TL;DR:

- Equity is the portion of a property’s value that you own outright, not just cash savings.

- First home buyers can use family or own property equity as security to buy a home.

- Using equity wisely can help achieve homeownership faster, but carries legal and financial risks.

Many first home buyers in New Zealand believe that without a sizeable cash deposit sitting in a savings account, the property market is simply out of reach. That belief is understandable, but it’s also one of the most common misconceptions we see at Mortgage Managers. Home equity, whether your own or a family member’s, can be just as powerful a tool as cash when it comes to securing your first property. This guide walks you through what equity actually is, how it works in a home loan application, the practical ways you can use it, the benefits and risks to weigh up, and how the right adviser makes the whole process far less daunting.

Table of Contents

- What is equity and how does it work?

- Ways first home buyers can use equity to purchase property

- Benefits and risks of using equity in home buying

- How mortgage advisers help you make the most of your equity

- A fresh perspective on equity for first home buyers

- Move forward with expert mortgage advice

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Equity unlocks opportunities | You can use home equity as a powerful alternative to cash deposits when buying property in New Zealand. |

| Multiple ways to use equity | Options include tapping your own property or a family member’s, often with lender support. |

| Weigh risks before acting | Consider both the upsides and obligations before leveraging equity for your first home. |

| Expert advice is essential | Mortgage advisers help you make sense of options and avoid common pitfalls with equity. |

What is equity and how does it work?

Now that we’ve challenged the cash deposit myth, let’s break down what equity really means in plain terms.

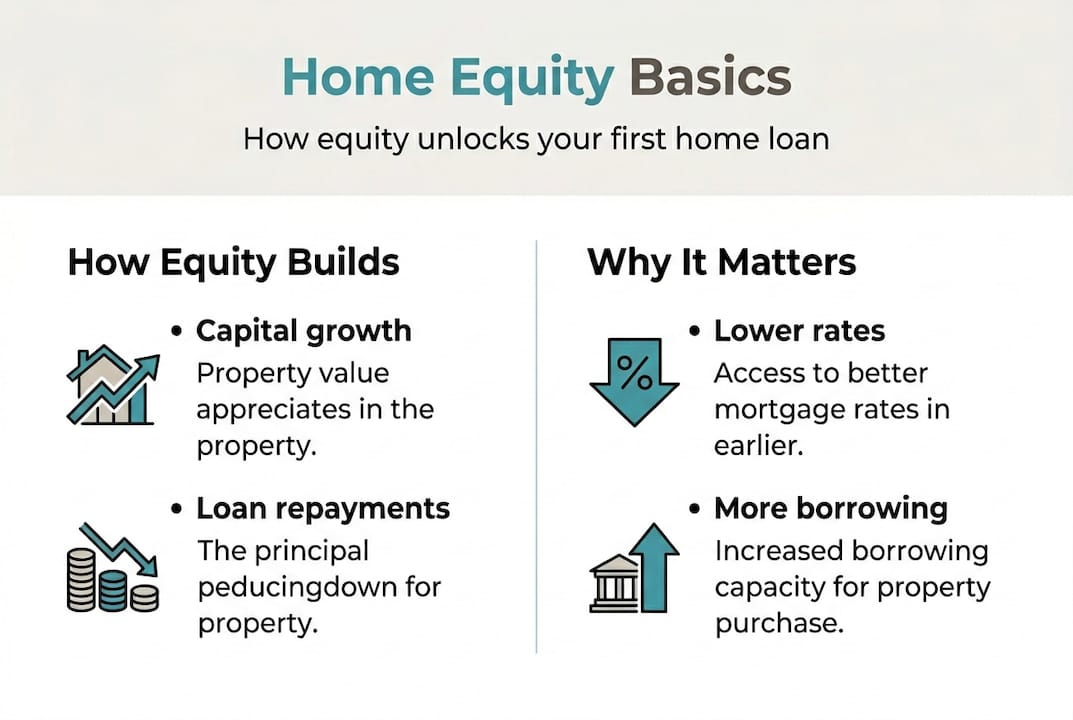

Home equity basics refers to the portion of a property’s value that you actually own outright. The formula is simple: property value minus any outstanding mortgage equals your equity. If your home is worth $700,000 and you owe $500,000, you have $200,000 in equity. That gap is real financial value, and lenders recognise it as such.

Equity builds in two main ways. First, as property values rise over time through capital growth, your equity increases even if your mortgage stays the same. Second, every regular mortgage repayment chips away at your outstanding balance, steadily growing the share of the property you own. For many New Zealand homeowners, these two forces work together to build equity faster than expected.

Here’s a simple illustration of how equity can grow over time:

| Year | Property value | Outstanding mortgage | Equity |

|---|---|---|---|

| 2022 | $700,000 | $560,000 | $140,000 |

| 2024 | $740,000 | $530,000 | $210,000 |

| 2026 | $780,000 | $500,000 | $280,000 |

For first home buyers, the most relevant types of equity are:

- Own equity: Equity you hold in an existing property, perhaps an investment property or a property you’ve inherited.

- Family equity: Equity held by parents or close relatives, offered as a guarantee or security.

- Built equity: Equity that grows naturally through repayments and capital appreciation over time.

It helps to think of equity as a currency in the property world. You can’t spend it at a supermarket, but a bank will treat it as genuine security when assessing your home loan application. That’s the key insight most first home buyers miss.

Pro Tip: Equity is not the same as cash, but lenders treat it as real, tangible value when you structure your loan correctly. The distinction matters when planning which assets to use in your application.

Ways first home buyers can use equity to purchase property

Having established what equity is, let’s look at the main ways you can actually use it to buy your first home.

There are two primary paths. The first is using equity from a property you already own. This is more common for people moving from one home to another, but it also applies to buyers who may have an interest in an existing property. The second, and arguably more relevant for genuine first home buyers, is using a family member’s equity as security through a guarantee arrangement.

A home loan with equity as the deposit works by offering a bank additional security over another property rather than providing cash upfront. Here is how the process typically unfolds:

- Assess available equity. You or your family member calculates how much usable equity exists in the guarantor property.

- Speak with a mortgage adviser. An adviser checks lender criteria and confirms whether the equity qualifies as security.

- Obtain a property valuation. The lender will require a registered valuation on the guarantor property.

- Structure the loan. The adviser structures the loan so the guarantee covers only the shortfall, not the entire mortgage.

- Submit the application. The full application goes to the lender with the equity guarantee in place.

- Settlement. Once approved, you complete the purchase without needing a large cash deposit.

Here’s a quick comparison of using equity versus cash for a deposit:

| Factor | Cash deposit | Equity guarantee |

|---|---|---|

| Source | Savings | Property value |

| Impact on liquidity | Reduces savings | Preserves cash |

| Lender acceptance | Universal | Lender-specific |

| Risk profile | Lower | Moderate |

| Setup complexity | Simple | Requires structuring |

A real-world example: a couple in Auckland wants to buy a $750,000 home but only has $30,000 saved. Their parents have $350,000 in equity in their own mortgage-free home. By using releasing equity options to set up a family guarantee, the couple can meet the lender’s security requirements without draining the family’s savings.

Benefits and risks of using equity in home buying

With these methods in mind, it’s crucial to weigh up the main benefits and risks of using equity before committing to this approach.

The benefits are genuine and significant. When you reach or can demonstrate benefits of reaching 20% equity, you typically access lower interest rates and avoid low equity margins, which are surcharges lenders add when your deposit is below 20%. Using equity strategically can get you to that threshold faster.

Key benefits include:

- Lower interest rates through avoiding low equity pricing on your loan.

- Faster market entry without waiting years to save a full cash deposit.

- Preserved liquidity because your cash savings stay intact for renovations, emergencies, or other needs.

- Greater flexibility in negotiating loan structures with the right lender.

- Family support that is structured legally and safely through a guarantee arrangement.

However, the risks are equally real and worth understanding clearly.

In New Zealand, buyers using a family equity guarantee put the guarantor’s property at risk if repayments cannot be met. This is a serious legal and financial commitment for all parties involved.

Signs equity may not be the right approach for you right now:

- Your income does not comfortably service the full loan amount.

- The guarantor property already carries a large mortgage of its own.

- Family relationships may not withstand the financial pressure of a guarantee arrangement.

- You haven’t yet sought independent legal advice for the guarantor.

Pro Tip: Before using family equity, every party should seek independent legal and financial advice. Lenders will often require this as part of their approval process, so it’s not optional.

The refinancing benefits of building your own equity over time are also worth noting. Once your loan-to-value ratio improves, you gain real leverage to refinance on better terms, which reduces the long-term cost of your mortgage considerably.

How mortgage advisers help you make the most of your equity

To avoid taking unnecessary risks and maximise your chance of success, it pays to know where a good adviser can help.

A skilled role of a mortgage adviser is far more than a form-filler. When equity is involved, the structuring of your loan becomes genuinely complex. Getting it wrong can mean higher costs, declined applications, or unexpected obligations for your family.

Here’s where an adviser adds the most value in an equity-based purchase:

- Identifying usable equity. Not all equity qualifies under every lender’s criteria. An adviser assesses your specific situation against current lender policies.

- Structuring the guarantee correctly. A good adviser will limit the guarantee to the smallest amount necessary, protecting the guarantor’s exposure.

- Matching you to the right lender. Different banks treat equity guarantees differently. Your adviser knows which lenders are most likely to approve your situation.

- Negotiating loan terms. Advisers can negotiate interest rates and conditions that a first home buyer might not secure independently.

- Planning for the future. An adviser will map out when and how the guarantee can be released once your own equity builds sufficiently.

Using the equity calculator tool available through Mortgage Managers is a great starting point to understand your current position before your first adviser conversation.

Pro Tip: Ask your adviser specifically about futureproofing your borrowing. A well-structured equity loan should include a clear plan for releasing any family guarantee within a defined timeframe, ideally three to five years.

You should absolutely seek advice if you are using family equity, unsure which lender suits your situation, or comparing multiple loan structures. On the other hand, if your equity position is simple and well-documented, a single consultation may be all you need to move forward confidently.

A fresh perspective on equity for first home buyers

It’s one thing to understand the rules, but let’s challenge the conventional approach with a view that most standard guides won’t offer you.

Most Kiwi first home buyers underutilise equity for two reasons: risk-aversion and incomplete information. Banks are not always forthcoming about creative equity solutions because their job is to assess your loan, not to design your strategy. You have to know to ask, and you have to ask the right person.

Here’s our honest take at Mortgage Managers: if you keep waiting to save enough cash to meet a 20% deposit in today’s Auckland market, you may be running a race where the finish line keeps moving. Property values in many parts of New Zealand have historically outpaced savings rates. Equity, used wisely and with expert guidance, is not a shortcut. It is a legitimate and often overlooked launchpad.

The in-depth equity release guide we’ve put together is worth reading if you want to take the next step with full understanding. The families who move forward confidently are not always the ones with the most cash. They’re the ones who asked better questions.

Move forward with expert mortgage advice

Ready to put your new equity knowledge into action? The team at Mortgage Managers is here to make this straightforward for you.

As your personal mortgage shoppers, we do the groundwork of comparing lenders, structuring your equity correctly, and finding terms that suit your unique situation. Every first home buyer’s circumstances are different, and a one-size approach simply doesn’t work when equity is involved. Reaching out costs you nothing and could save you years of unnecessary saving. Visit the Mortgage Managers team today and take the first confident step towards owning your first home.

Frequently asked questions

Can I use my parents’ home equity to buy my first house?

Yes, many New Zealand lenders allow family equity guarantees, though specific criteria apply and all parties need to understand the risks and obligations involved before proceeding.

What’s the minimum equity I need for a home loan in New Zealand?

20% equity is the ideal threshold for better rates and to avoid low equity margins, but some lenders will accept as little as 5% or allow equity top-ups through guarantee arrangements.

Does using equity increase my future repayments?

Yes, using equity typically means you are borrowing more overall, which leads to higher repayments over the life of the loan. Your adviser will model this clearly so you understand the full repayment impact before you commit.

Is equity the same as a cash deposit?

No, equity versus cash are different things, but lenders allow you to use equity as security in a similar way to a cash deposit when your loan application is structured correctly.