A lot of home buyers looking at the New Zealand property market quickly discover that mortgage options can be overwhelming and that is why knowing the role of mortgage brokers NZ is important and this article was written.

Understanding the unique role of mortgage brokers in New Zealand is crucial for anyone wanting more choice, clearer guidance, and stronger negotiating power when it comes to finding the best property financing solution.

Having a good mortgage broker is not just about getting the lowest home loan interest rates, but is about making sure that you have a home loan that will suit your situation and enable you to pay your home loan off faster – that’s how you really do save money!

Table of Contents

- What Mortgage Brokers Do In New Zealand

- Types Of Loans Brokers Can Arrange

- How Mortgage Application Process Works

- Legal Obligations And Fee Structures

- Comparing Brokers Versus Direct Lenders

Key Takeaways

| Point | Details |

|---|---|

| Role of Mortgage Brokers | Mortgage brokers in New Zealand assist clients in securing home loans by evaluating financial situations and recommending tailored mortgage solutions. |

| Types of Loans Available | Brokers can arrange various loan types including residential, investment, and specialist lending solutions tailored to individual financial needs. |

| Mortgage Application Process | Brokers simplify the mortgage application process, guiding clients through each stage to enhance the likelihood of approval. |

| Comparison with Direct Lenders | Unlike direct lenders, brokers access multiple lender networks, providing broader product options and personalised financial advice. |

What Mortgage Brokers Do In New Zealand

Mortgage brokers in New Zealand play a pivotal role in helping home buyers navigate the complex landscape of property financing. These financial professionals assist clients in securing home loans by comprehensively evaluating individual financial situations and recommending tailored mortgage solutions.

Their primary function involves acting as strategic intermediaries between borrowers and multiple lending institutions. Mortgage brokers analyse a client’s financial profile, credit history, income stability, and borrowing capacity to match them with appropriate loan options. This approach enables home buyers to access a broader range of mortgage products than they might discover independently, potentially saving significant money through more competitive interest rates and terms.

The key services mortgage brokers provide include:

- Comprehensive financial assessment and loan eligibility evaluation

- Comparison of mortgage products across multiple lenders

- Negotiation of competitive interest rates and loan conditions

- Guidance through complex application processes

- Personalised advice tailored to individual financial circumstances

Beyond simply connecting borrowers with lenders, these professionals offer strategic financial guidance. They help clients understand the nuances of different mortgage structures, explain potential risks and benefits, and provide ongoing support throughout the home loan journey. By leveraging their industry expertise and network of lending relationships, mortgage brokers transform what could be an overwhelming financial process into a manageable and informed experience for home buyers.

Types Of Loans Brokers Can Arrange

Mortgage brokers in New Zealand offer a diverse range of loan options designed to meet the unique financial needs of different borrowers. Various loan types are available to help individuals and investors achieve their property ownership goals, from first-time home buyers to experienced property investors.

The primary loan categories that mortgage brokers can arrange include residential mortgages, investment property loans, and specialist lending solutions. Borrowers can access multiple loan structures tailored to specific financial circumstances, such as:

- Fixed-Rate Mortgages: Loans with a consistent interest rate for a predetermined period

- Variable-Rate Mortgages: Loans where interest rates can fluctuate based on market conditions

- Interest-Only Loans: Temporary arrangements where borrowers pay only interest for an initial period

- Low Deposit Home Loans: Specialised options for first-time buyers with limited savings

- Investment Property Mortgages: Loans specifically designed for property investment strategies

Mortgage brokers excel at navigating non-standard lending options that traditional banks might not offer. These can include loans for self-employed professionals, individuals with complex income structures, or those with slightly imperfect credit histories. By working with a diverse network of lenders, brokers can help clients find financing solutions that might otherwise seem out of reach, transforming seemingly challenging borrowing scenarios into achievable property ownership opportunities.

How Mortgage Application Process Works

The mortgage application process can seem complex, but mortgage brokers simplify each critical stage for home buyers. Comprehensive financial assessment forms the foundation of a successful mortgage application, requiring careful preparation and strategic documentation.

A typical mortgage application involves several key stages:

- Initial Consultation: Detailed discussion of financial circumstances

- Financial Documentation Gathering:

- Proof of income

- Bank statements

- Credit history records

- Employment verification

- Loan Option Matching

- Application Submission

- Lender Assessment

- Final Approval

Mortgage brokers guide clients through each application stage, acting as strategic intermediaries between borrowers and financial institutions. Their expertise becomes particularly valuable when navigating complex lending criteria, helping clients understand potential challenges and optimise their application’s likelihood of approval. Preparing a mortgage application requires meticulous attention to detail, with brokers helping clients present their financial profile in the most compelling manner possible.

Legal Obligations And Fee Structures

Mortgage brokers in New Zealand operate under strict legal frameworks designed to protect consumers and ensure transparent financial advice. These professionals must be registered financial advisers, which means they are legally obligated to act in their clients’ best interests, provide clear information about their services, and maintain the highest standards of professional conduct.

The fee structures for mortgage brokers typically involve multiple compensation models:

- Lender Commission: Primary income source where lenders pay brokers for successful loan placements

- Client Service Fees: Direct charges to clients for comprehensive mortgage consultation

- Hybrid Fee Arrangements: Combination of lender commissions and client-paid service fees

Brokers are required to disclose all potential financial arrangements to maintain transparency and prevent conflicts of interest. This includes explaining exactly how they are compensated, whether through lender commissions, client fees, or a combination of both. Clients have the right to understand the full financial implications of working with a mortgage broker, ensuring they can make informed decisions about their lending strategy.

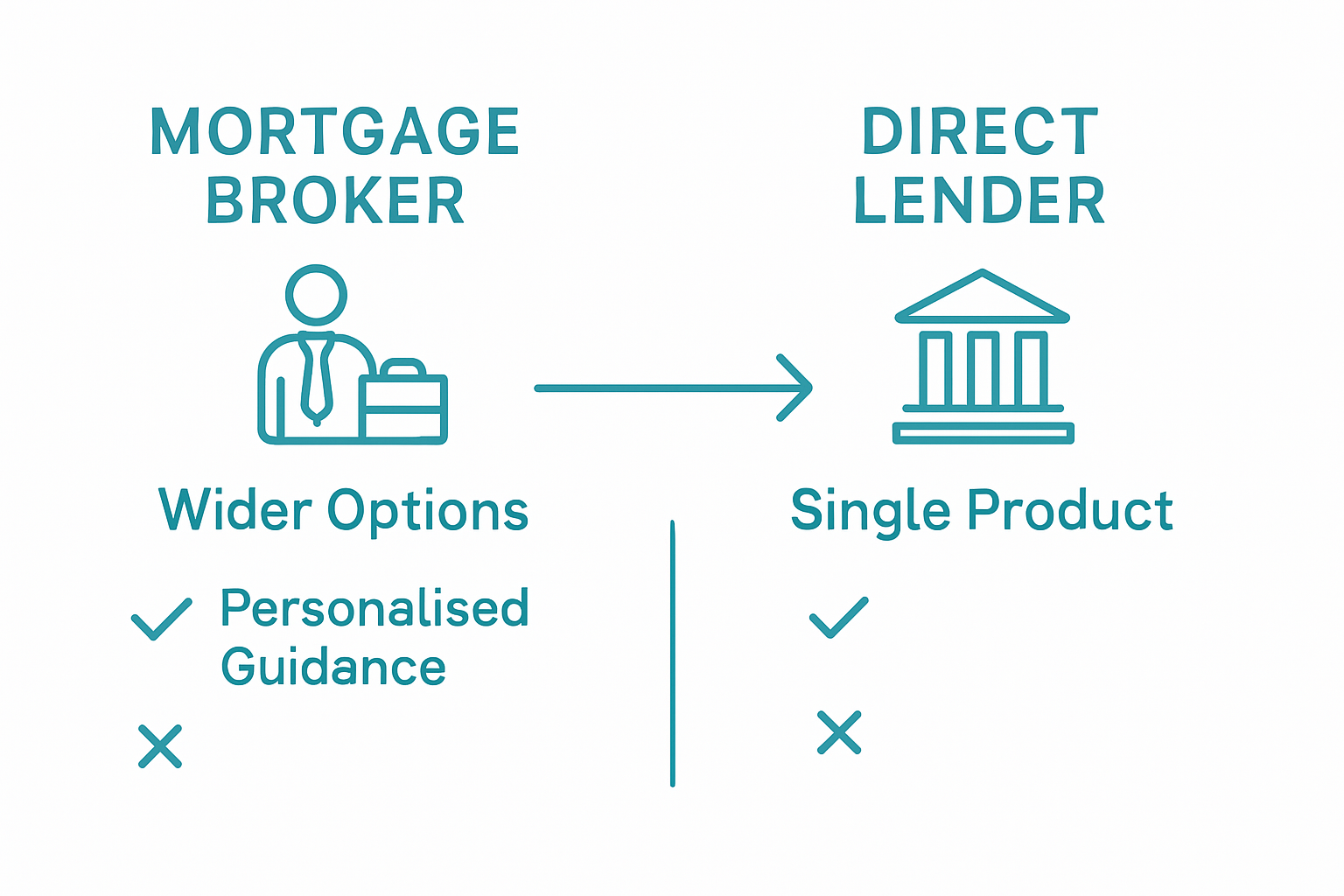

Comparing Brokers Versus Direct Lenders

Mortgage brokers offer a fundamentally different approach to lending compared to traditional direct lenders, providing home buyers with a more comprehensive and flexible financial solution. While direct lenders represent a single financial institution with limited product ranges, mortgage brokers act as strategic intermediaries who can access multiple lender networks.

Key differences between brokers and direct lenders include:

- Product Range:

- Direct Lenders: Limited to their own financial products

- Mortgage Brokers: Access to multiple lender offerings

- Personalisation:

- Direct Lenders: Standard application processes

- Mortgage Brokers: Tailored financial advice and matching

- Time Investment:

- Direct Lenders: Borrowers must approach each institution separately

- Mortgage Brokers: Streamlined application across multiple potential lenders

Brokers provide a strategic advantage by navigating complex lending landscapes, helping clients understand nuanced differences between loan products that direct lenders might not transparently explain. Their expertise allows home buyers to make more informed decisions, potentially saving thousands through better-matched financial products and more competitive interest rates.

Unlock the Benefits of Expert Mortgage Guidance with Mortgage Managers

Navigating the complex world of home loans can feel overwhelming for many New Zealand home buyers. The challenges of understanding varied mortgage types, assessing financial eligibility, and comparing multiple lenders are exactly where expert support makes a difference. If you want to avoid costly mistakes and gain personalised advice tailored to your unique financial situation, working with trusted mortgage brokers is essential.

Mortgage Managers are based in Hobsonville where we are servicing Auckland and beyond. We specialise in acting as your strategic partner throughout the mortgage journey, from getting your first home loan approved to comparing fixed-rate and variable options to exploring specialist lending solutions.

Our advisers provide expert insights that align with your property ownership goals.

Don’t let uncertainty hold you back—take advantage of our in-depth financial assessments and streamlined application guidance today. Visit Mortgage Managers to start securing your future home with confidence now.

Frequently Asked Questions

What services do mortgage brokers provide for home buyers?

Mortgage brokers assist home buyers by evaluating their financial situations, comparing mortgage products from multiple lenders, negotiating competitive interest rates, guiding them through the application process, and providing personalised financial advice.

How do mortgage brokers differ from direct lenders?

Mortgage brokers act as intermediaries who access a variety of loan options from different lenders, while direct lenders offer only their own financial products. Brokers provide tailored advice and streamline the application process across multiple lenders.

What types of loans can mortgage brokers help arrange?

Mortgage brokers can arrange various loan types including fixed-rate mortgages, variable-rate mortgages, interest-only loans, low deposit home loans, and investment property mortgages, catering to different financial needs and circumstances.

What is the mortgage application process with a broker?

The application process typically involves an initial consultation, gathering financial documentation, matching loan options, submitting the application, lender assessment, and final approval, with brokers guiding clients at each stage.

Recommended

- Mortgage Broker NZ: Complete Guide for Home Buyers

- Discover the Best Mortgage Brokers in New Zealand – Mortgage Managers

- Find A Mortgage Broker In Auckland – Mortgage Managers

- Good New Zealand Mortgage Brokers Help Real Estate Agents

- Comprendre le fonctionnement du prêt relais en immobilier – LPI: La parisienne immobilière agence immobilière Paris 19

- 7 Essential Tips for First Home Buyers in Melbourne – Onyx Removals

- Is a Pre-Completion Snagging Inspection (PCI) Really Worth It?