TL;DR:

- First-time homebuyers in New Zealand often underestimate the total upfront costs beyond their deposit, which include legal fees, disbursements, insurance, and rates adjustments. Proper budgeting involves early estimates, adding buffers, understanding disbursements, and recognizing that settlement costs can vary significantly, preventing delays or surprises at closing. Collaborating with professionals and planning for all expenses ensures a smoother settlement process and financial confidence.

You’ve saved your deposit, you’ve found the right property, and you’re ready to sign. Then your lawyer sends through a settlement statement and the total is several thousand dollars more than you expected. This is exactly why budget for closing costs matters so much, and why skipping this step catches so many first-time buyers off guard. Closing costs are the fees and charges that sit outside your deposit, and they are unavoidable. Understanding them early is the difference between a smooth settlement and a stressful scramble for cash.

Table of Contents

- Key takeaways

- Closing costs explained for NZ first home buyers

- The misconceptions that catch buyers out

- How to estimate and budget for closing costs

- Deposit vs closing costs: the full picture

- Managing closing costs without the stress

- My take on why this matters more than most buyers realise

- Let Mortgagemanagers help you plan for settlement

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Closing costs go beyond the deposit | Legal fees, disbursements, insurance and rates adjustments add thousands to your upfront cash needs. |

| NZ legal fees alone can be significant | Typical legal fees range from $1,200 to $2,500 plus GST, and that is before disbursements. |

| KiwiSaver does not cover closing costs | Your KiwiSaver withdrawal funds the deposit only, so settlement fees need separate cash. |

| Budget a buffer on top of estimates | Prorations and last-minute adjustments mean your final settlement figure often exceeds early quotes. |

| Get detailed quotes early | Separating fixed fees from third-party disbursements helps you build a realistic total picture. |

Closing costs explained for NZ first home buyers

Closing costs are the upfront settlement fees you pay on top of your deposit to finalise the purchase of a home. Buyers typically pay most closing costs, which include lender fees, legal fees, and government charges. In New Zealand, these costs take a specific shape that every first-time buyer should understand before signing anything.

Here are the main categories you will encounter at settlement:

- Legal fees and conveyancing costs. Your solicitor handles the title search, contract review, and settlement process. NZ legal fees typically range from $1,200 to $2,500 plus GST, and some firms offer first-home buyer discounts worth asking about.

- Government disbursements. These include title registration fees and any Land Information New Zealand (LINZ) charges, which your lawyer passes on at cost.

- Building and LIM reports. A building inspection can cost $400 to $900 depending on the property size and location. A Land Information Memorandum (LIM) from your local council typically runs $200 to $400.

- Home and contents insurance. Most lenders require you to have insurance in place from settlement day. Your first premium or bond may be payable upfront.

- Council rates and utility prorations. If the seller has pre-paid rates or other outgoings, you will reimburse them for the period from your settlement date to the end of that billing cycle. These settlement-day adjustments affect your final cash requirement and are easy to underestimate.

In some transactions, sellers may agree to cover a portion of closing costs as part of negotiations. However, you should not rely on this, especially in competitive markets. Plan to fund everything yourself and treat any seller contribution as a bonus.

Understanding NZ legal fees for home buyers early in the process means you will not be blindsided when the settlement statement arrives.

The misconceptions that catch buyers out

The most common mistake first-time buyers make is treating their deposit as the full measure of their upfront cash commitment. Your deposit secures the purchase, but it does not touch any of the fees and charges due at settlement. These are entirely separate expenses, and the gap between what buyers expect and what they actually owe at closing catches people out repeatedly.

A second misconception is that closing costs are fixed and predictable from the start. The truth is that actual closing costs can vary significantly, and early estimates change as the transaction progresses. Third-party disbursements shift depending on property-specific factors. Rates prorations depend on the exact settlement date. Even a one-week change to your settlement date can alter your final figure.

“Unexpected charges, often from prorations or added disbursements, cause common settlement-day surprises. Experienced conveyancers advocate keeping buffers in place from the time the final settlement statement is issued until funds are cleared.” — MoneyBalance NZ

The danger here is not just financial stress. If you do not have enough cleared funds on settlement day, the settlement can be delayed. A delayed settlement can trigger penalty interest clauses in your contract and create a cascade of problems involving your lender, the vendor, and your own moving timeline.

Pro Tip: Request a detailed cost estimate from your lawyer as soon as you have an accepted offer. Do not wait until the week before settlement to ask what you owe.

How to estimate and budget for closing costs

Getting this right comes down to one principle: start early and add a buffer. Here is a practical process for first-time buyers in New Zealand.

-

Get a legal quote before you commit. Ask your lawyer to provide a written estimate that separates their fixed fee from third-party disbursements. Detailed cost breakdowns help you understand what is certain and what may change, which is the foundation of accurate budgeting.

-

Budget for reports upfront. Set aside money for building inspection and LIM report costs from the moment you start seriously looking at properties. These are often paid before settlement and before your formal mortgage approval.

-

Separate your KiwiSaver funds from your settlement cash. KiwiSaver withdrawals cover your deposit but do not extend to legal or settlement fees. These closing costs require separate cash, and many buyers miss this distinction entirely. KiwiSaver funds cannot be used for closing costs, so plan your settlement cash as a completely independent line in your budget.

-

Add a 10% to 15% buffer to your closing cost estimate. Prorations and last-minute adjustments are the norm, not the exception. A small buffer prevents a large problem.

-

Shop around for services where you can. Lender fees and service costs can vary and some are negotiable. Comparing lawyer quotes and asking about bundled services can reduce your total closing cost figure without sacrificing quality.

Pro Tip: When you receive your lawyer’s initial estimate, ask specifically whether the disbursements are capped or estimated. Capped disbursements give you a ceiling; estimated ones can exceed the quoted figure.

Deposit vs closing costs: the full picture

Many buyers fixate on the deposit percentage and lose sight of what else needs to be funded. Closing costs typically range from 2% to 5% of the purchase price. On a $700,000 property, that translates to $14,000 to $35,000 in closing costs on top of your deposit. Even at the lower end, this is a meaningful sum that requires its own budget line.

The table below shows a realistic breakdown of typical closing expenses for a first-home buyer in New Zealand purchasing a property in the $600,000 to $800,000 range.

| Expense | Typical range |

|---|---|

| Legal fees (incl. GST) | $1,500 to $3,000 |

| LINZ and title registration | $200 to $400 |

| Building inspection | $400 to $900 |

| LIM report | $200 to $400 |

| Home insurance (first premium) | $500 to $1,200 |

| Council rates proration | $200 to $800 |

| Mortgage registration fee | $100 to $300 |

| Miscellaneous adjustments and bank fees | $200 to $600 |

| Estimated total | $3,300 to $7,600+ |

That is a substantial addition to your deposit requirement. If you are stretching to reach a 10% or 20% deposit, these closing costs need to be funded separately and should not erode the deposit you have worked to accumulate. Planning your total cash amount, deposit plus closing costs plus buffer, is the only way to walk into settlement with genuine confidence.

Exploring real estate buying tips from experienced advisers reinforces that this total-cost thinking is standard practice among prepared buyers everywhere.

Managing closing costs without the stress

Once you understand what closing costs are and roughly what they will cost, managing them becomes much more straightforward. The goal is to move from reactive to proactive, and these practices help you do exactly that.

- Build your closing cost estimate into your savings goal from day one. Do not save your deposit and then realise you have nothing left for settlement fees. Treat closing costs as part of the total cash you need before you can buy.

- Work closely with your mortgage adviser and your conveyancer. These two professionals have the most direct visibility over what you will owe and when. Regular updates from both of them mean you are never caught unaware by a change in your settlement figure.

- Understand what seller concessions can and cannot achieve. Seller contributions can reduce out-of-pocket closing costs in some negotiations, but they depend entirely on market conditions and the seller’s motivation. Budget to fund everything yourself and negotiate seller contributions as an optional reduction rather than a planned one.

- Update your budget as estimates finalise. Your legal estimate from week one will sharpen as settlement approaches. Revise your figures whenever you receive updated information so your running total stays accurate.

- Prepare for settlement day properly. Having cleared funds available, and not just committed funds, is the only way to prevent settlement complications.

Pro Tip: Create a simple spreadsheet with two columns: your deposit funding sources (KiwiSaver, savings, gifted funds) and your closing cost funding sources (cash savings only). Keeping these visually separate helps you track both without accidentally conflating them.

My take on why this matters more than most buyers realise

I have worked with first-home buyers across Auckland and the wider New Zealand market for years, and the pattern I see most often is not a lack of commitment. It is a lack of information at the right stage of the process.

Buyers come in having saved a solid deposit. They have done the hard work. But when we sit down to map out the full cash requirement for settlement, the closing cost side of the ledger is almost always underprepared. Not because buyers are careless, but because no one clearly explained it to them upfront.

What I have learned is that treating the deposit and closing costs as two separate financial goals from the very beginning changes everything. Once you mentally separate them, you plan for them differently, you track them differently, and you reach settlement day with both covered instead of robbing one to fund the other.

The other thing worth saying plainly: the importance of closing costs is not something you should discover from your settlement statement. It should be something your mortgage adviser walks you through in the first meeting. If that conversation has not happened, ask for it.

Professional guidance at this stage is not a luxury. It is the most practical way to protect the savings you have worked hard to accumulate.

— Stuart

Let Mortgagemanagers help you plan for settlement

Understanding why you need to budget for closing costs is one thing. Having someone guide you through the exact numbers for your specific situation is another.

At Mortgagemanagers, our mortgage advisers in Auckland work with first-home buyers to map out their full upfront cash requirements, not just the deposit figure. We help you understand what your lender will need, what your lawyer will charge, and how to structure your savings so both your deposit and your settlement costs are funded when it matters. Whether you are in Hobsonville, West Auckland, the North Shore, or anywhere across New Zealand, our team is ready to help. Reach out to the Mortgagemanagers team to get started with a personalised plan today.

FAQ

What are closing costs when buying a home in NZ?

Closing costs are the fees and charges payable at settlement, separate from your deposit. They typically include legal fees, government disbursements, building reports, insurance, and council rates adjustments.

Why budget for closing costs separately from the deposit?

Your deposit and closing costs are funded from different sources. KiwiSaver funds cover the deposit but cannot be used for settlement fees, so you need separate cash savings available on settlement day.

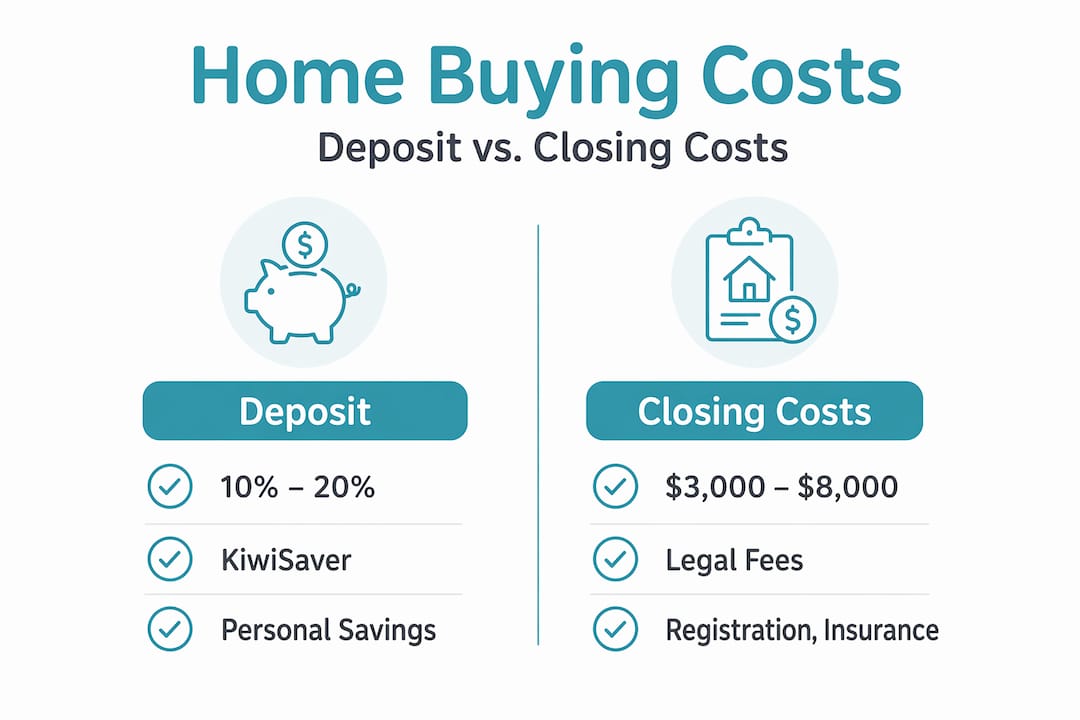

How much should I set aside for closing costs in NZ?

For most NZ first-home buyers, closing costs run between $3,000 and $8,000 depending on the property and transaction. Adding a 10% to 15% buffer on top of your lawyer’s estimate is a sound approach.

Can I negotiate closing costs with the seller?

In some cases, sellers may agree to contribute toward closing costs as part of the sale negotiation. However, this is not guaranteed, so budget to cover all costs yourself and treat any contribution as a reduction rather than a planned offset.

When should I start budgeting for closing costs?

Start as early as possible, ideally at the same time you begin saving your deposit. Getting a legal quote and building reports estimate before you make an offer gives you a realistic total cash target well before settlement day.