuyers. A typical mortgage includes several key elements: the principal (the total amount borrowed), interest rate (the cost of borrowing), loan term (duration of repayment), and the security (the property itself). Consumer Protection highlights that mortgage decisions involving lenders, interest rates, and repayment structures can significantly impact long-term financial commitments.

Mortgages generally fall into different categories based on structure and purpose:

- Fixed-rate mortgages: Interest rate remains constant for a set period

- Variable-rate mortgages: Interest rate fluctuates with market conditions

- Interest-only mortgages: Borrowers pay only interest for an initial period

- Revolving credit mortgages: Allows flexible repayments and credit access

Successful mortgage management requires careful planning and understanding of your financial landscape. By choosing the right mortgage structure, you can create a home loan strategy that aligns with your financial goals and provides long-term stability.

Types of Mortgages in New Zealand

New Zealand offers a diverse range of mortgage options designed to meet various financial needs and preferences. Consumer Protection highlights that the mortgage landscape includes multiple types, each with unique characteristics tailored to different financial situations.

The primary mortgage types in New Zealand include:

- Fixed-Rate Mortgages: Interest rates remain constant for a predetermined period, typically 1-5 years

- Floating-Rate Mortgages: Interest rates fluctuate with market conditions, offering more flexibility

- Revolving Credit Mortgages: Combines mortgage and transaction account, allowing borrowers to offset interest

- Interest-Only Mortgages: Borrowers pay only interest for an initial period, reducing short-term repayment obligations

Settled emphasizes that choosing the right mortgage depends on individual financial circumstances, risk tolerance, and long-term financial goals. Different mortgage structures offer unique advantages, making it crucial to understand each option’s potential impact on your financial planning.

To find the most suitable mortgage for your specific needs, exploring the best mortgage type with a professional mortgage adviser can provide personalized insights and help you make an informed decision about your home loan strategy.

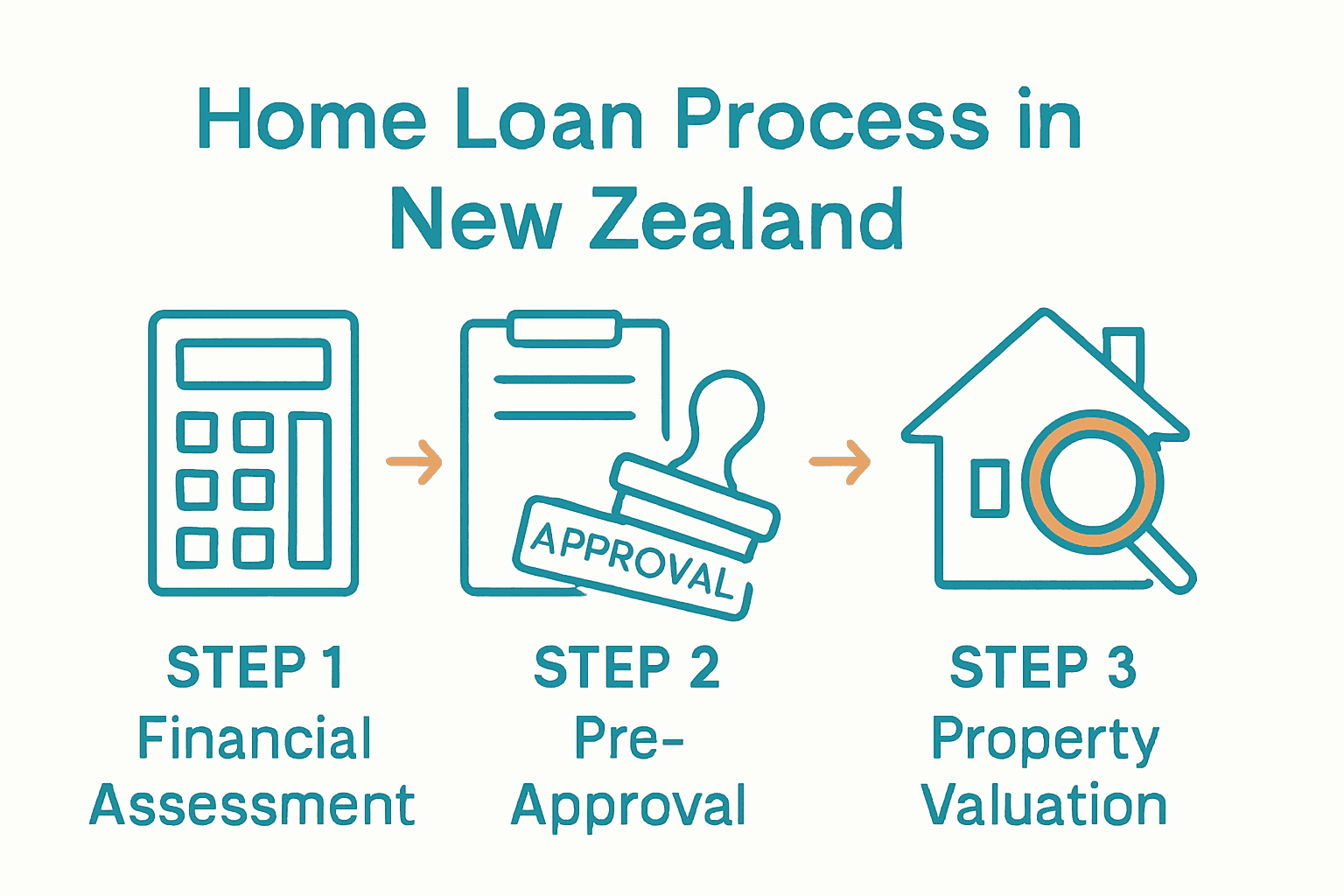

How the Mortgage Process Works Locally

Mortgage applications in New Zealand involve a structured process designed to assess financial readiness and property suitability. Settled outlines that the mortgage journey typically encompasses obtaining pre-approval, selecting an appropriate loan type, and completing the purchase with comprehensive legal and financial considerations.

The local mortgage process generally follows these key stages:

- Financial Assessment

- Evaluate personal income and expenses

- Check credit history and score

- Determine borrowing capacity

- Pre-Approval

- Submit initial application

- Receive conditional lending offer

- Understand maximum borrowable amount

- Property Valuation

-

Lender conducts property assessment

-

Confirms property meets lending criteria

-

Validates purchase price

Consumer Protection emphasizes the critical importance of understanding lender options and thoroughly assessing financial circumstances before making a commitment.

Navigating this complex process can feel overwhelming, which is why finding a good local mortgage broker can provide personalized guidance and simplify your home loan journey. A professional mortgage adviser can help you understand each step, interpret lender requirements, and increase your chances of successful mortgage approval.

Eligibility, Deposit, and Documentation Needed

Mortgage eligibility in New Zealand involves a comprehensive assessment of an individual’s financial health and capacity to repay a home loan. Settled highlights that potential borrowers typically need a deposit of at least 20% of the property’s value, accompanied by extensive financial documentation.

Key documentation requirements for mortgage applications include:

-

Personal Identification

- Valid passport or driver’s licence

- Proof of residential address

- Tax identification number

-

Financial Documentation

- Last 3 months of bank statements

- Proof of income (payslips, tax returns)

- Detailed list of existing debts and financial obligations

- Employment verification

Sorted emphasizes that lenders meticulously assess borrowing capacity by evaluating income stability, existing debt levels, and comprehensive credit history. This thorough examination helps determine the maximum loan amount and individual lending risk.

For those struggling to meet traditional deposit requirements, getting a home loan with a 5% deposit might be possible through specialized lending options. Working with a mortgage adviser can help you navigate these alternative pathways and understand the specific criteria for low-deposit home loans.

Costs, Risks, and Key Obligations Explained

Mortgage costs extend far beyond the initial property purchase, involving a complex financial landscape of ongoing expenses and potential risks. Consumer Protection highlights that mortgages entail multiple financial components, including interest payments, administrative fees, and potential penalty charges that can significantly impact long-term financial planning.

Key financial obligations and potential risks include:

-

Recurring Costs

- Monthly principal and interest repayments

- Property insurance premiums

- Council rates and maintenance expenses

-

Potential Financial Risks

- Interest rate fluctuations

- Property value depreciation

- Unexpected income reduction

- Job loss or economic instability

Sorted emphasizes the importance of developing robust strategies to manage mortgage risks, including maintaining emergency savings and understanding how interest rate changes can impact overall financial stability.

To protect yourself from potential financial challenges, reviewing a simple financial checklist can provide crucial insights into managing your mortgage effectively and maintaining long-term financial resilience.

Take Control of Your Home Loan Journey with Expert Guidance

Understanding what a mortgage truly involves can feel overwhelming. The article clearly highlights challenges such as grasping different mortgage types, navigating eligibility and deposit requirements, managing ongoing costs, and protecting against financial risks. These pain points can leave many homebuyers uncertain about which mortgage structure suits their financial situation or how to confidently proceed through the local mortgage process.

Mortgage Managers is here to help you turn confusion into clarity. As trusted Auckland mortgage advisers based in Hobsonville, we specialise in personalised home loan strategies tailored to your unique goals. Whether you need expert advice on choosing the right mortgage structure or want to explore options like getting a home loan with a 5% deposit, we guide you every step of the way.

Take the stress out of managing your mortgage and protect your future with professional support from a team that understands local lending criteria and financial landscapes.

Discover how we can simplify your journey starting today

Ready to find the home loan that fits your dreams and budget? Visit Mortgage Managers now and connect with a local mortgage adviser who puts your needs first.

Frequently Asked Questions

What is a mortgage?

A mortgage is a loan secured against a property, allowing individuals to borrow money to purchase a home while using the property itself as collateral for the loan.

What are the main types of mortgages?

The main types of mortgages include fixed-rate mortgages, floating-rate mortgages, revolving credit mortgages, and interest-only mortgages, each offering different repayment structures and flexibility.

What documentation do I need to apply for a mortgage?

Key documentation required for a mortgage application includes personal identification, proof of income, bank statements, and details of existing debts to assess your financial health and eligibility.

What costs should I consider when taking out a mortgage?

When taking out a mortgage, consider ongoing costs such as monthly repayments, property insurance premiums, council rates, and maintenance expenses, along with potential risks like interest rate fluctuations and changes in your financial situation.