TL;DR:

- A conditional offer in New Zealand involves clauses that must be satisfied within a set period to protect your deposit and rights, while an unconditional offer is a binding commitment with no further requirements. Going unconditional means you are legally obligated to complete the purchase, risking forfeiting your deposit and legal consequences if unable to do so. Properly understanding and coordinating pre-approval, conditional approval, and market timing are essential to making safe, strategic offers.

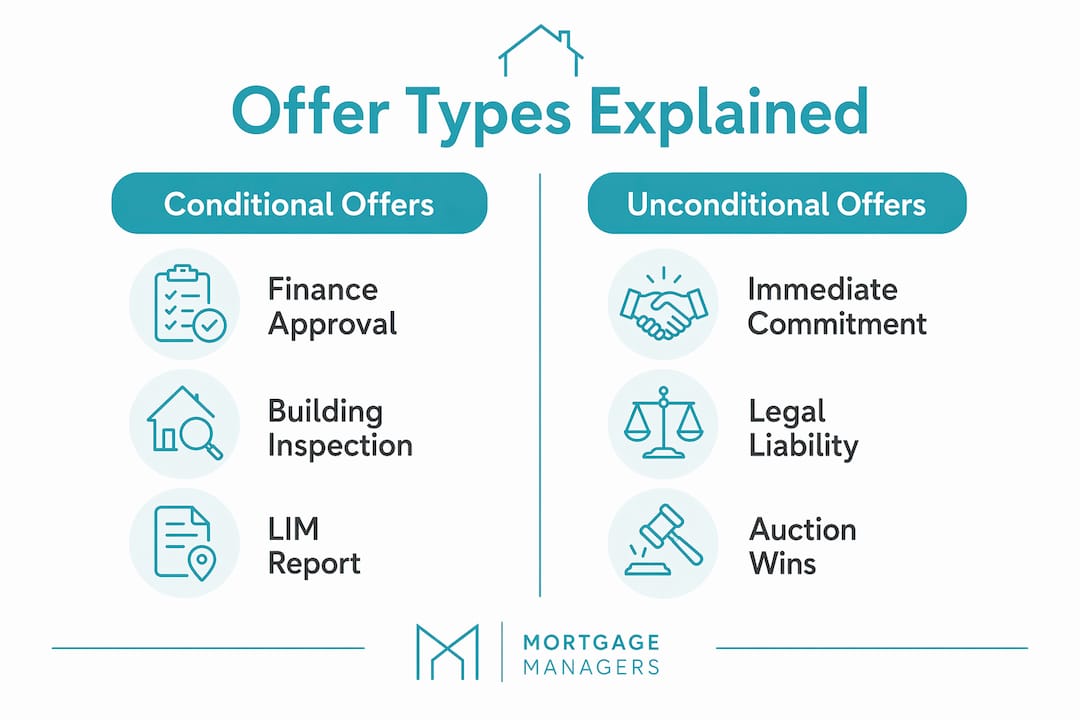

A conditional offer is a formal purchase agreement that includes specific clauses a buyer must satisfy before the sale proceeds, while an unconditional offer is a legally binding commitment with no further requirements attached. Understanding the difference between conditional vs unconditional offers is one of the most consequential decisions you will make as a New Zealand home buyer. Get it right and you protect your deposit, your due diligence, and your financial future. Get it wrong and you could forfeit your deposit or face legal action. This guide walks you through both offer types, the financing steps that connect them, and how to use each one strategically.

What conditions are commonly included in conditional offers?

A conditional offer in NZ is structured around “subject to” clauses that give you a defined window, typically 10 to 15 working days, to complete your due diligence before committing fully. These clauses are not just formalities. They are your legal safety net.

The three most common conditions are:

- Finance condition: This requires you to obtain formal loan approval from your lender for the specific property. Pre-approval is not enough here. You need conditional loan approval tied to that exact address before you can confidently waive this clause.

- Building inspection condition: A registered building inspector assesses the property’s physical condition, identifying structural issues, moisture problems, or deferred maintenance. This report can reveal thousands of dollars in hidden costs.

- LIM report condition: A Land Information Memorandum from the local council discloses consents, drainage, zoning, and any known hazards on the land. A clean LIM is not guaranteed, and surprises here can be deal-breakers.

If any condition is not met within the agreed timeframe, you can cancel the agreement and recover your deposit in full. This is the core protection a conditional offer provides. Importantly, if a building or LIM report reveals defects, you are not limited to simply walking away. Buyers can negotiate a reduced purchase price or require the vendor to carry out repairs before the agreement becomes unconditional. That negotiation leverage disappears the moment you go unconditional.

Pro Tip: Always request both a building inspection and a LIM report, even if the property looks immaculate. Issues uncovered during this window give you real bargaining power, not just an exit.

How do unconditional offers affect buyer and seller rights?

An unconditional offer is the point of no return in New Zealand property transactions. Once you waive your conditions in writing through your lawyer, no cooling-off period exists. You are legally obligated to complete the purchase.

The consequences of failing to complete an unconditional purchase are serious:

- You forfeit your deposit, which is typically 10% of the purchase price, paid within 2 to 3 working days of going unconditional.

- The vendor can pursue you for any shortfall if the property sells for less at a later date.

- Legal proceedings can follow, adding significant cost and stress on top of the financial loss.

For sellers, an unconditional offer delivers certainty. There is no risk of the deal falling over due to a failed finance condition or an unfavourable building report. This is why sellers in competitive markets, and particularly at auction, strongly prefer unconditional offers.

Going unconditional before completing all due diligence and confirming finance is one of the most costly mistakes a buyer can make. The legal and financial exposure is real and immediate.

Auctions in New Zealand are unconditional by default. If you bid and win, you are committed from the fall of the hammer. This means all your due diligence, including your building inspection, LIM report, and confirmed finance approval, must be completed before auction day. There are no exceptions.

Pre-approval vs conditional loan approval: what’s the difference?

Many buyers confuse mortgage pre-approval with conditional loan approval, and that confusion can create serious problems when it comes time to make an offer. They are distinct stages with very different implications.

| Stage | What it covers | Tied to a property? |

|---|---|---|

| Pre-approval | Assesses your income, expenses, and borrowing capacity broadly | No. Based on your finances only |

| Conditional loan approval | Formal approval linked to a specific property, subject to lender conditions | Yes. Tied to exact address, valuation, and insurance |

Pre-approval takes approximately 6 to 8 working days and remains valid for 60 to 90 days, provided your financial situation stays stable. It tells you what you can borrow in general terms. It does not mean a lender will approve a loan for any specific property you choose.

Conditional loan approval is property-specific. It requires you to submit your signed Sale and Purchase Agreement, a registered valuation, and proof of insurance. The lender then assesses the property as security for the loan. Changes in your income, the property’s valuation coming in below purchase price, or issues with the title can all cause a lender to withdraw approval at this stage.

This distinction matters enormously when you are deciding whether to include a finance condition in your offer. Pre-approval gives you confidence in your budget. Conditional loan approval is what actually satisfies a finance condition. Relying on pre-approval alone and waiving a finance condition is a significant risk, particularly if the property is unusual, the valuation is uncertain, or your financial circumstances are complex.

Pro Tip: Talk to a mortgage adviser before you make any offer. They can tell you how quickly your lender can move from pre-approval to conditional approval, which directly affects how long you need in your finance condition window.

How to use conditional and unconditional offers strategically

Choosing between a conditional and an unconditional offer is not just about risk tolerance. It is about reading the market, knowing your financial position, and working with the right professionals.

Use a conditional offer when:

- You have not yet completed a building inspection or obtained a LIM report on the property.

- Your conditional loan approval has not been confirmed for that specific property.

- The property has features that may affect its valuation, such as non-standard construction, a leaky building history, or unusual zoning.

- You are a first-home buyer using a Kāinga Ora First Home Loan or First Home Grant, which involves additional lender criteria and eligibility checks.

Consider an unconditional offer when:

- You have completed all due diligence prior to making the offer, as is required at auction.

- Your lender has provided conditional loan approval for a comparable property and you have high confidence the valuation will stack up.

- The market is highly competitive and a conditional offer is unlikely to be accepted.

Mortgage advisers bring real-time knowledge of lender criteria and turnaround times, which is especially valuable when you are trying to keep your finance condition window as short as possible to appeal to a seller. A shorter condition period signals confidence and seriousness. An adviser who knows a lender can turn around conditional approval in five working days gives you a genuine competitive edge over a buyer who needs ten.

For first-home buyers exploring government support schemes, the process involves additional eligibility checks that take time. Building that time into your condition period, rather than rushing to go unconditional, protects you from a situation where your grant or loan falls through after you have already committed.

Pro Tip: If you are competing in a multi-offer situation, ask your mortgage adviser whether your lender can provide a pre-approved valuation on the property before you submit. This can allow you to shorten or even waive the finance condition with genuine confidence rather than wishful thinking.

Key takeaways

Unconditional offers carry immediate legal and financial consequences in New Zealand, making thorough due diligence and confirmed finance approval non-negotiable before waiving any conditions.

| Point | Details |

|---|---|

| Conditional offer protection | Finance, building, and LIM conditions give you 10 to 15 working days to exit without losing your deposit. |

| Unconditional commitment | No cooling-off period exists in NZ. Failing to complete can mean forfeiting your deposit and facing legal action. |

| Pre-approval is not enough | Conditional loan approval is property-specific and required to safely waive a finance condition. |

| Negotiation window | Building or LIM report findings can be used to negotiate price or repairs before going unconditional. |

| Adviser advantage | A mortgage adviser’s knowledge of lender timelines helps you structure competitive condition periods without taking on unnecessary risk. |

Why I think buyers underestimate the unconditional moment

I have worked with many buyers across Auckland and wider New Zealand, and the pattern I see most often is this: buyers understand the theory of conditional offers but underestimate the weight of going unconditional. They treat it as a formality rather than a legal threshold.

The truth is that the moment you go unconditional, the entire dynamic of the transaction shifts. You no longer have leverage. You cannot renegotiate. You cannot walk away without real financial pain. I have seen buyers rush to go unconditional in a competitive market, only to discover the valuation came in short or the building report flagged significant remediation costs they had not budgeted for.

My honest advice is this: never go unconditional to win a property. Go unconditional because you have done the work and you are genuinely ready. The role of a mortgage adviser in this process is not just about finding a good interest rate. It is about making sure your finance is confirmed, your timelines are realistic, and you are not walking into a commitment you cannot complete.

First-home buyers in particular often feel pressure to compete with investors or experienced buyers by matching their unconditional offers. Resist that pressure. A conditional offer with a tight, well-structured condition period is a strong offer. You do not need to take on unlimited risk to be competitive.

— Stuart

How Mortgagemanagers can help you make the right offer

At Mortgagemanagers, we work with buyers across Auckland, West Auckland, the North Shore, and remotely throughout New Zealand to make sure your finance is in the right shape before you ever sign a Sale and Purchase Agreement. Our team understands lender timelines, valuation requirements, and the specific criteria that apply to first-home buyers using Kāinga Ora products.

When you work with us, we help you structure your finance condition period realistically, move quickly from pre-approval to conditional loan approval, and give you the confidence to make offers that are both competitive and safe. Whether you are buying at auction or negotiating a private sale, having a trusted mortgage adviser by your side means you never have to guess whether you are ready to go unconditional.

FAQ

What is a conditional offer in New Zealand?

A conditional offer is a property purchase agreement that includes clauses, such as finance, building inspection, or a LIM report, that must be satisfied within an agreed timeframe, typically 10 to 15 working days, before the sale proceeds.

What happens if I go unconditional and cannot complete the purchase?

You risk forfeiting your deposit, which is usually 10% of the purchase price, and the vendor can pursue legal action for any further losses. There is no cooling-off period in New Zealand once an offer is unconditional.

Is mortgage pre-approval enough to waive a finance condition?

No. Pre-approval is a broad assessment of your borrowing capacity. Conditional loan approval is property-specific and required to safely waive a finance condition, as it involves the lender assessing the property as security.

Can I negotiate after a building report reveals problems?

Yes. If a building or LIM report uncovers defects, you can negotiate a lower purchase price or require the vendor to carry out repairs before the agreement becomes unconditional. This negotiation must happen before you waive your conditions.

Do I need a mortgage adviser to make an offer on a property?

You are not legally required to use one, but a mortgage adviser provides real-time knowledge of lender criteria and turnaround times that can help you structure a competitive offer with a realistic condition period, reducing both risk and stress.