TL;DR:

- Preparing complete and well-organized documents accelerates mortgage approval and minimizes delays in New Zealand.

- Lenders stress-test repayment capacity at high-interest rates, which may lower your borrowing limit unexpectedly.

Getting a better mortgage application together in New Zealand takes more than saving a deposit and hoping for the best. Many Kiwi borrowers are surprised to find their applications delayed or declined, not because they can’t afford the loan, but because their paperwork was incomplete, their bank statements told the wrong story, or they misunderstood what lenders actually look for. This guide walks you through exactly what banks scrutinise, how to prepare your documents, what affordability testing really means for your borrowing power, and how to time your application for the best possible outcome.

Table of Contents

- Key takeaways

- Building a better mortgage application starts with documents

- How NZ lenders assess your affordability

- Understanding mortgage pre-approval timing

- What investors need to know about LVR and deposits

- Practical tips to avoid common mortgage pitfalls

- My honest take on what really makes the difference

- How Mortgagemanagers helps you get approved

- Common questions

Key takeaways

| Point | Details |

|---|---|

| Document readiness matters | Having a complete evidence pack ready speeds up lender verification and reduces back-and-forth delays. |

| Affordability is stress-tested | NZ lenders test repayment capacity at rates around 8–8.5%, so your true borrowing limit may be lower than you expect. |

| Pre-approval has an expiry date | Mortgage pre-approvals are valid for 60–90 days and are conditional, not a guaranteed green light. |

| Investors face stricter deposit rules | Property investors need at least a 35% deposit under current LVR restrictions, compared to 20% for owner-occupiers. |

| Bank statement behaviour counts | Lenders scrutinise spending patterns closely, so cleaning up discretionary spending months before applying strengthens your position. |

Building a better mortgage application starts with documents

Before a lender can assess your borrowing capacity, they need to verify who you are, where your income comes from, and how you manage your finances. Skipping or delaying any part of this is one of the most common reasons applications stall. Complete document preparation is not just a formality. It directly speeds up lender verification and reduces the frustrating back-and-forth that can cost you weeks.

Here is what you will typically need to pull together:

- Photo ID: A current passport or driver’s licence

- Proof of address: A recent utility bill or bank statement showing your residential address

- Income proof: Three recent payslips and an IRD earnings summary; for self-employed borrowers, at least two years of financial statements and tax returns

- Bank statements: Three to six months of statements across all accounts, including savings and transaction accounts

- KiwiSaver documentation: Balance statements and evidence of withdrawal eligibility if you are using KiwiSaver as part of your deposit

- Liabilities documentation: Statements for credit cards, personal loans, car finance, and any existing mortgages

- Deposit evidence: Proof of how your deposit was accumulated, whether through savings, a gift, or equity

Self-employed borrowers face a steeper evidence requirement. Lenders want to see consistent income over at least two years, and a single strong year is rarely enough on its own. If this applies to you, working with an adviser who knows which lenders are more flexible with self-employed applications is genuinely useful.

Pro Tip: Organise your documents into a single digital folder before you begin talking to lenders. Being able to send everything at once signals that you are prepared and reduces the chance of a lender losing interest while waiting for outstanding items.

One area that catches many applicants off guard is the KiwiSaver withdrawal process. KiwiSaver withdrawal documentation must be prepared and verified before drawdown, so leaving this until the last minute can delay settlement. Start the process early.

Check the full mortgage application checklist from Mortgagemanagers to make sure nothing slips through the cracks.

How NZ lenders assess your affordability

Saving a 20% deposit does not automatically mean a lender will approve your loan. Affordability testing goes well beyond your income figure, and understanding this is central to improving your mortgage application.

New Zealand lenders operate under responsible lending obligations and the Credit Contracts and Consumer Finance Act (CCCFA), which require them to confirm you can comfortably service the loan. Banks stress-test repayment capacity at rates of 8.0 to 8.5%, which is typically 2 to 3 percentage points above the rate you will actually pay. This means if a lender offers you a rate of 5.8%, they will calculate whether you could still afford repayments if rates rose to around 8.5%.

Lenders also use the Household Expenditure Measure (HEM) as a benchmark for living costs, but here is the catch: they use whichever is higher between the HEM figure and your actual demonstrated spending. If your bank statements show you spending significantly more than the HEM benchmark, your assessed living expenses go up and your borrowing capacity comes down.

What lenders are looking for in your bank statements:

- Consistent, explainable income deposits

- No unexplained large deposits or withdrawals

- No pattern of overdrafts, missed payments, or dishonoured direct debits

- Gambling transactions, which are viewed very negatively even if infrequent

- Buy Now Pay Later (BNPL) accounts, treated as ongoing liabilities

The RBNZ debt-to-income rules also cap owner-occupier borrowing at 6 times gross income, while investors are capped at 7 times. If your total debt, including the proposed mortgage, exceeds this threshold, approval becomes much harder regardless of your deposit size.

Pro Tip: Three months before applying, treat your bank account as if a lender is already reading it. Cancel subscriptions you don’t use, reduce dining and entertainment spending, and avoid opening any new credit facilities. The visible improvement in your statements can meaningfully increase what a lender will offer you.

Understanding mortgage pre-approval timing

Pre-approval is one of the most misunderstood parts of the best mortgage application process. Many buyers seek it too early and let it expire, or treat it as a guaranteed loan when it is actually a conditional assessment.

Here is how pre-approval works in practice, in the right order:

- Assess your financial position first. Before approaching a lender, know your income, liabilities, and deposit amount. This prevents surprises during formal assessment.

- Submit your application close to when you intend to buy. Pre-approvals are valid for 60–90 days and will expire if you don’t proceed to an unconditional offer within that window.

- Avoid any financial changes during the pre-approval period. Taking on new debt, changing jobs, or making large purchases can void your pre-approval entirely, even if nothing was formally communicated to the lender.

- Understand what the lender reviews. Income stability, spending behaviour, existing liabilities, credit history, and deposit source are all assessed. A clean record across all five areas strengthens the outcome.

- Treat pre-approval as conditional, not final. The property itself must still be approved by the lender, and a formal valuation is typically required before unconditional approval is granted.

Timing your pre-approval close to your actual purchase is the single most effective way to protect its value. Applying six months before you plan to buy means you will likely need to reapply, with all the paperwork that involves. Read more about how pre-approval works at Mortgagemanagers’ pre-approval guide for NZ buyers.

Pro Tip: If your pre-approval is nearing its 90-day limit and you haven’t found a property yet, contact your adviser before it expires. A renewal is usually straightforward if your financial position hasn’t changed, and it avoids a gap in coverage.

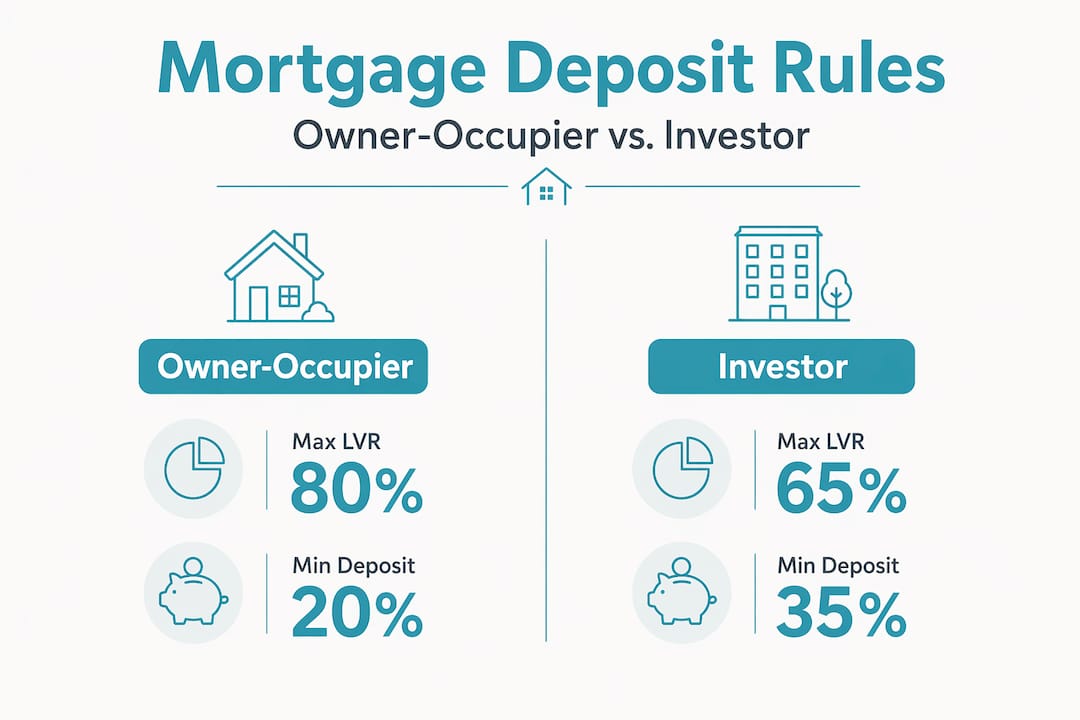

What investors need to know about LVR and deposits

Property investors face a noticeably different set of rules compared to owner-occupiers, and understanding these upfront can save you considerable frustration during the application process.

| Borrower type | Maximum LVR | Minimum deposit |

|---|---|---|

| Owner-occupier | 80% | 20% |

| Property investor | 65% | 35% |

The Reserve Bank’s LVR restrictions require investors to bring a 35% deposit to the table. Most investors fund this through equity in existing properties rather than cash savings, which is a legitimate strategy but requires careful documentation.

Key considerations for investor applications:

- Equity as deposit. If you are drawing on equity from an existing property, your lender will require a current valuation and confirmation that the combined LVR across both properties remains within acceptable limits.

- Portfolio DTI compliance. With the RBNZ DTI cap at 7 times income for investors, having multiple existing debts can significantly constrain what you can borrow for an additional property.

- Rental income treatment. Lenders typically use only 70–75% of projected rental income in their serviceability calculations, so relying on rental returns to carry the full mortgage repayment is rarely viable on paper.

- Stress testing at investor rates. Banks test investor loan serviceability at stress rates around 8–9%, which is even more conservative than owner-occupier testing.

Exceptions to the 65% LVR limit exist but are rare. Most lenders allocate only a small portion of their lending above threshold, and these spots are competitive. Building a strong financial profile across all other dimensions gives you a better shot if you do need to apply for one of those exceptions.

Practical tips to avoid common mortgage pitfalls

Even when your documents are in order and your finances look healthy, small oversights can weaken an otherwise solid application. Here is where many Kiwi borrowers lose ground in the final stretch:

Manage your credit enquiries carefully. Multiple credit applications in the months before a mortgage application signal financial stress to lenders, even if each enquiry was minor. Avoid applying for new credit cards, car loans, or any Buy Now Pay Later accounts for at least three to six months before submitting your mortgage application.

Review your bank statements proactively. Before your lender sees them, you should review three to six months of statements yourself. If there are irregular transactions, transfers, or cash withdrawals that look unusual, prepare a written explanation. Proactive transparency is far better than being caught off guard by a lender query mid-application.

Reduce or close unused credit cards. This is a point many borrowers miss. High credit card limits reduce borrowing capacity even when balances are zero, because lenders assess the potential liability of the full limit. Closing unused cards or reducing limits a few months before applying can meaningfully increase how much you are able to borrow. The same principle applies to BNPL accounts and store credit facilities.

Coordinate your timing. There is a specific sequence that works best: get your finances in order, gather your documents, seek pre-approval close to your intended purchase window, then make your offer. Breaking this sequence, such as making an offer before securing pre-approval, adds unnecessary risk.

Working with a mortgage adviser in Auckland or remotely across NZ gives you access to lender-specific knowledge that most borrowers simply don’t have. Different banks have different appetites for different borrower profiles, and a skilled adviser knows where to direct your application for the best chance of approval. This kind of insight is especially helpful for self-employed applicants or those with non-standard income.

Pro Tip: If you have rising interest rate concerns affecting your overall debt load, understanding how rate changes affect liabilities helps you prioritise which debts to reduce before applying.

My honest take on what really makes the difference

I have worked through hundreds of mortgage applications with Kiwi buyers, and the pattern I see repeatedly is this: borrowers who struggle are rarely struggling because they can’t afford a home. They are struggling because they walked in underprepared, at the wrong time, or with a financial story their bank statements didn’t support.

The paperwork is the floor, not the ceiling. Having every document ready and correct is the baseline expectation. What actually separates a smooth approval from a frustrating decline is the three months of behaviour that precede the application. The spending patterns, the credit decisions, the timing relative to income verification windows. All of this shapes what a lender sees.

I’ve also seen borrowers damage strong applications by seeking pre-approval too early, letting it expire, then reapplying during a period when their circumstances had quietly shifted. Lenders notice inconsistencies between applications. Aligning the timing between pre-approval and purchase is not just a formality. It is a genuine risk management decision.

One thing I believe strongly: the best mortgage application process is rarely something a borrower can fully optimise on their own. Not because it’s impossibly complex, but because lenders don’t advertise how they score applications, and each one has different tolerances. An adviser who knows which lender will look favourably on your specific profile, your income structure, your deposit source, is not a luxury. For many applicants, it is what gets the deal across the line.

— Stuart

How Mortgagemanagers helps you get approved

If this article has shown you anything, it’s that a better mortgage application is built long before you sign a sale and purchase agreement. At Mortgagemanagers, the team specialises in helping Kiwi buyers, whether you are purchasing your first home in Auckland or building an investment portfolio from Hobsonville to Hamilton, to put together a mortgage application that gives lenders exactly what they need to say yes.

As experienced mortgage advisers and personal shoppers for home loans, the Mortgagemanagers team matches your financial profile to the lender most likely to approve it, manages lender queries on your behalf, and gives you access to home loan options banks don’t always advertise. You pay nothing for this service. The lender does.

The smartest step you can take before you start looking at properties is to get professional mortgage advice early. It saves time, avoids costly missteps, and means you walk into the market knowing exactly what you can borrow and how to position your application for success.

Common questions

What documents do I need for a mortgage application in NZ?

You will typically need photo ID, proof of address, three months of payslips or two years of financials if self-employed, three to six months of bank statements, liabilities documentation, and deposit evidence including KiwiSaver details if applicable.

How does affordability testing affect my borrowing limit?

NZ lenders stress-test your repayment capacity at rates of 8.0 to 8.5%, and use the higher of your actual expenses or the HEM benchmark. This means your approved loan amount is often lower than your income alone would suggest.

How long does mortgage pre-approval last in New Zealand?

Pre-approvals are generally valid for 60 to 90 days and do not guarantee final approval. Submitting your application close to your intended purchase date and avoiding financial changes during this period protects its value.

Can high credit card limits affect my mortgage approval?

Yes. Lenders treat the full credit card limit as a potential liability, not just the balance. Reducing or closing unused credit cards before applying can improve your borrowing capacity.

Do property investors need a larger deposit than owner-occupiers?

Yes. Under Reserve Bank LVR rules, investors need a minimum 35% deposit, compared to 20% for most owner-occupiers. Many investors fund the difference through equity in existing properties.