More than half of first-time homebuyers in New Zealand find the mortgage approval process confusing and stressful and that’s why we have written this article about the mortgage approval process guide NZ home loans.

This guide will explain what the banks and non-bank lender are looking at when assessing and looking to approve a NZ home loan.

A home loan is usually the largest financial commitment most people ever make, so understanding every step matters. With careful preparation and clear knowledge of lender expectations, you can turn an overwhelming process into a straightforward path to home ownership while avoiding common setbacks.

Table of Contents

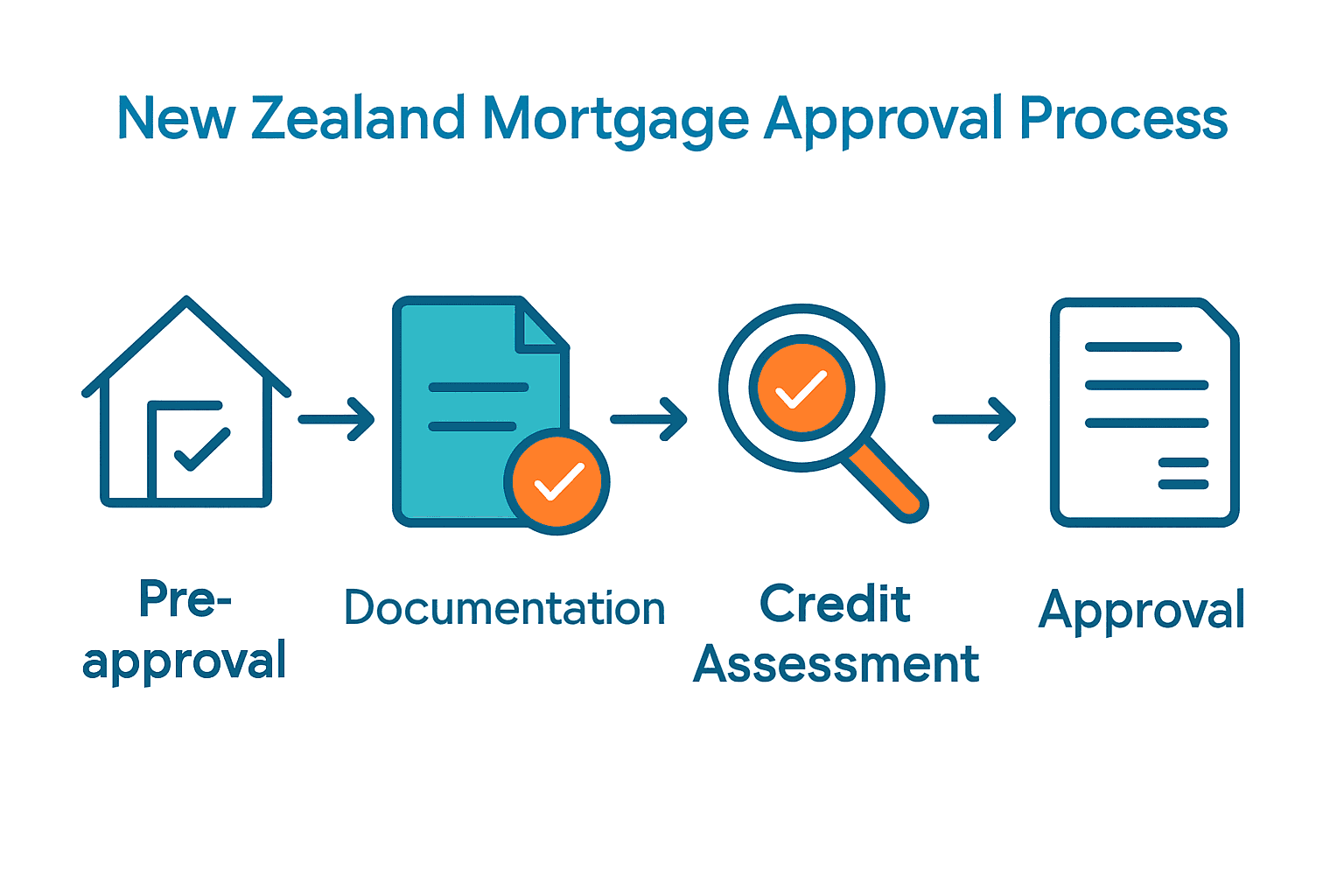

- Understanding The Mortgage Approval Process

- Essential Documentation And Eligibility Criteria

- Types Of Home Loans In New Zealand

- Credit Assessment And Approval Stages

- Common Obstacles And How To Overcome Them

Key Takeaways (for Mortgage Approval Process Guide NZ)

| Point | Details |

|---|---|

| Mortgage Pre-Approval is Essential | Start the mortgage process by obtaining pre-approval to understand borrowing limits and enhance your credibility with sellers. |

| Comprehensive Documentation is Crucial | Gather necessary financial documents to present a clear picture of your financial health, increasing your chances of approval. |

| Understand Various Loan Types | Familiarize yourself with different home loan options (e.g., fixed-rate, floating-rate) to choose the best fit for your financial situation. |

| Address Common Obstacles Proactively | Tackle potential challenges, such as credit issues or high debt, by improving your financial profile and seeking professional guidance. |

Understanding the Mortgage Approval Process

Navigating the mortgage approval process can feel like solving a complex puzzle, but breaking it down step by step makes the journey more manageable. According to Luminate Insights, the mortgage pre-approval process is a critical first step for potential homebuyers in New Zealand. This initial stage helps you understand exactly how much you can borrow and demonstrates to sellers that you’re a serious, financially prepared buyer.

The mortgage approval process typically involves several key stages that lenders use to assess your financial health and borrowing capacity. Financial documentation plays a crucial role in this evaluation. Lenders will carefully review your income, expenses, credit history, and existing financial commitments. Stuart Wills highlights that this assessment can be particularly nuanced for applicants with complex financial structures like family trusts or Look-Through Companies (LTCs).

To increase your chances of mortgage approval, you’ll want to prepare thoroughly:

- Gather comprehensive financial records

- Check and improve your credit score

- Save for a substantial deposit (typically 10-20% of the property value)

- Demonstrate stable employment and income

- Minimise existing debts and financial obligations

If you want expert guidance through this process, our guide on preparing a mortgage application provides detailed insights into creating a strong application that improves your approval odds. Remember, every lender has unique criteria, so understanding their specific requirements can significantly enhance your mortgage application’s success.

Essential Documentation and Eligibility Criteria

Preparing for a mortgage application requires meticulous documentation and understanding of lender eligibility requirements. Luminate Insights emphasises that gathering the right paperwork is crucial for a successful mortgage application. Lenders will typically require a comprehensive set of documents that provide a clear picture of your financial health and capacity to repay the loan.

The essential documentation typically includes:

- Proof of income (pay slips, tax returns, employment verification)

- Bank statements covering the last 3-6 months

- Proof of deposit and savings history

- Valid government-issued identification (passport or drivers licence)

- Details of existing debts and financial commitments

- Evidence of assets and investments

Note: the eligibility criteria can become more complex for applicants with unique financial structures. For instance, those operating through family trusts or Look-Through Companies (LTCs) will need to provide additional documentation demonstrating financial stability and income streams.

Eligibility typically hinges on several key factors:

- Credit score and credit history

- Stable employment with consistent income

- Debt-to-income ratio (usually under 40%)

- Sufficient deposit (typically 10-20% of property value)

- Age requirements (usually 18-70 years)

If you want to dive deeper into mortgage application preparation, our guide on mortgage brokers and bank criteria can provide additional insights into navigating the complex landscape of home loan applications.

First home buyers will often have less than the 10-20% deposit that the banks might want, but there are a number of low deposit options including the Kainga Ora First Home Loan where a 5% deposit is acceptable. The deposit criteria for new builds is more flexible with some banks allowing just 5% deposit and then there are options such as shared home ownership and AffordAssist which both start from just 5% deposit too.

Types of Home Loans in New Zealand

Navigating the home loan landscape in New Zealand requires understanding the diverse range of mortgage options available to potential homebuyers.

Fixed-rate mortgages and floating-rate mortgages represent the two primary loan types that form the foundation of most home financing strategies. Each comes with unique characteristics designed to meet different financial needs and risk tolerances.

The main types of home loans include:

- Fixed-Rate Mortgages: Offer stable interest rates for a set period (typically 1-5 years)

- Floating-Rate Mortgages: Have variable interest rates that fluctuate with market conditions

- Combination Loans: Split between fixed and floating rates for balanced risk management

- Interest-Only Loans: Allow borrowers to pay only interest for a specified period

- Low Deposit Home Loans: Designed for buyers with smaller initial deposits

Special considerations come into play for different borrower profiles. First-time homebuyers might find low deposit home loans particularly attractive, while investors might prefer more flexible lending options. There Are Bank Alternatives For Home Loans In New Zealand highlights that borrowers are no longer limited to traditional bank lending, with alternative financing options expanding in recent years.

Choosing the right home loan depends on multiple factors, including your financial situation, risk appetite, and long-term goals. Our guide on what makes a good home loan can provide deeper insights into selecting the most suitable mortgage type for your specific circumstances.

Remember, the best loan isn’t a one-size-fits-all solution but one that aligns perfectly with your unique financial landscape.

With NZ home loans the fixed loans will generally have lower interest rates and so most people want the majority of lending locked into these types of loans, and often split across a couple of fixed terms to lower the risk, BUT most people also want to pay their mortgage off faster and that can become a problem when using fixed loans. You therefore want to try and get approved with a bank that allows more flexibility with fixed loans – like the ability to pay up to 20% more without penalty, and to reduce to the minimum repayment at the click of a button (with no bank re-assessment) and even to have the ability to redraw money if you have paid in advance.

Very few banks offer this flexibility and so you need to speak with your mortgage adviser about the options and make sure that you are getting approved with a bank that can offer these features.

Credit Assessment and Approval Stages

Luminate Insights reveals that the mortgage credit assessment process is a comprehensive evaluation designed to protect both lenders and borrowers. Credit assessment involves a detailed examination of your financial health, looking beyond simple numbers to understand your overall financial reliability and capacity to repay a home loan.

The key stages of credit assessment typically include:

- Initial application review

- Credit score and history verification

- Income and employment validation

- Debt-to-income ratio calculation

- Asset and liability assessment

- Risk profiling

Lenders pay special attention to complex financial structures, particularly for applicants using family trusts or Look-Through Companies (LTCs). These unique scenarios require more nuanced financial documentation and potentially additional scrutiny.

Lenders evaluate several critical factors during the approval process:

- Consistency of income

- Length of employment

- Credit score (typically above 650 is preferred)

- Existing debt levels

- Repayment history

- Stability of financial circumstances

For those navigating more challenging credit scenarios, our guide on bank alternatives for home loans can provide alternative pathways to securing mortgage financing. Understanding these assessment stages helps you prepare a stronger, more compelling application that increases your chances of approval.

Common Obstacles and How to Overcome Them

Luminate Insights highlights that mortgage applications frequently encounter challenging roadblocks that can derail even the most promising home ownership dreams. Credit challenges represent the most significant hurdle for many potential borrowers, with complex financial histories often creating unexpected barriers to mortgage approval.

Common obstacles in the mortgage application process include:

- Poor credit score or limited credit history

- High debt-to-income ratio

- Inconsistent employment history

- Insufficient savings for deposit

- Complex income structures

- Previous financial defaults or bankruptcies

Stuart Wills emphasises that applicants with unique financial situations – such as those using family trusts or Look-Through Companies – face additional scrutiny. These complex financial structures require more comprehensive documentation and a strategic approach to demonstrating financial stability.

Strategies to overcome these obstacles include:

- Improving credit score through consistent bill payments

- Reducing existing debt

- Maintaining stable employment

- Building a robust savings history

- Preparing comprehensive financial documentation

- Seeking professional mortgage advice

If traditional lending paths seem challenging, our guide on bank alternatives for home loans can help you explore alternative financing options that might better suit your unique financial circumstances.

Take Control of Your Mortgage Approval Journey Today

Navigating the mortgage approval process can be overwhelming, especially when faced with challenges like complex income structures or tight credit requirements.

If you are aiming to secure your dream home but feel uncertain about meeting lender expectations or assembling the right documentation, you are not alone and should not try doing it alone either.

Understanding key steps such as credit assessment and financial eligibility are important, butt then choosing the right bank and loan type is critical too.

At Mortgage Managers, we specialise in guiding Auckland homebuyers through every stage of the mortgage journey. Based in Hobsonville with a deep understanding of the local West Auckland and Auckland’s North Shore markets, our expert mortgage advisers help simplify your options and tailor solutions to your unique financial situation. We operate remotely throughout the country offering NZ home loans from Northland to Southland.

Visit our website to discover how we prepare strong mortgage applications, explore bank alternatives for home loans when traditional options seem difficult, or learn about what makes a good home loan.

Don’t let the complexities hold you back.

Contact us now and take the first confident step toward securing your New Zealand home with expert support and advice.

Frequently Asked Questions

What is the mortgage approval process?

The mortgage approval process involves several key stages, including reviewing your financial documentation, assessing your credit history and employment stability, and determining your borrowing capacity. Lenders analyze these factors to gauge your ability to repay the loan.

What documentation do I need for a mortgage application?

Essential documentation typically includes proof of income, bank statements from the last 3-6 months, evidence of your deposit and savings history, valid ID, and a detailed account of existing debts and financial commitments.

How do lenders assess my creditworthiness for a mortgage?

Lenders assess your creditworthiness through a credit assessment process that includes verifying your credit score, validating your income and employment, calculating your debt-to-income ratio, and assessing your overall financial stability and reliability.

What common obstacles can affect my mortgage approval?

Common obstacles include a poor credit score, high debt-to-income ratio, inconsistent employment history, insufficient savings for a deposit, and complex income structures. Overcoming these challenges often requires strategic financial planning and preparation.

Other Recommended Articles

- Basic 101 On How To Apply For A Home Loan

- Unlocking the Door to Your First Home: How to Get a Mortgage in NZ – Mortgage Managers

- Learn How We Prepare A Mortgage Application

- The Non-Bank Lenders That Mortgage Brokers Use