TL;DR:

- Understanding your borrowing power helps you determine a realistic property budget and avoid chasing homes beyond your means.

- Factors such as income, expenses, existing debts, deposit size, and credit history influence how much you can borrow, and these can be improved through strategic actions.

Figuring out how much you can borrow is one of the first and most important steps in buying your first home in New Zealand, yet it’s also one of the most confusing. Many buyers spend months searching for properties without knowing whether their budget is realistic, only to face disappointment at the bank. The good news is that borrowing power is not some mysterious number locked away in a lender’s vault. Once you understand what drives it, you can take practical steps to strengthen your position, even if you have a modest deposit or a few credit bumps along the way.

Table of Contents

- What is borrowing power and why does it matter?

- What do lenders look at? Key factors that affect borrowing power

- How to calculate your borrowing power: a step-by-step guide

- Common mistakes first home buyers make

- How lenders assess unique cases: low deposits and imperfect credit

- What most guides get wrong about borrowing power

- Get tailored help with your borrowing power

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Borrowing power basics | It’s how much you can borrow, shaped by income, expenses, debts, deposit, and credit history. |

| Know what banks check | Lenders assess more than income—your expenses, debts, and credit make a big impact. |

| Steps you can take | Work through the basic calculation, check your numbers, and seek help if needed. |

| Avoid common pitfalls | Don’t overestimate your borrowing or hide debts; honest figures lead to better outcomes. |

| Options for tricky cases | Low-deposit or credit-impaired buyers still have solutions and should investigate all lender types. |

What is borrowing power and why does it matter?

Borrowing power is simply the maximum loan amount a lender will offer you, based on a careful look at your finances. Think of it as your financial GPS for the property market. It tells you where you can go, what you can afford, and how to get there without running out of fuel halfway.

Why does it matter so much? Because it shapes everything. Your borrowing power determines the price range you should be searching in, the type of property you can realistically target, and whether your home loan application is likely to succeed or stall. Buyers who skip this step often fall in love with homes outside their reach, wasting time, money, and emotional energy.

Several core factors feed into your borrowing power:

- Your income, including salary, wages, self-employment earnings, and rental income

- Your regular living expenses and the number of dependants you support

- Any existing debts, such as car loans, credit cards, student loans, or hire purchase agreements

- The size of your deposit and your savings history

- Your credit score and any past defaults or missed payments

Understanding factors affecting mortgage rates can also shift your borrowing power significantly, since even a small change in interest rates alters how much a lender thinks you can comfortably repay each month.

“Borrowing power is not a fixed ceiling. It’s a dynamic figure that responds to the choices you make today, long before you set foot in a bank.”

Setting realistic expectations from the start saves you enormous stress. It also means you walk into every conversation with a lender or mortgage adviser with confidence rather than guesswork.

What do lenders look at? Key factors that affect borrowing power

Now that the concept is clear, let’s look at what details lenders actually scrutinise when they sit down to calculate your borrowing power. The picture is more detailed than most buyers expect.

Income is the starting point. Lenders look at your gross income, meaning your earnings before tax, from all sources. Full-time employment is viewed favourably because it signals stability. Casual, part-time, or self-employed income is still counted, but lenders typically want to see a track record, often two years of tax returns for self-employed applicants.

Regular expenses matter enormously. Lenders use their own living cost benchmarks to estimate how much a household of your size typically spends each month. They also factor in your actual declared expenses. If you have children, your childcare and schooling costs will reduce the income available for mortgage repayments.

Existing debts are a major variable. Your credit score role is closely tied to how lenders view your debt history. Every credit card limit is counted against you, even if the balance is zero, because lenders assume you could draw on that credit at any time.

| Factor | Impact on borrowing | How to improve |

|---|---|---|

| Gross income | Higher income increases borrowing | Add all legitimate income sources |

| Living expenses | Lower expenses increase borrowing | Reduce discretionary spending |

| Credit card limits | Reduces available borrowing | Cancel unused cards before applying |

| Existing loan debts | Directly reduces borrowing power | Pay down or consolidate debts |

| Deposit size | Larger deposit reduces risk and may unlock better rates | Save consistently and use KiwiSaver |

| Credit score | Strong score improves approval chances | Fix errors, avoid late payments |

Understanding mortgage features for first-time buyers can also help you identify which loan structures align best with your financial profile before you even apply.

Pro Tip: Cancel any credit cards or store cards you’re not actively using at least three months before you apply for a home loan. Even a $5,000 limit on an untouched card can reduce your borrowing power by more than you’d expect.

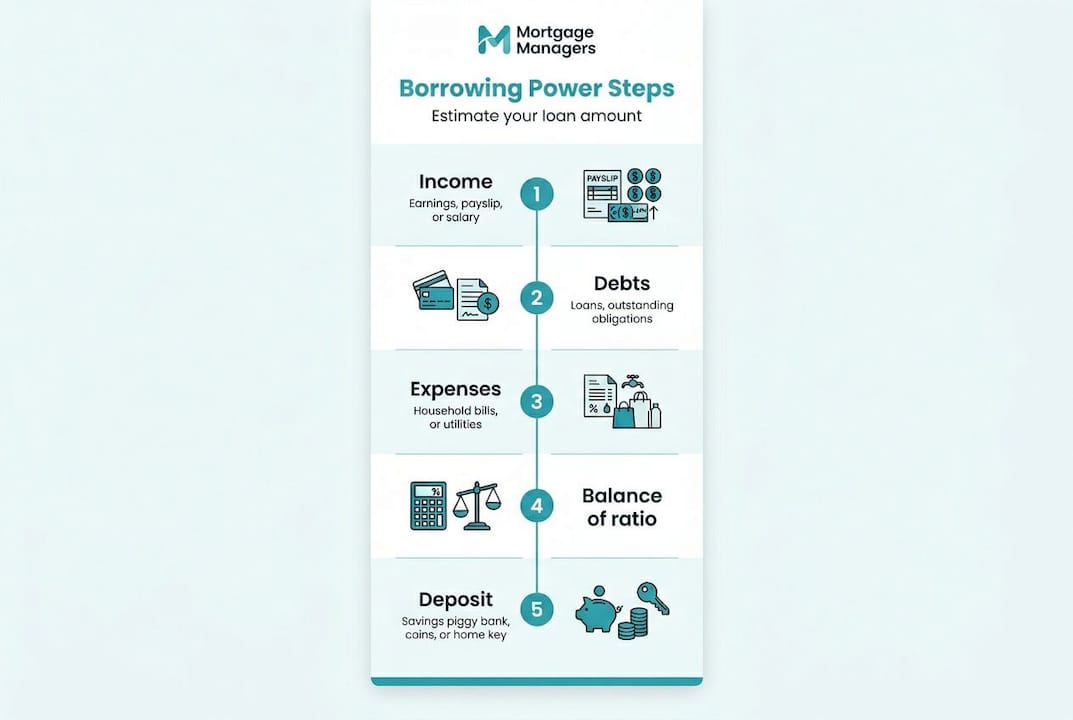

How to calculate your borrowing power: a step-by-step guide

Armed with an understanding of the key factors, you can now work through a practical process to estimate your own borrowing power. This won’t replace a full assessment by a mortgage adviser, but it will give you a solid starting point.

Step 1: Gather your income information. List every regular income source: your salary, any secondary employment, rental income, government support such as Working for Families, and any other verifiable income. Write down the annual gross figure for each.

Step 2: List your debts and monthly repayments. Include every credit card limit, personal loan balance, car loan, student loan, and overdraft facility. Note the monthly repayment for each.

Step 3: Estimate your living costs. Use the following benchmarks as a guide, knowing that lenders will use their own minimum figures too:

| Household type | Estimated monthly living costs |

|---|---|

| Single person | $1,800 to $2,400 |

| Couple, no children | $2,800 to $3,500 |

| Family with one child | $3,500 to $4,500 |

| Family with two or more children | $4,500 to $6,000 |

Step 4: Apply a serviceability ratio. New Zealand lenders typically assess your ability to repay at a test interest rate, often 1.5% to 2% higher than the current advertised rate. This is a buffer to ensure you could still afford repayments if rates rise. A common rule of thumb is that your total debt repayments, including the new mortgage, should not exceed 35% to 40% of your gross income.

Step 5: Account for your deposit and LVR. LVR stands for loan-to-value ratio and represents the proportion of the property’s value that you’re borrowing. If a home is worth $700,000 and you have a $140,000 deposit, your LVR is 80%. Most mainstream lenders prefer an LVR of 80% or below. A higher LVR can still work but often comes with additional requirements or a slightly higher interest rate.

A sample calculation: Imagine you earn $90,000 gross per year, your partner earns $70,000, giving a combined income of $160,000. You have $2,000 in monthly living costs, a car loan with a $400 monthly repayment, and $120,000 saved as a deposit. Based on standard serviceability assumptions, a rough estimate might give you a borrowing capacity in the range of $680,000 to $750,000, which combined with your deposit puts your property budget around $800,000 to $870,000.

Following the steps to get a mortgage in New Zealand in the right order makes this process far smoother. Before you reach the formal application stage, reviewing mortgage application tips for Kiwi buyers can help you avoid common errors that slow approvals.

Pro Tip: Run your numbers using at least two different interest rate scenarios, one at the current advertised rate and one at the lender’s test rate. This shows you the realistic range of your borrowing capacity, not just the optimistic end.

Common mistakes first home buyers make

Once you’ve done the maths, it’s important to avoid the common errors that trip up so many first home buyers before they even reach the settlement stage.

Overestimating income. Buyers sometimes include income that lenders won’t fully count, such as bonuses that aren’t guaranteed, irregular overtime, or income from a side job they only started recently. If that income disappears from your calculation, your borrowing power may be thousands of dollars lower than you assumed.

Underestimating expenses. It’s tempting to present a lean household budget to look better on paper, but lenders use their own minimum benchmarks. If your declared expenses are below those benchmarks, the lender will substitute their figures. Being honest upfront avoids nasty surprises.

Overlooking small debts. A $2,000 credit card limit here and a $1,500 Afterpay arrangement there might feel insignificant, but they add up quickly and can shave a meaningful amount off your maximum loan.

Ignoring future changes. Many first home buyers forget to account for circumstances that could shift after purchase. Planning a family? Parental leave will reduce household income. Expecting a rate rise? Your repayments may increase materially within a year or two of buying.

- Avoid relying solely on online calculators, which often use generic assumptions rather than your specific lender’s criteria

- Don’t apply to multiple lenders at once, as each credit check leaves a mark on your credit file

- Never assume that being pre-approved means you’re fully approved, conditions still apply

- Don’t make large purchases or take on new debt between pre-approval and settlement

“The gap between what a calculator says and what a lender actually approves can be significant. A mortgage adviser bridges that gap.”

Getting mortgage approval as a first-time buyer often comes down to preparation and knowing which mistakes to sidestep before they cost you.

How lenders assess unique cases: low deposits and imperfect credit

If you’re worried you won’t qualify because your deposit is small or your credit history is less than perfect, there is genuinely encouraging news. The lending landscape in New Zealand has more options than many first home buyers realise.

Low deposit options. The First Home Loan scheme, backed by Kāinga Ora, allows eligible buyers to purchase with as little as a 5% deposit if you meet income and price caps. This is a genuine game-changer for buyers who have been saving diligently but can’t quite reach the 20% threshold. Some banks also have their own low-deposit products for buyers with strong income and employment stability.

Guarantor support. A parent or close family member can act as a guarantor, using equity in their own home to support your application. This can reduce your effective LVR without requiring you to save a larger deposit yourself. It’s a meaningful way families can help without handing over cash.

Non-bank lenders. If the main banks say no, the conversation is far from over. Non-bank lenders specialise in complex or non-standard cases and often have more flexible criteria around credit history, income types, and deposit size. The trade-off is sometimes a slightly higher interest rate, but for many buyers it’s the bridge they need to get into their first home.

Strengthening a weak credit profile:

- Check your credit report for errors and dispute any inaccuracies immediately

- Pay all existing bills and minimum repayments on time, consistently, for at least six months before applying

- Reduce or eliminate high-interest consumer debt

- Avoid applying for new credit in the lead-up to your mortgage application

- Show a solid pattern of regular savings, even modest amounts add up over time

Pro Tip: Don’t self-disqualify before you’ve spoken to a professional. Many buyers assume they have no chance and never ask. A mortgage adviser who works across multiple lenders can often find a pathway that a single bank visit would never reveal.

What most guides get wrong about borrowing power

Here’s an honest observation from years of working with New Zealand first home buyers. Most online guides and bank calculators present borrowing power as a simple arithmetic problem. Put in your numbers, get a figure, done. But that misses the most important truth: borrowing power is dynamic, negotiable, and lender-specific.

We regularly see buyers who were told by one lender they couldn’t borrow enough to buy in their target suburb, only to find a different lender or a different loan structure gave them the capacity they needed. This isn’t because the second lender is reckless. It’s because different institutions weigh factors differently. Some are more generous with certain income types. Some count boarder income. Others have lower expense benchmarks for certain household configurations.

The other thing guides rarely say clearly is that timing matters. A buyer who cleans up their credit, reduces their credit card limits, and builds their savings over six focused months can dramatically shift their position. Borrowing power is a reflection of your financial health at a point in time, not a permanent verdict.

Understanding the full range of types of mortgage lenders in New Zealand is genuinely valuable knowledge. Banks are the most visible option but they are not always the best fit for every buyer’s situation.

The buyers who succeed fastest are those who seek advice early, before they start attending open homes. They come to the process knowing their numbers, understanding their options, and ready to act when the right property appears.

Get tailored help with your borrowing power

Understanding your borrowing power is empowering, but putting it into practice is where the real work begins. You don’t have to navigate this alone, and honestly, you shouldn’t have to.

At Mortgage Managers, our expert mortgage advisers are based in Hobsonville and work with first home buyers across Auckland, West Auckland, the North Shore, and remotely throughout New Zealand. We act as your personal home loan shoppers, comparing options across a wide panel of lenders to find the right fit for your situation. Whether your finances are straightforward or a little more complex, a quick conversation can clarify exactly what you can borrow and how to get there. Ready to find out where you stand? Apply for a mortgage and take the first real step towards owning your home.

Frequently asked questions

What is the minimum deposit needed for a first home in New Zealand?

The minimum deposit is typically 20% of the property’s purchase price, but eligible buyers can access the First Home Loan scheme with as little as 5% if they meet income and price cap criteria.

How does student loan debt affect my borrowing power?

Student loan repayments are treated as a regular outgoing by lenders, which reduces the income available for mortgage repayments and therefore lowers your overall borrowing power.

Can I get a mortgage with a poor credit history?

Yes, some non-bank lenders and government-backed schemes work with applicants who have credit challenges, though conditions and interest rates may differ from standard loans.

Does including boarder income help my home loan application?

Some lenders will accept boarder income as a contribution to your total income if it is regular and supported by evidence such as a tenancy agreement or bank deposits, but criteria vary significantly between lenders.

How often should I reassess my borrowing power?

You should recalculate your borrowing power any time your financial situation changes materially, such as a pay rise, new debt, change in employment, or a shift in living costs.