TL;DR:

- Understanding principal and interest helps New Zealand borrowers manage their mortgage effectively and save money over time.

- While early payments are mostly interest, making extra repayments and choosing suitable loan structures can significantly reduce total interest costs and loan duration.

When you take out a home loan in New Zealand, every repayment you make is doing two jobs at once. Yet most borrowers spend years making payments without truly understanding what is principal and interest, or how those two components split inside each monthly instalment. That gap in knowledge costs people real money. Understanding principal and interest explained in plain terms puts you in control of your budget, helps you spot opportunities to save, and removes the anxiety that comes from writing a large cheque every month without fully knowing where it goes.

Table of Contents

- Key takeaways

- What is principal and interest on a mortgage?

- How principal and interest shift over a 30-year loan

- Principal and interest versus interest-only loans

- Strategies to pay down principal faster

- My honest take on understanding your mortgage

- How Mortgagemanagers can help you

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Principal is your loan balance | It is the amount you originally borrowed, reducing with every repayment you make. |

| Interest is the cost of borrowing | Calculated monthly on the outstanding principal balance, it decreases as your balance drops. |

| Early payments are mostly interest | In the first years of a 30-year loan, only a small slice of each payment reduces the principal balance. |

| Extra payments create big savings | Paying additional amounts toward principal early on cuts future interest and shortens your loan term. |

| P&I is not your full housing cost | Property rates, insurance, and body corporate fees sit on top of your principal and interest repayment. |

What is principal and interest on a mortgage?

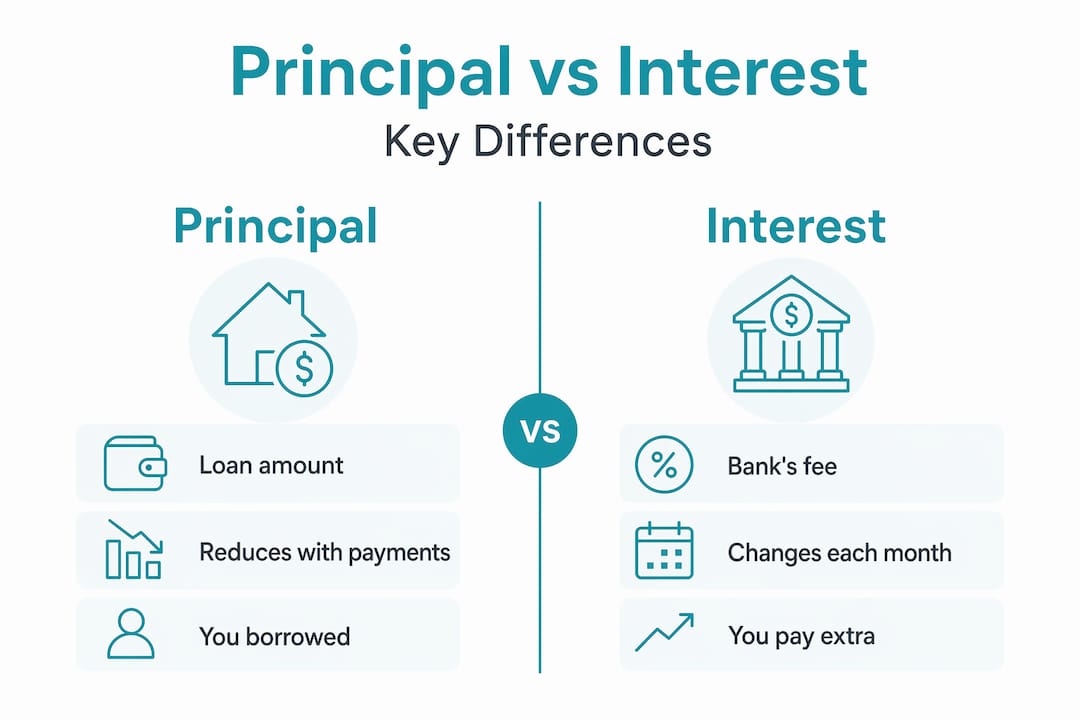

These two words describe the twin components inside every standard home loan repayment. Get comfortable with both, and your entire mortgage becomes far less intimidating.

Principal is the actual amount of money you borrowed. If you purchased a home and took out a $600,000 loan, your opening principal balance is $600,000. Every dollar of principal you repay reduces that balance, which is sometimes called the principal balance meaning the total sum still owed to the lender on any given day.

Interest is the fee the bank charges for lending you that money. It is not a fixed dollar amount set at the start. Instead, interest is calculated monthly as a percentage of whatever principal balance remains unpaid. The formula is straightforward:

Monthly interest = (Outstanding principal × Annual interest rate) ÷ 12

Because interest is always calculated on the remaining balance, what is interest on a loan actually changes every single month. As you chip away at the principal, the interest charge shrinks alongside it. This is the engine that drives amortisation, the structured schedule by which your loan balance reaches zero over the agreed term.

Here is what a standard principal and interest (P&I) repayment looks like in practice:

- Each monthly payment is split between an interest charge and a principal reduction.

- The total payment amount stays the same for the life of a fixed repayment schedule.

- The interest portion shrinks each month because the balance it is calculated on gets smaller.

- The principal portion grows each month to keep the total payment constant.

- After the full loan term, the balance reaches exactly zero.

Pro Tip: Ask your lender or mortgage adviser for a full amortisation schedule the day you settle. Seeing the month-by-month breakdown of principal vs interest makes the entire loan feel concrete rather than abstract.

How principal and interest shift over a 30-year loan

This is the part that surprises most borrowers. The difference between principal and interest is not a 50/50 split. In the early years, most of your payment covers interest with only a small portion reducing the balance. That ratio slowly reverses over time.

To make this real, consider an example based on the New Zealand median home price. Using a 20% deposit and a 6.36% interest rate, the monthly P&I payment is approximately $2,068, with a total lifetime cost of around $744,480.

| Loan year | Approx. monthly interest | Approx. monthly principal | Outstanding balance |

|---|---|---|---|

| Year 1 | ~$3,180 | ~$288 | ~$597,700 |

| Year 5 | ~$2,960 | ~$508 | ~$559,200 |

| Year 10 | ~$2,620 | ~$848 | ~$493,800 |

| Year 20 | ~$1,680 | ~$1,788 | ~$315,500 |

| Year 30 | ~$25 | ~$2,043 | ~$0 |

Figures are illustrative and based on a $600,000 loan at 6.36% over 30 years.

That table tells a powerful story. In Year 1, roughly 92% of your payment is interest. By Year 20, the split has almost reversed. This is why understanding amortisation schedules empowers smarter repayment decisions. Borrowers who do not know this can feel demoralised watching their balance barely move in the first few years, not realising the system is working exactly as designed.

Pro Tip: Use a debt payoff calculator to model how even one extra repayment per year affects your total interest bill and loan end date. The numbers are often more motivating than people expect.

Principal and interest versus interest-only loans

Not every home loan in New Zealand follows the standard P&I structure. Some borrowers, particularly investors, opt for interest-only periods. Understanding the difference between principal and interest versus interest-only repayments is worth your time before you sign anything.

With an interest-only loan, your repayment covers only the interest charge for a set period, typically one to five years. The principal balance does not move at all during that time. Payments are lower in the short term, which appeals to investors managing cash flow. However, interest-only loans increase total interest paid over the life of the loan because the principal remains unchanged while interest accrues on the full balance.

| Feature | Principal and interest | Interest-only |

|---|---|---|

| Monthly repayment | Higher | Lower |

| Principal balance movement | Reduces from day one | Stays the same during I-O period |

| Total interest paid | Lower over loan life | Higher overall |

| Equity built | Grows steadily | Does not grow during I-O period |

| Risk profile | Lower | Higher if property values fall |

Who suits which structure? In plain terms:

- P&I suits owner-occupiers focused on building equity, first-home buyers, and anyone whose priority is minimising total cost over the loan term.

- Interest-only suits property investors who need to maximise short-term cash flow and can claim interest as a tax deduction, provided they have a clear strategy for the reversion to P&I repayments.

The risk with interest-only periods is that when they expire, your principal balance is the same as the day you settled. Your repayments jump sharply upward, and the remaining loan term is shorter. Budgeting for that transition is critical.

Strategies to pay down principal faster

Knowing how the numbers work is one thing. Using that knowledge to save money is another entirely. Here are practical moves that NZ borrowers can make to reduce their principal balance faster and cut total interest costs.

-

Make lump-sum extra repayments. A tax refund, work bonus, or inheritance paid directly onto your mortgage reduces the principal immediately. Extra principal payments reduce future interest on every remaining month of your loan, creating compounding savings that far exceed the one-off payment amount.

-

Increase your regular payment above the minimum. Even an additional $50 or $100 per fortnight toward principal accelerates your payoff timeline meaningfully. Over a 30-year loan, this strategy can save tens of thousands of dollars in interest.

-

Switch to fortnightly repayments. Instead of 12 monthly payments, fortnightly repayments produce 26 half-payments annually, which equals 13 full monthly payments. That one extra payment per year works directly on principal reduction. Fortnightly repayments reduce total interest and shorten loan duration without requiring a major budget overhaul.

-

Refinance to a lower interest rate. If market conditions have shifted since you first borrowed, a lower rate means more of each payment goes to principal from the outset. Refinancing has costs, so model the break-even point before committing. You can explore five ways to pay your mortgage faster to understand whether refinancing fits your situation.

-

Check your loan terms before paying extra. Some fixed-rate loans in New Zealand carry prepayment penalties or caps on extra repayments during a fixed term. Understand your contract so extra payments do not trigger unnecessary fees.

Pro Tip: Disciplined extra principal payments made in the first third of your loan term deliver the greatest interest savings because the outstanding balance is still large and every dollar of reduction has the maximum compounding effect.

One more thing to keep in mind as you budget: your P&I repayment is not your total housing cost. Property taxes and insurance sit on top of principal and interest, and distinguishing P&I from PITI (principal, interest, taxes, and insurance) prevents unpleasant surprises in your monthly cash flow. Build all of these into your budget from day one.

My honest take on understanding your mortgage

I have sat across from a lot of New Zealand borrowers over the years, and the single most common frustration I hear goes something like this: “We have been paying for four years and our balance has barely moved.” That feeling is real, and it is not a sign that anything is broken. It is simply the front-loaded nature of amortisation working as designed.

What concerns me more is when borrowers do not know to expect it. When you understand that the difference between principal and interest shifts dramatically over time, you stop feeling cheated and start feeling motivated. I have seen clients save well over $50,000 in interest simply by making one extra lump-sum repayment each year, not because they were wealthy, but because they understood how the numbers worked and acted accordingly.

The other thing I want to flag: many people focus intensely on the interest rate and forget to budget for the full cost of homeownership. Rates, body corporate levies, and insurance premiums are real monthly obligations. A mortgage that looks affordable on paper can become stressful when those extras land unexpectedly. Know what is principal and interest, but also know what sits outside that number.

My strongest piece of advice is this. Get your amortisation schedule, look at it honestly, and speak to an adviser who can help you build a repayment strategy around your real life. The numbers are not your enemy. They are your guide.

— Stuart

How Mortgagemanagers can help you

At Mortgagemanagers, we work with New Zealand borrowers every day who are trying to make sense of exactly these questions. Whether you are buying your first home or reviewing an existing loan, understanding how principal and interest interact inside your mortgage is the foundation of every smart repayment decision.

Our team of Auckland mortgage advisers takes the time to walk you through your amortisation schedule, explain your repayment options clearly, and help you find a loan structure that fits your life. We compare lenders across the market, identify opportunities to save on interest, and support you long after settlement. You should never feel like you are making one of the biggest financial decisions of your life without a trusted guide beside you. Reach out to the Mortgagemanagers team today and get clarity on your home loan from people who genuinely know the New Zealand mortgage market.

FAQ

What is the difference between principal and interest?

Principal is the amount you originally borrowed, while interest is the fee the lender charges for providing that loan. Each repayment reduces the principal balance and pays the interest calculated on what remains.

How do I calculate principal and interest on a mortgage?

Monthly interest is calculated by multiplying your outstanding principal balance by your annual interest rate, then dividing by 12. Your principal reduction for that month is the total payment minus the interest charge.

Why does my loan balance barely move in the early years?

Early in a 30-year loan, most of your payment covers interest because interest is calculated on a large outstanding balance. As the balance reduces over time, the interest portion shrinks and more of each payment reduces the principal.

What is the principal balance meaning in a home loan?

The principal balance is the total amount still owed to the lender on any given day, not including future interest charges. It decreases with each repayment and reaches zero at the end of the loan term.

Is interest-only better than a principal and interest loan?

Interest-only loans have lower short-term payments but do not reduce your balance, meaning you pay more interest overall. A principal and interest loan costs more each month but builds equity and reduces the total amount paid over the life of the loan.