TL;DR:

- In 2025, the Reserve Bank of New Zealand’s LVR rules limit owner-occupier lending above 80% LVR to 25% of new commitments and investor lending above 70% LVR to 10%, shaping deposit requirements and lender availability.

- However, exemptions for new builds and government schemes like Kāinga Ora enable higher LVRs, especially for first home buyers, with careful pre-application planning recommended.

Loan-to-value ratio (LVR) rules in 2025 are the Reserve Bank of New Zealand’s primary tool for controlling how much high-deposit-risk lending banks can issue. The RBNZ caps owner-occupier lending above 80% LVR at 25% of new commitments, and investor lending above 70% LVR at just 10%. These thresholds directly shape how much deposit you need and how many lenders will consider your application. Whether you are buying your first home in Auckland or adding to a property portfolio, understanding these 2025 LVR regulations is the clearest path to knowing where you stand.

What are the LVR limits and speed limits in 2025?

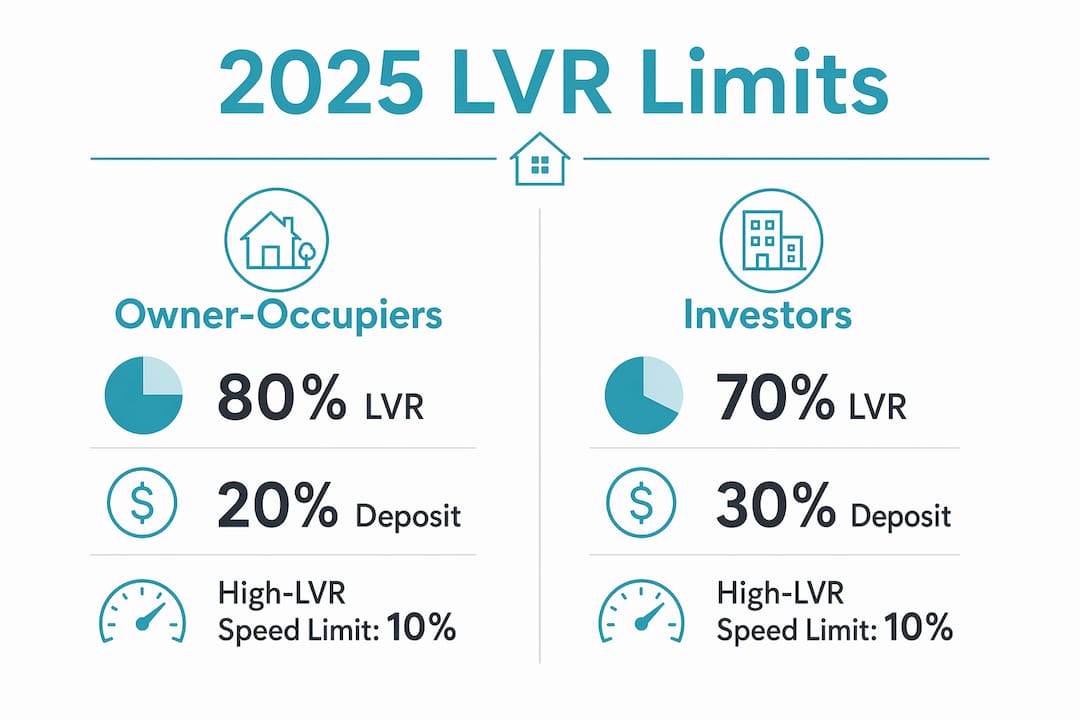

The core LVR settings set by the RBNZ establish two distinct thresholds depending on your borrower type. Owner-occupiers face an 80% LVR cap, meaning you need at least a 20% deposit to borrow at the standard rate. Investors face a stricter 70% LVR cap, requiring a minimum 30% deposit. These are not absolute ceilings, but they define the boundary above which lending becomes tightly restricted.

The “speed limit” concept is where things get more nuanced. Banks are permitted to lend above these thresholds, but only up to a set proportion of their total new lending each quarter. For owner-occupiers, up to 25% of new commitments can sit above the 80% LVR mark. For investors, only 10% of new lending can exceed the 70% threshold. Think of it as a quota system. Once a bank fills its high-LVR quota for the quarter, no more exceptions are available until the next period begins.

| Borrower type | Standard LVR limit | Minimum deposit | Speed limit (high-LVR allowance) |

|---|---|---|---|

| Owner-occupier | 80% | 20% | 25% of new lending |

| Investor | 70% | 30% | 10% of new lending |

| New build owner-occupier | 90% | 10% | Exempt from speed limit |

| New build investor | 80% | 20% | Exempt from speed limit |

In practice, this means that even if you technically qualify for a high-LVR loan, your bank may not have capacity to approve it. Investor properties require a minimum 35% deposit in most standard cases, with only a narrow slice of lending permitted above that threshold. The quota fills faster than many borrowers expect, particularly during periods of strong market activity.

Pro Tip: Ask your lender or mortgage adviser where they sit against their quarterly high-LVR quota before you apply. Timing your application early in a quarter can meaningfully improve your chances of approval.

How do new builds and government schemes affect LVR requirements?

New builds are the most significant exemption within the 2025 LVR framework. Unlike existing properties, new builds are not subject to the speed limit restrictions that cap high-LVR lending. This means new builds allow higher LVRs for both owner-occupiers and investors, with owner-occupiers able to borrow up to 90% LVR and investors up to 80%. The practical effect is a much lower deposit requirement, which opens the door for buyers who cannot yet reach the standard 20% or 30% threshold.

There are a few things worth understanding clearly about this exemption:

- New build exemptions apply to properties that have not previously been lived in, typically defined as newly constructed dwellings or those purchased off the plan.

- Banks still apply their own risk appetite to new build lending. The RBNZ permits higher LVRs, but individual lenders are not obligated to approve them. Not all banks will lend at 90% LVR on a new build even when the rules allow it.

- Valuations on new builds can be unpredictable, particularly for off-the-plan purchases where the final value may differ from the contracted price.

- Settlement risk is real. If your financial situation changes between signing and settlement, the bank may reassess your application under tighter criteria.

Government-backed schemes add another layer of access for eligible buyers. The Kāinga Ora First Home Loan allows eligible buyers to purchase with as little as a 5% deposit by underwriting the high-LVR risk on behalf of the bank. This effectively removes the deposit barrier for first home buyers who meet the income and property price criteria. The scheme does not override LVR rules but works within them by shifting the risk exposure away from the lender.

Pro Tip: If you are considering a new build to access the higher LVR exemption, get pre-approval confirmed with your chosen lender before signing a sale and purchase agreement. Bank appetite for 90% LVR new build lending varies, and you do not want to be caught without finance at settlement.

How do banks apply LVR rules alongside debt-to-income limits?

LVR is one layer of a multi-criteria lending assessment. Understanding LVR changes in isolation misses the fuller picture of what banks actually evaluate when approving a mortgage. Since July 2024, DTI restrictions cap borrowing at 6 times income for owner-occupiers and 7 times income for investors. This means even if your deposit clears the LVR threshold, your total debt load relative to your income must also sit within these limits.

The layered nature of these criteria creates a compounding effect that catches many borrowers off guard. Here is how the approval process typically works in sequence:

- LVR check. Does your deposit meet the standard threshold? If not, does the bank have high-LVR quota available?

- DTI check. Does your total proposed debt (including the new mortgage) sit within 6 or 7 times your gross income?

- Serviceability test. Can you afford repayments if interest rates rise? Banks apply stress tests at typically 2 to 3 percentage points above current market rates to assess repayment resilience.

- Credit and conduct assessment. Your credit history, existing liabilities, and spending patterns are reviewed.

“Many borrowers focus entirely on saving a deposit and assume that meeting the LVR threshold is the finish line. In reality, DTI limits and serviceability tests are where applications most commonly stall.”

The interaction between LVR and DTI is particularly relevant for investors. An investor purchasing a second property may clear the 70% LVR requirement with a 30% deposit but find that their combined debt across both properties exceeds 7 times their income. At that point, the DTI cap becomes the binding constraint, not the LVR. Understanding which rule is actually limiting your borrowing is the first step to addressing it. For a broader look at how these criteria interact, the 2025 mortgage trends guide for NZ first home buyers covers the full picture well.

What practical steps help borrowers navigate the 2025 LVR rules?

The impact of LVR rules on your mortgage approval is real, but it is not insurmountable. The borrowers who succeed under these settings are the ones who prepare deliberately rather than apply and hope. Here are the most effective steps you can take:

- Engage a mortgage adviser early. Advisers know which lenders have high-LVR quota remaining, which banks are most receptive to new build applications, and how to structure your application to meet DTI limits. This knowledge is not publicly available and changes week to week.

- Reduce existing debts before applying. Credit card limits, personal loans, and buy-now-pay-later balances all count against your DTI calculation, even if you carry no balance. Closing unused credit facilities before applying can meaningfully shift your DTI ratio.

- Consider a new build if your deposit is limited. The exemption from speed limits gives new builds a structural advantage for buyers with 10% to 20% deposits. This is particularly relevant in Auckland where new townhouse developments are actively marketed to first home buyers.

- Shop across multiple lenders. High-LVR quota fills at different rates across different banks. ANZ, ASB, BNZ, Westpac, and Kiwibank each manage their own internal quotas independently. One bank being at capacity does not mean all banks are.

- Prepare documentation that demonstrates financial resilience. Lenders want to see stable income, manageable expenses, and a savings history. Three to six months of bank statements showing consistent savings behaviour strengthens your application against the serviceability test.

Pro Tip: If you are an investor, calculate your DTI ratio before approaching any lender. Add up all your current debt (mortgages, car loans, personal loans) and divide by your gross annual income. If the result is above 6, address that before applying rather than discovering it mid-assessment.

For a detailed walkthrough of how to structure your application under current criteria, the mortgage application guide for Kiwis covers the practical steps thoroughly.

Key takeaways

The 2025 LVR rules set firm deposit thresholds for owner-occupiers and investors, but new build exemptions, government schemes, and careful application timing create genuine pathways for borrowers who plan ahead.

| Point | Details |

|---|---|

| Owner-occupier LVR limit | Standard cap is 80% LVR, requiring a minimum 20% deposit for most purchases. |

| Investor LVR limit | Standard cap is 70% LVR, with only 10% of bank lending permitted above this threshold. |

| New build advantage | Owner-occupiers can access up to 90% LVR on new builds, exempt from speed limit quotas. |

| DTI rules compound LVR | Borrowing is also capped at 6 times income for owner-occupiers and 7 times for investors. |

| Timing and lender choice matter | High-LVR bank quotas fill during busy periods, so applying early and across multiple lenders improves approval chances. |

LVR policy is a moving target: my honest view

The thing I see borrowers get wrong most often is treating the current LVR settings as permanent fixtures. They are not. LVR settings are dynamic tools that the RBNZ adjusts based on house price growth, credit conditions, and broader financial stability concerns. The settings we have now reflect a particular moment in the market cycle. They can tighten again if house prices accelerate, or ease further if the market cools.

What this means practically is that planning your borrowing around an assumption of future easing is a risky strategy. I have seen borrowers delay applications waiting for rules to loosen, only to find conditions tightened instead. The conservative approach is to plan for the rules as they stand today and treat any future easing as a bonus rather than a baseline.

The other thing worth saying plainly is that many borrowers underestimate DTI rules when assessing their borrowing capacity. They focus on the deposit and assume LVR compliance is the hard part. In my experience, DTI is where well-prepared borrowers with solid deposits still get caught out, particularly investors with existing mortgages. Knowing your DTI ratio before you walk into a lender conversation is not optional. It is the foundation of a credible application.

The borrowers who navigate these settings well are not necessarily the ones with the biggest deposits. They are the ones who understand the full picture, engage professional advice early, and approach the process with realistic expectations and a clear plan.

— Stuart

How Mortgagemanagers can help you find the right path

Knowing the rules is one thing. Knowing how to work within them to get your mortgage approved is another matter entirely.

At Mortgagemanagers, our Auckland-based mortgage advisers work with first home buyers, investors, and everyone in between to find the right lending solution under the current regulatory framework. We know which lenders have high-LVR capacity, how to structure applications to meet DTI limits, and which new build or government scheme options suit your situation. As your personal mortgage shoppers, we do the legwork across multiple lenders so you do not have to. Get in touch with the Mortgagemanagers team today and take the guesswork out of your mortgage planning.

FAQ

What is the LVR limit for owner-occupiers in 2025?

The standard LVR limit for owner-occupiers is 80%, meaning you need at least a 20% deposit. Banks can lend above this threshold, but only up to 25% of their total new lending commitments per quarter.

Do investors face stricter LVR requirements than owner-occupiers?

Yes. Investors face a 70% LVR cap, requiring a minimum 30% deposit, with only 10% of new bank lending permitted above that level. This makes high-LVR investor lending significantly harder to access than owner-occupier lending.

Are new builds exempt from LVR speed limits?

New builds are exempt from the speed limit restrictions, allowing owner-occupiers to borrow up to 90% LVR and investors up to 80%. However, individual banks still apply their own risk criteria and are not required to approve lending at these higher levels.

How does the Kāinga Ora First Home Loan help with LVR requirements?

The Kāinga Ora First Home Loan allows eligible buyers to purchase with as little as a 5% deposit by underwriting the high-LVR risk on behalf of participating banks. It does not override LVR rules but removes the deposit barrier for qualifying first home buyers.

Can DTI limits stop my mortgage even if I meet the LVR threshold?

Yes. DTI restrictions cap total borrowing at 6 times gross income for owner-occupiers and 7 times for investors. If your combined debt exceeds these multiples, your application can be declined regardless of your deposit size or LVR compliance.