Role of mortgage adviser in Auckland: expert guide 2026

Many Auckland homebuyers believe mortgage advisers simply add unnecessary costs to an already expensive process. In reality, 67% of Kiwis who switched banks used mortgage advisers, revealing their crucial role in securing competitive loans. For first-time buyers and those navigating credit challenges, advisers transform a confusing maze of lender requirements into a clear, manageable pathway to homeownership.

Table of Contents

- Role Of Mortgage Adviser In Auckland: Expert Guide 2026

- Understanding The Role Of A Mortgage Adviser In New Zealand

- How Mortgage Advisers Support First-Time Buyers And Those With Credit Challenges

- Common Misconceptions About Mortgage Advisers In New Zealand

- Mortgage Adviser Vs. Direct Application: Comparative Benefits

- How To Work Effectively With A Mortgage Adviser

- Partner With Auckland’s Trusted Mortgage Specialists

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Mortgage advisers simplify options | They navigate complex Auckland lending markets and match you with suitable lenders based on your unique financial situation. |

| First-time and credit-challenged buyers benefit most | Advisers negotiate lender criteria and structure loans to overcome barriers that direct applications often cannot. |

| Using advisers creates measurable advantages | Access to multiple lenders, faster approvals, and often better rates than applying directly to banks. |

| Not all advisers offer full market access | Some work with limited lender panels, so choosing the right adviser matters for getting genuinely competitive options. |

| Preparation maximises adviser value | Gathering financial documents and asking targeted questions ensures efficient collaboration and better outcomes. |

Understanding the role of a mortgage adviser in New Zealand

Mortgage advisers act as intermediaries between you and lenders, providing tailored loan options under strict legal standards. They assess your financial position, goals, and constraints to recommend suitable mortgage products from their lender panel. This personalised approach proves especially valuable in Auckland’s competitive property market, where timing and lender choice significantly impact your borrowing power.

Advisers operate under regulatory frameworks requiring transparency, suitability assessments, and disclosure of any conflicts of interest. They must prioritise your best interests when recommending products. Understanding the role of advisers in home buying helps you appreciate how these professionals navigate lender policies, interest rate structures, and application requirements that most borrowers find overwhelming.

Key functions mortgage advisers perform include:

- Conducting comprehensive financial assessments to determine borrowing capacity

- Comparing loan products across multiple lenders to identify optimal matches

- Managing application paperwork and liaising with lenders throughout approval processes

- Educating clients on mortgage terms, risks, and long-term financial implications

- Negotiating terms and advocating for clients with challenging financial profiles

When you find a mortgage broker in Auckland, you gain access to expertise that translates complex lending criteria into actionable strategies. Advisers stay current on lender policy changes, which shift frequently in response to economic conditions and regulatory updates. This knowledge proves invaluable for first-time buyers unfamiliar with documentation requirements or credit-challenged applicants needing creative loan structuring.

The Consumer NZ mortgage adviser guide emphasises that quality advisers provide market insights beyond what individual banks disclose. They understand which lenders favour certain borrower profiles, enabling strategic application placement that maximises approval chances whilst minimising wasted time on unsuitable lenders.

How mortgage advisers support first-time buyers and those with credit challenges

First-time buyers often struggle with understanding deposit requirements, KiwiSaver withdrawal processes, and how lenders assess income stability. Mortgage advisers negotiate lender criteria and improve approval chances for clients facing these obstacles. They customise loan structures to align with your employment type, income sources, and future financial plans.

For Auckland buyers with credit challenges, advisers become essential advocates. They know which lenders specialise in bad credit home loans and understand specific criteria each institution applies. Rather than facing multiple rejections through direct applications, you benefit from strategic positioning with lenders most likely to approve your circumstances.

Advisers streamline preapproval processes by:

- Identifying documentation requirements upfront to prevent delays

- Explaining how lenders calculate serviceability and deposit needs

- Recommending steps to strengthen applications before formal submission

- Managing communication with lenders to address queries quickly

- Providing realistic timelines and setting appropriate expectations

Pro Tip: Before meeting your adviser, review your credit report through Centrix or Equifax. Identifying issues early allows advisers to develop strategies addressing concerns proactively rather than reactively after lender rejections.

The emotional support advisers provide proves equally valuable. First-time buyers frequently feel overwhelmed by jargon-filled contracts and high-pressure sales tactics from some lenders. Having an experienced professional explain options objectively reduces stress and builds confidence throughout the process. Consumer NZ insights on mortgage advisers confirm that this guidance significantly improves borrower satisfaction and financial outcomes.

For those researching mortgage approval tips for bad credit, advisers offer practical pathways forward. They structure applications highlighting strengths whilst addressing weaknesses transparently, increasing lender trust. Understanding how to choose a financial adviser ensures you partner with professionals equipped to handle complex scenarios effectively.

Common misconceptions about mortgage advisers in New Zealand

Many homebuyers hesitate to use advisers based on myths that misrepresent their value and function. Research disproves beliefs that advisers add costs without savings, lack objectivity, or that banks offer better deals directly. Understanding reality helps you make informed decisions about engaging professional mortgage guidance.

Myth: Advisers charge fees that negate any potential savings. Reality: Most advisers receive commission from lenders, meaning no direct cost to you. Even when fees apply, the competitive rates and loan terms advisers secure typically exceed any charges. Banks often price identically for adviser-referred and direct clients, so using an adviser provides expert guidance without paying premium rates.

Myth: Banks offer better deals when you apply directly. Reality: Lenders maintain consistent pricing across channels to remain competitive. Banks value adviser relationships because brokers deliver pre-qualified applicants, reducing their acquisition costs. This efficiency often translates to faster processing and more flexible negotiations rather than better direct-customer pricing.

Myth: Advisers show bias towards specific lenders or limited options. Reality: Reputable advisers maintain broad lender panels and disclose any limitations upfront. However, some advisers do work with restricted lender groups, which can limit your options. Being informed about why use mortgage broker nz helps you ask the right questions about lender panel breadth during initial consultations.

Key realities about adviser objectivity include:

- Regulatory requirements mandate disclosure of commission structures and conflicts

- Quality advisers prioritise long-term client relationships over single-transaction commissions

- Transparent advisers explain why they recommend specific lenders for your situation

- You can request information about all lenders on their panel before proceeding

The Consumer NZ debunking myths resource emphasises that informed consumers who ask direct questions about fees, lender relationships, and service scope receive honest answers that clarify adviser value. Choosing advisers based on reputation, transparency, and demonstrated market knowledge ensures you benefit from genuine expertise rather than sales-focused guidance.

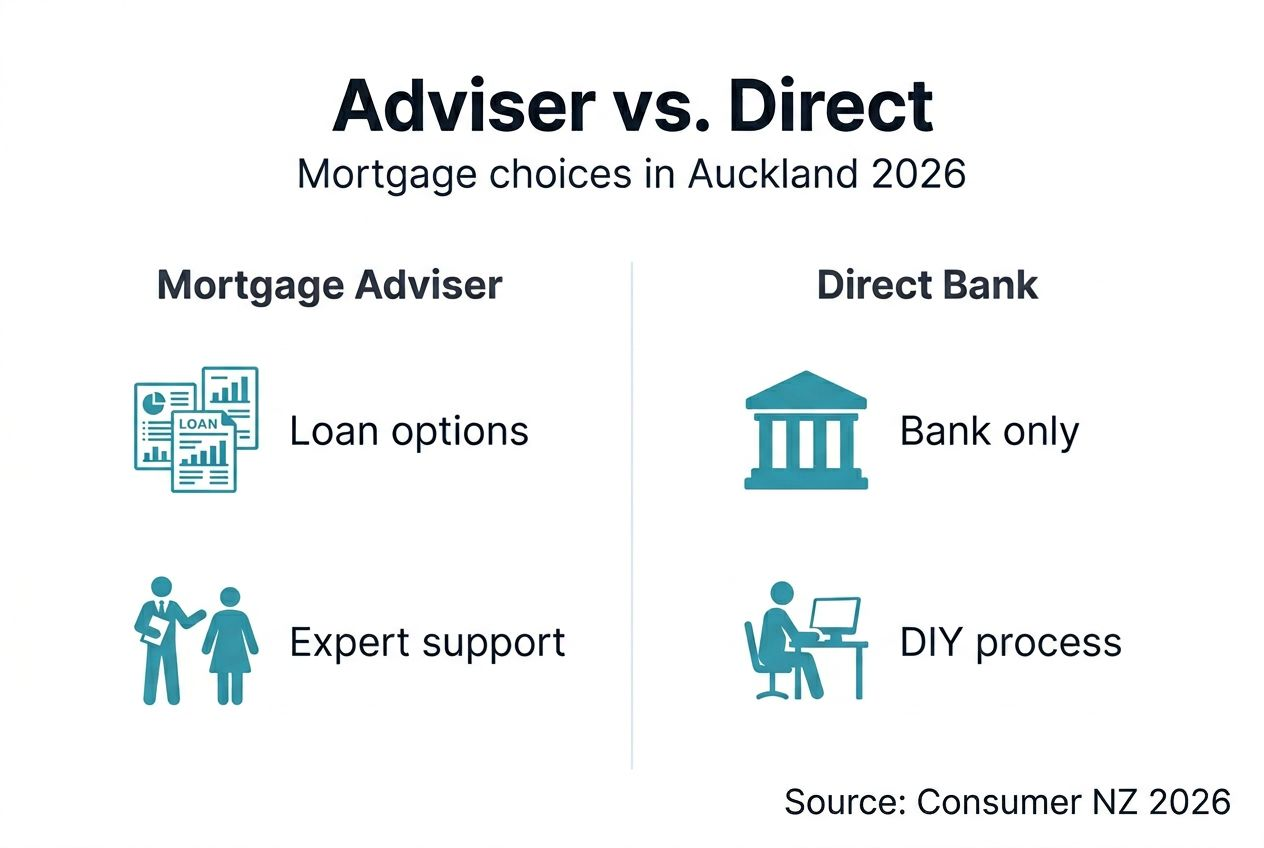

Mortgage adviser vs. direct application: comparative benefits

Understanding the practical differences between using an adviser and applying directly helps you choose the approach best suited to your knowledge, time availability, and financial complexity. The 67% of home loan customers who switched banks used mortgage advisers, demonstrating their effectiveness in accessing competitive options.

| Factor | Mortgage Adviser | Direct Bank Application |

|---|---|---|

| Lender Access | Multiple lenders compared simultaneously | Single lender’s products only |

| Personalised Guidance | Tailored recommendations based on full financial assessment | Generic product information without customisation |

| Time Investment | Adviser handles research, paperwork, and lender communication | You manage all research, applications, and follow-up |

| Approval Chances | Strategic lender matching improves success rates | Limited to one lender’s criteria and appetite |

| Cost | Typically no fee (lender-paid commission) or transparent charges | No direct cost but potentially higher rates without comparison |

| Market Knowledge | Current insights across lender policies and rate changes | Limited to marketing materials and branch staff knowledge |

| Complex Situations | Experience navigating credit issues and non-standard income | Standard criteria applied rigidly with limited flexibility |

Advisers provide access to non bank lenders mortgage brokers use, expanding options beyond mainstream banks. These alternative lenders often approve applications that banks decline, particularly for self-employed borrowers or those with imperfect credit histories. Direct applications limit you to whatever products your chosen bank offers, potentially missing better-suited alternatives.

Key advantages of adviser-facilitated applications:

- Simultaneous comparison of rates, fees, and terms across lenders

- Expert interpretation of complex lending policies and eligibility criteria

- Reduced application stress through professional paperwork management

- Access to wholesale rates and special lender promotions not publicly advertised

Pro Tip: Even if you ultimately apply directly, consulting an adviser initially provides market intelligence about competitive rates and terms. This knowledge strengthens your negotiating position with direct lenders.

Direct applications suit borrowers with straightforward finances, strong credit, and time to research multiple lenders independently. However, for Auckland’s competitive property market where speed and certainty matter, advisers deliver efficiency that often proves decisive. When you find a mortgage broker in Auckland, you essentially outsource the comparison shopping whilst retaining final decision authority.

The Consumer NZ mortgage adviser comparison confirms that adviser-assisted borrowers report higher satisfaction and better understanding of their mortgage terms. This educational component creates long-term value beyond the immediate transaction.

How to work effectively with a mortgage adviser

Maximising the value from your adviser relationship requires preparation and clear communication. Proper preparation and asking key questions about fees, lenders, and loan options ensures productive adviser relationships that deliver optimal outcomes efficiently.

Essential documents to prepare before your initial meeting:

- Recent payslips or proof of income for the past three months

- Bank statements showing savings, expenses, and account conduct

- Credit report from Centrix or Equifax to understand your credit position

- Identification documents including driver licence and proof of address

- Details of existing debts, assets, and financial commitments

Asking the right questions upfront establishes transparency and sets appropriate expectations. Understanding choosing a financial adviser helps you evaluate whether an adviser’s approach aligns with your needs.

Critical questions to ask during initial consultations:

- What is your lender panel size and which institutions do you work with?

- How are you compensated and are there any fees I need to pay directly?

- What is your experience with clients in similar financial situations to mine?

- What is the typical timeline from application to settlement?

- How will you communicate updates and what response times should I expect?

- What happens if my application faces challenges or requires restructuring?

- Do you provide ongoing support after settlement for refinancing or reviews?

The mortgage adviser process typically follows these steps:

- Initial assessment: Comprehensive review of your financial position, goals, and constraints

- Market comparison: Analysis of suitable lenders and products matching your profile

- Option presentation: Detailed explanation of recommended loans with pros, cons, and trade-offs

- Application submission: Preparation and lodgement of applications with chosen lender

- Progress management: Liaison with lender, addressing queries, and keeping you informed

- Settlement coordination: Final checks, documentation review, and loan drawdown

Communicating openly about your circumstances accelerates the process significantly. Advisers cannot help effectively if they lack complete information about income sources, credit history, or future plans. Transparency about concerns or constraints enables advisers to develop realistic strategies rather than pursuing unsuitable options.

The questions to ask mortgage advisers resource provides additional guidance on evaluating adviser expertise and service quality. Quality advisers welcome detailed questions and provide clear, jargon-free answers that demonstrate their knowledge and commitment to your interests.

Partner with Auckland’s trusted mortgage specialists

Navigating Auckland’s complex mortgage landscape requires expertise that transforms confusion into clarity. The strategies and insights we have explored demonstrate how professional mortgage guidance delivers measurable advantages for first-time buyers and those facing credit challenges.

Mortgage Managers brings localised Auckland market knowledge combined with access to comprehensive lender panels across New Zealand. Our Hobsonville-based team understands the unique challenges West Auckland, North Shore, and greater Auckland buyers face. We specialise in structuring solutions for complex financial situations, turning potential obstacles into pathways to homeownership. Whether you are navigating first-time buyer programmes, credit repair strategies, or non-standard income assessment, our advisers provide transparent guidance focused on your long-term financial success. Contact our team to discuss your specific circumstances and discover how strategic mortgage advice creates opportunities you might not access independently.

Frequently asked questions

What does a mortgage adviser actually do for Auckland homebuyers?

Mortgage advisers assess your financial situation, compare loan products across multiple lenders, and recommend suitable options based on your specific circumstances. They manage application processes, negotiate with lenders, and provide ongoing support throughout the approval and settlement journey.

Do mortgage advisers charge fees or cost extra compared to direct bank applications?

Most advisers receive commission from lenders, meaning no direct cost to you. When fees apply, they are disclosed upfront and often offset by the competitive rates and terms advisers secure. Banks typically price identically for adviser-referred and direct applicants.

Can mortgage advisers help with bad credit or complex financial situations?

Yes, advisers specialise in navigating challenging scenarios by matching you with lenders who accommodate credit issues, non-standard income, or unique circumstances. They structure applications strategically to maximise approval chances that direct applications often cannot achieve.

How do I choose the right mortgage adviser in Auckland?

Evaluate advisers based on lender panel breadth, experience with similar client situations, fee transparency, and communication approach. Ask about their regulatory compliance, request client references, and ensure they welcome detailed questions about their processes and recommendations.

How long does the mortgage application process take with an adviser?

Timelines vary based on application complexity and lender processing speeds, but advisers typically facilitate faster approvals through efficient documentation preparation and proactive lender communication. Expect four to six weeks from initial consultation to settlement for straightforward applications, longer for complex scenarios.