TL;DR:

- Credit files significantly influence NZ home loan approvals, with timely payments and low utilization key.

- Improving credit takes months, but consistent positive habits can boost eligibility faster.

- Non-bank lenders offer flexibility for those with past credit issues, often at higher interest rates.

A single missed payment from three years ago. A credit card sitting at 80% of its limit. These small details can quietly block your path to a home loan in New Zealand, even if your income is solid and your savings are strong. Most Kiwis don’t realise how much their credit file shapes a lender’s decision, or how quickly targeted action can shift the outcome. This guide walks you through the practical, evidence-backed steps to repair your credit and position yourself confidently for a home loan, whether you’re a first-time buyer or working through past financial challenges.

Table of Contents

- Understanding your credit file and its impact

- The core mechanics of credit repair in New Zealand

- Timeline and expectations: Quick wins and enduring results

- Navigating lender options: Banks versus non-bank lenders

- What most guides miss: The real keys to credit repair success

- Let Mortgage Managers clear the path to your home loan success

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Understand your credit file | Your credit history, utilisation, and error-free records shape home loan outcomes much more than a single score. |

| Follow a proven repair process | Review reports, pay on time, lower utilisation, avoid new credit, and monitor improvement for best results. |

| Be patient for real results | Immediate improvements are possible, but major issues need months or years to fully recover before loan approval. |

| Choose the right lender path | Banks are stricter, non-banks offer flexibility for imperfect credit but at higher costs. |

| Expert support accelerates success | Mortgage advisers and brokers help connect you with suitable lenders and fast-track your home loan journey. |

Understanding your credit file and its impact

To understand how credit repair works, it’s crucial to first grasp how your credit file shapes loan outcomes. Your credit file is essentially a financial report card, a detailed record of how you’ve managed debt, repayments, and credit applications over time. In New Zealand, credit reporting agencies like Equifax, Centrix, and illion compile this information, and lenders rely heavily on it when deciding whether to approve your home loan.

Your credit score is a number derived from the data in your file. The higher the score, the lower the perceived risk to the lender. But here’s the part most people don’t realise: there is no single universal minimum score that guarantees approval. What matters is how your score stacks up against each lender’s own criteria.

Here’s what lenders typically focus on:

- Payment history: Whether you pay on time, every time

- Credit utilisation: How much of your available credit you’re using

- Length of credit history: How long you’ve had credit accounts open

- Number of recent applications: Each application leaves a mark on your file

- Errors or inaccuracies: Incorrect information that drags your score down unfairly

Understanding your credit file for NZ buyers is the starting point for any meaningful repair strategy. And it pays to know the rules that govern the process. The NZ lending regulations under the CCCFA and Responsible Lending Code require lenders to assess income stability, debt-to-income ratios, and holistic suitability, not just a credit score number.

Key insight: Banks generally prefer scores above 650, while non-bank lenders tend to be more flexible. But your whole financial picture matters, not just your score in isolation.

This is genuinely encouraging news. Even if your score isn’t perfect right now, you’re not necessarily locked out. The system is designed to look at your broader circumstances, which means strategic improvement can open real doors.

The core mechanics of credit repair in New Zealand

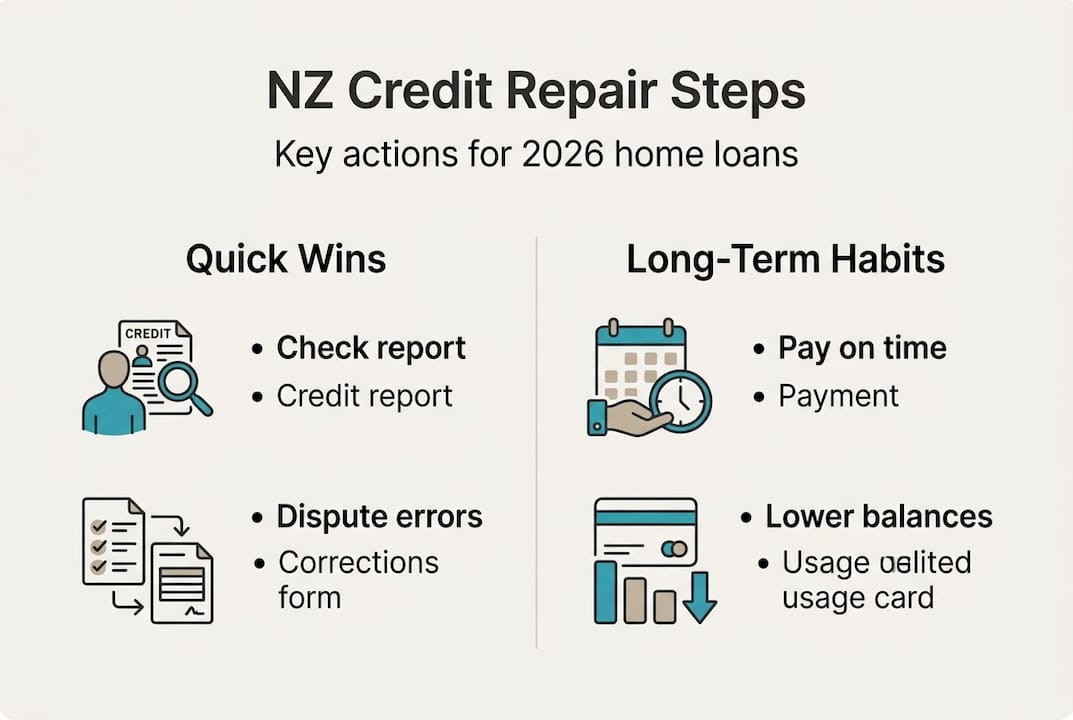

Once you know what shapes your credit, let’s break down the repair process step by step. Repairing your credit isn’t magic. It’s a methodical process where consistent, positive behaviour replaces the negative patterns that lowered your score in the first place.

Here’s a practical framework to follow:

- Obtain your credit report from Equifax, Centrix, or illion. You’re entitled to a free copy.

- Review it carefully for errors. Incorrect defaults, duplicated accounts, or wrong personal details all need to be disputed directly with the credit agency.

- Pay every bill on time going forward. This is the single most powerful action you can take.

- Reduce your credit card balances to below 30% of each card’s limit as quickly as possible.

- Avoid applying for new credit while you’re in repair mode. Every application leaves a hard enquiry on your file.

- Set up automatic payments so you never miss a due date, even during busy or stressful periods.

- Monitor your progress every quarter to see what’s working and adjust your approach.

Following a structured path to rebuilding credit for NZ home loan eligibility means reviewing reports, paying on time, reducing utilisation below 30%, avoiding new applications, resolving debts, and monitoring progress quarterly.

Pro Tip: Set calendar reminders three days before each bill is due, not just on the due date. This gives you a buffer to fix any issues before you miss a payment.

Here’s a quick comparison of the most impactful credit repair actions:

| Action | Time to see impact | Difficulty |

|---|---|---|

| Dispute and fix errors | 30-60 days | Low |

| Reduce credit utilisation | 30-45 days | Medium |

| Consistent on-time payments | 3-6 months | Low |

| Resolve outstanding defaults | 6-12 months | Medium/High |

| Build credit history length | 12+ months | Passive |

Using improving credit score tips tailored for New Zealand buyers can accelerate this process. Pair these actions with regular credit monitoring guidance to track your gains and stay on course.

Timeline and expectations: Quick wins and enduring results

Now that you know the steps, it’s vital to understand how long results actually take. Setting realistic expectations isn’t pessimism. It’s the most useful thing you can do to stay motivated through the process.

Some improvements happen faster than you might expect. Reducing your credit card utilisation below 30% can deliver score improvements in 30-45 days, sometimes meaningfully. Three to six months of consistent, on-time payments can produce substantial progress that lenders genuinely notice.

![]()

Here’s a realistic breakdown of the NZ credit repair timeline:

| Credit issue | Time to improve | Time to clear from file |

|---|---|---|

| High utilisation | 30-45 days | Immediate on repayment |

| Missed payments | 3-6 months of positives | 5 years |

| Defaults | 6-24 months of positives | 5 years |

| Serious credit infringements | 1-3 years | 7 years |

| Bankruptcy | 2-5 years of positives | 7 years |

The timeline for qualifying with defaults may feel daunting, but partial improvements along the way are real and valuable. Lenders do look at the trend. A file that shows consistent recovery is far more compelling than one that shows stagnation.

Important realities to keep in mind:

- Major issues like defaults and bankruptcy remain on your New Zealand credit file for up to seven years

- Full default clearance typically happens at the five-year mark

- Consistent positive behaviour from now means you’re actively building a better story for lenders

- Non-bank lenders can often work with you earlier in the recovery journey

Statistic to know: Some buyers have seen their credit score boost by 50% in six months through focused, consistent action on utilisation and payment history.

The message here is straightforward. Start now, stay consistent, and every month of positive behaviour is a step closer to your home loan approval.

Navigating lender options: Banks versus non-bank lenders

After understanding repair timelines, you’ll need to know which lenders fit your improved situation. Not all lenders are created equal when it comes to credit history, and knowing your options can save you from unnecessary rejections.

Traditional banks are generally the most risk-averse. They tend to prefer applicants with scores above 650 and a clean, consistent repayment history. A single default from a few years ago can be enough to prompt a decline, even if everything else looks strong. Banks move carefully, and their criteria reflect that.

Non-bank lenders operate differently. They assess your application with more flexibility, considering your full financial story rather than relying as heavily on a score threshold. This makes them a genuine beacon of hope for buyers working through past credit challenges. The trade-off is that non-bank loan options typically come with higher interest rates, which reflects the additional risk the lender is taking on.

Here’s how the two options stack up:

- Banks: Lower interest rates, stricter criteria, prefer scores above 650, less flexibility on recent credit events

- Non-bank lenders: Higher interest rates, more flexible assessment, consider the full picture, accessible earlier in credit recovery

Pro Tip: A non-bank loan doesn’t have to be your permanent solution. Many buyers use one to get into their home, repair their credit further, then refinance to a mainstream bank lender after 12-24 months.

This is where a mortgage broker becomes your financial GPS. Brokers like the team at Mortgage Managers can access a wide range of lenders and match your specific circumstances to the right option, saving you the credit damage of multiple rejected applications. For practical approval tips for bad credit situations, working with a broker is often the smartest move you can make. Banks are stricter and favour scores above 650, while non-bank lenders accept lower scores at higher rates, and brokers help match applicants to suitable credit assessment options.

What most guides miss: The real keys to credit repair success

Having covered the practical steps and options, let’s share the real-world wisdom every home loan hopeful needs. Most articles about credit repair focus heavily on score numbers. Check your score here, target this number, hit that threshold. But in our experience working with New Zealand home buyers, obsessing over the number misses the point entirely.

What lenders actually trust is a pattern of behaviour. A rising score built on six months of consistent payments tells a far more convincing story than a one-time fix that bumped the number without changing anything meaningful. Prioritising payment history and low utilisation delivers the fastest gains, but patience is what transforms those gains into lasting mortgage eligibility.

Score-tracking apps and calculators are useful tools. We’re not dismissing them. But they can create a false sense of progress if your underlying habits haven’t changed. The buyers who successfully repair their credit and hold onto that improvement are the ones who build reliable financial routines, not those who chase short-term score jumps.

Focus on NZ credit score tips that build genuine long-term habits. The score will follow. That’s the part most guides won’t tell you clearly enough.

Let Mortgage Managers clear the path to your home loan success

With clarity on credit repair, timelines, and lender options, here’s how Mortgage Managers can support your home loan journey.

Knowing what to do is one thing. Having experienced advisers in your corner is another entirely. At Mortgage Managers, we specialise in helping Kiwis navigate exactly these kinds of challenges, whether you’re a first-time buyer building your credit profile or a homeowner working through past setbacks.

Our advisers work across both bank and non-bank lenders, matching your unique situation to the right solution at the right time. We guide you through the mortgage application process from start to finish, helping you avoid the common mistakes that slow approvals down. Think of our personal mortgage advisers as your dedicated guides through every step of the home buying journey. Reach out today and let’s map the clearest route to your home loan approval together.

Frequently asked questions

How long does credit repair take before I can apply for a home loan in New Zealand?

Quick improvements, like reducing credit utilisation, may be visible in 30-45 days, but major issues such as defaults can take two to seven years to fully clear from your file.

Is there a minimum credit score needed for banks versus non-bank lenders?

Banks typically favour scores above 650 and apply stricter criteria, while non-bank lenders accept lower scores with more flexibility, though usually at higher interest rates.

What is the most important factor for improving my credit score?

Paying every bill on time is the single biggest driver of credit repair, followed closely by keeping your credit utilisation below 30%, as confirmed by rebuilding credit research for NZ buyers.

What laws protect me when repairing credit or applying for a mortgage?

New Zealand’s CCCFA and Responsible Lending Code require lenders to assess your affordability and overall suitability fairly, giving you important consumer protections throughout the process.

How can Mortgage Managers help with my credit repair and home loan goals?

Mortgage Managers advisers provide expert lender matching and personalised support, helping home buyers with credit challenges find the right path to approval through the role of advisers in the home buying process.