TL;DR:

- A serviceability assessment evaluates your ability to repay a home loan based on income, expenses, debts, and stress-test interest rates. Lenders apply different policies, and passing both the stress test and DTI cap is essential for approval, with preparation improving your chances. Understanding these factors and optimizing your financial profile can significantly increase your borrowing capacity.

A serviceability assessment is a lender’s formal evaluation of your ability to repay a home loan, calculated using your income, living expenses, existing debts, and a stress-tested interest rate. Every New Zealand bank and non-bank lender runs this check before approving a mortgage, and your result directly determines how much you can borrow. Understanding how it works gives you a real advantage before you ever walk into a lender’s office.

In 2026, New Zealand lenders apply stress-test rates of around 8.0% to 9.0%, which sits roughly 2% to 3% above current market rates. That gap is deliberate. Lenders want to know you can still meet repayments if interest rates climb after you settle. The Reserve Bank of New Zealand (RBNZ) and the Credit Contracts and Consumer Finance Act (CCCFA) both shape how rigorously lenders must conduct these checks, making serviceability one of the most consequential filters in the home loan process.

What are serviceability assessments and what do lenders actually check?

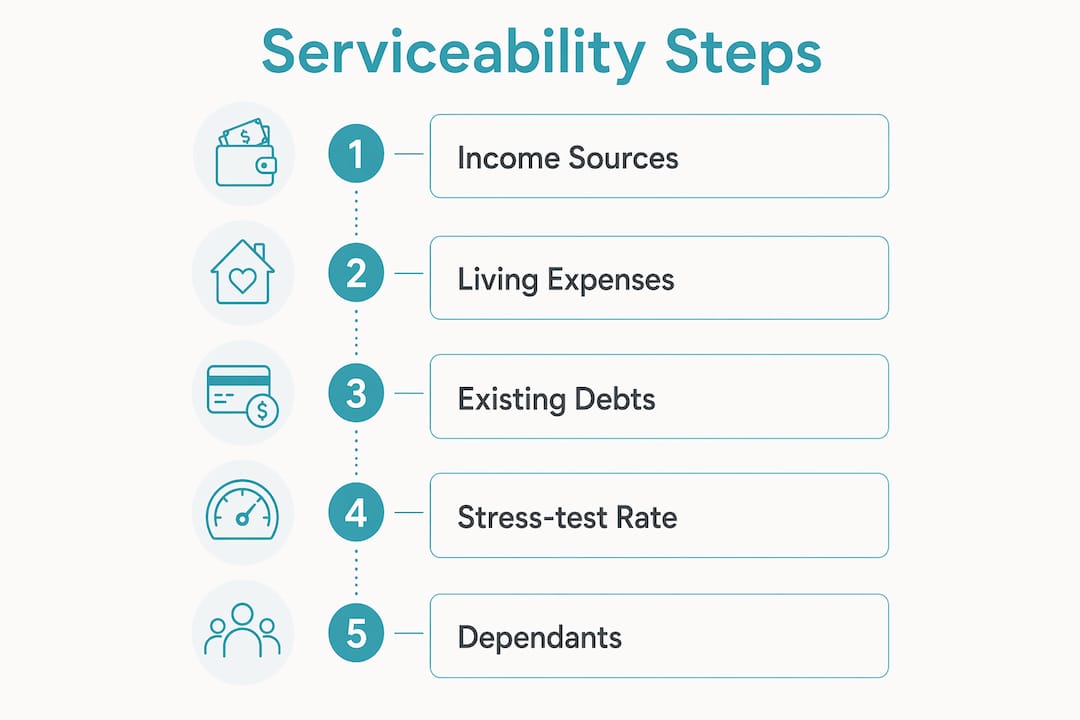

Serviceability assessments are the structured process lenders use to confirm your finances can support a mortgage, not just today, but under pressure. The assessment pulls together several financial inputs and runs them through the lender’s internal model to produce a maximum loan figure.

Income sources and how lenders treat them

Lenders accept a range of income types, but not all income carries equal weight. Base salary from permanent employment is counted at full value. Variable income, including overtime, bonuses, and commission, is often discounted to 80% or less because it is not guaranteed month to month. Rental income from investment properties is typically counted at 80% of gross rent to allow for vacancy and maintenance costs. Self-employed income requires at least two years of financial statements, and lenders will average those figures rather than use the most recent year alone.

Living expenses and the HEM benchmark

Lenders assess your living costs using either your declared expenses or an internal benchmark called the Household Expenditure Measure (HEM), and they always apply whichever figure is higher. The HEM is scaled by household size, so a couple with two children will face a higher benchmark than a single applicant. This prevents borrowers from understating their costs to inflate their borrowing capacity. If your declared expenses are genuinely lower than the HEM, the lender will use the HEM regardless.

Existing debts and credit limits

Every debt you carry reduces your serviceability. Lenders include personal loans, car finance, student loans, and credit card limits in their calculations. Credit card limits are treated as potential repayments of 3% to 5% of the total limit, regardless of whether you carry a balance. A $10,000 credit card limit you never use can still reduce your borrowing capacity by tens of thousands of dollars. Buy now, pay later (BNPL) obligations such as Afterpay or Laybuy are also factored in under CCCFA requirements.

Dependants and the stress-test rate

Each dependant in your household adds to the lender’s estimated living costs, which reduces the surplus income available for mortgage repayments. The stress-test rate is then applied to the proposed loan amount to calculate the repayment figure used in the assessment. Because buffers average 2% to 3% above current rates, your assessed repayment is significantly higher than what you would actually pay at today’s rates.

Pro Tip: Before applying, request a breakdown of your current credit card limits and BNPL accounts. Reducing or closing unused credit facilities can meaningfully lift your borrowing capacity without changing your income.

How do serviceability tests and the RBNZ’s DTI limit work together?

New Zealand borrowers must clear two separate hurdles to get a mortgage approved: the serviceability stress test and the RBNZ’s Debt-to-Income (DTI) ratio cap. Understanding how they interact is critical because either one can be the binding constraint on your loan size.

The DTI limit sits at 6 times gross annual income for most owner-occupier applicants, a rule the RBNZ introduced in July 2024. If your household earns $120,000 per year, the DTI cap limits your total debt to $720,000. That figure includes all existing debts, not just the new mortgage. A car loan of $30,000 and a personal loan of $20,000 would reduce your available mortgage capacity to $670,000 under the DTI rule alone.

The serviceability test works differently. It calculates whether your income, after living expenses and existing debt repayments, leaves enough surplus to cover the stress-tested mortgage repayment. The lender then approves the lower of the two figures: the DTI maximum or the serviceability maximum. Borrowers must pass both tests to receive approval, and in practice, one will almost always be tighter than the other depending on your financial profile.

| Constraint | What it measures | Binding for whom |

|---|---|---|

| DTI cap (6× income) | Total debt relative to gross income | High earners with large existing debts |

| Serviceability test | Monthly cash flow after expenses and stress-tested repayments | Borrowers with high living costs or variable income |

| Combined effect | Lender approves the lower of the two limits | Most applicants face one as the primary barrier |

For a first home buyer with no existing debts and modest living costs, the serviceability test is usually the tighter constraint. For someone carrying a car loan, credit card debt, and a student loan, the DTI cap may kick in first. Reviewing your 2026 mortgage application with both limits in mind gives you a clearer picture of where you actually stand.

Pro Tip: Calculate your own DTI before approaching a lender. Add up all your current debts, divide by your gross annual income, and compare the result to 6. If you are already close to that threshold, paying down debt before applying will have a direct impact on your maximum loan.

Why do different lenders calculate serviceability differently?

There is no universal calculation standard for serviceability assessments across New Zealand lenders. Each institution sets its own stress-test rate, living expense benchmarks, income discounting policies, and debt treatment rules. The result is that your borrowing capacity can vary by $50,000 or more depending on which lender you approach.

These differences show up in several specific ways:

- Stress-test rates: One lender may test at 8.5% while another uses 9.0%. That half-percent difference compounds significantly over a $600,000 loan.

- Income treatment: Some lenders accept 100% of a regular bonus if it has been paid for two consecutive years. Others cap all variable income at 80% regardless of history.

- Living expense benchmarks: The HEM figures lenders use are not publicly disclosed and vary between institutions. A lender with a lower internal benchmark will calculate a higher surplus income and therefore approve a larger loan.

- Credit card treatment: Most lenders count the full credit limit, but the repayment rate applied (3% versus 5%) affects the monthly liability figure used in the assessment.

- BNPL and short-term debt: Some lenders exclude small BNPL balances below a threshold; others include every active account.

This variation is not a flaw in the system. It reflects genuine differences in risk appetite and lending policy. For you as a homebuyer, it means the first lender you speak to is not necessarily the one that will offer you the best outcome. Reviewing NZ mortgage trends for first home buyers helps you understand which lender policies are shifting and where opportunities exist.

How can you improve your serviceability assessment outcome?

Your serviceability result is not fixed. Several practical steps taken in the months before you apply can lift your borrowing capacity and improve your chances of approval.

-

Reduce or close unused credit facilities. Credit card limits count against you even at zero balance. Closing a $15,000 card you rarely use can add meaningful capacity to your assessment. The same applies to BNPL accounts with Afterpay, Laybuy, or Zip.

-

Pay down existing debts. Every dollar of personal loan or car finance you eliminate reduces the monthly liability figure lenders use in their calculations. Focus on high-interest, short-term debts first for the fastest impact on serviceability.

-

Document your income thoroughly. Lenders want consistency. Payslips covering the last three months, your most recent two years of tax returns if self-employed, and a letter from your employer confirming your employment type all strengthen your file. Gaps in documentation lead to conservative income assessments.

-

Review your bank statements before the lender does. Under CCCFA affordability requirements, lenders scrutinise your transaction history for patterns. High discretionary spending, online gambling transactions, or irregular income deposits can raise concerns. Three months of clean, consistent statements makes a strong impression.

-

Declare expenses accurately. Understating your living costs does not help you. Lenders apply the HEM benchmark if your declared expenses fall below it, and inaccurate declarations can trigger compliance concerns under the CCCFA.

-

Work with a mortgage adviser. An adviser who knows which lenders apply more favourable income treatment or lower living expense benchmarks can match your profile to the right institution from the start. This saves time and protects your credit file from multiple hard enquiries.

Pro Tip: Start your preparation at least three to six months before you plan to apply. Improving your serviceability profile takes time, and lenders look at patterns, not just a single month’s figures.

Practical strategies for improving home loan eligibility are worth reviewing alongside these steps, particularly if you are managing existing debt obligations.

Key takeaways

Serviceability assessments determine your maximum borrowing capacity by measuring your income against stress-tested repayments, living expenses, and existing debts, and every New Zealand homebuyer must pass both the serviceability test and the RBNZ’s DTI cap to secure a mortgage.

| Point | Details |

|---|---|

| Stress-test rates in 2026 | Lenders test at 8.0% to 9.0%, roughly 2% to 3% above current market rates. |

| DTI cap applies alongside serviceability | The RBNZ’s 6× income DTI limit restricts total debt, independent of cash flow tests. |

| Lender variation is significant | Borrowing capacity can differ by $50,000 or more between lenders due to policy differences. |

| Credit limits reduce capacity | Unused credit card and BNPL limits count as liabilities regardless of actual balance. |

| Preparation improves outcomes | Reducing debts, cleaning bank statements, and documenting income lifts your assessed capacity. |

Stuart’s take on serviceability in New Zealand’s current market

What I see most often is first home buyers who are genuinely surprised by how much the stress-test rate reduces their borrowing power. You might be paying 6.5% on your mortgage today, but the lender is assessing your ability to repay at 8.5% or higher. That gap can cut tens of thousands of dollars off your approved loan amount, and it catches people off guard when they have been budgeting based on current rates.

The DTI rules introduced in July 2024 added another layer of complexity that many buyers still do not fully account for. I have seen situations where a borrower’s serviceability test result was perfectly fine, but their existing car loan and credit card debt pushed them over the 6× DTI threshold. The solution was straightforward once we identified it, but without that analysis upfront, they would have applied to the wrong lender and faced a decline.

The most underrated advantage a homebuyer has is lender choice. Because there is no universal serviceability standard, the right lender for your specific income structure and debt profile can make a material difference to your outcome. That is not about finding a lender who cuts corners. It is about finding one whose policies align with your genuine financial position. Working with an adviser who knows those policies in detail is the most direct path to a well-matched application.

The CCCFA reforms have also made bank statement scrutiny far more rigorous than it was five years ago. Discretionary spending patterns that would have gone unnoticed before are now reviewed carefully. I always recommend clients take a hard look at three months of transactions before applying, not to hide anything, but to understand what the lender will see and address anything that looks inconsistent.

— Stuart

How Mortgagemanagers can help you navigate serviceability

Understanding serviceability rules is one thing. Applying them to your specific financial situation, across multiple lenders with different policies, is where expert guidance pays off.

Mortgagemanagers works with homebuyers across Auckland, the North Shore, West Auckland, and remotely throughout New Zealand to assess your borrowing capacity against current lender criteria. The team stays current on 2026 stress-test rates, RBNZ DTI limits, and CCCFA requirements so you receive advice grounded in today’s lending environment, not last year’s rules. Whether you are a first home buyer or returning to the market, a personalised assessment of your serviceability position is the clearest starting point. Speak with a mortgage adviser at Mortgagemanagers to understand exactly where you stand and which lenders are best suited to your profile.

FAQ

What is a serviceability assessment in New Zealand?

A serviceability assessment is a lender’s evaluation of whether your income, after living expenses and existing debt repayments, is sufficient to cover mortgage repayments at a stress-tested interest rate. In New Zealand, lenders apply test rates of around 8.0% to 9.0% in 2026 to assess this capacity.

How does the RBNZ’s DTI limit affect my borrowing capacity?

The RBNZ’s Debt-to-Income cap limits most owner-occupier borrowers to total debt of no more than 6 times their gross annual income. This operates separately from the serviceability test, and lenders approve only the lower of the two limits.

Why do different lenders offer different borrowing amounts?

Lenders set their own stress-test rates, income discounting policies, and living expense benchmarks, which means your assessed borrowing capacity can vary by $50,000 or more between institutions. There is no single universal serviceability calculation in New Zealand.

Do credit cards affect my serviceability assessment?

Yes. Lenders treat your total credit card limit as a liability, typically calculating a monthly repayment of 3% to 5% of the limit regardless of your actual balance. Reducing or closing unused credit cards before applying can improve your serviceability result.

Can I improve my serviceability assessment before applying?

You can improve your result by paying down existing debts, closing unused credit facilities, maintaining consistent income documentation, and reviewing your bank statements for discretionary spending patterns that lenders scrutinise under CCCFA affordability requirements.