TL;DR:

- Home loan pre qualification estimates your borrowing capacity based on unverified financial data, helping you plan your property search. It differs from pre approval, which involves a credit check and provides a conditional commitment from the lender. Preparing accurate documents and improving financial stability increase your chances of obtaining a strong pre qualification and subsequent pre approval.

Home loan pre qualification is a conditional financial estimate that shows how much a lender may be willing to lend you, based on your current income, debts, and deposit. Think of it as your financial compass before you start property hunting. In New Zealand, this process sits under the framework of the Credit Contracts and Consumer Finance Act (CCCFA), which governs responsible lending obligations. Knowing your borrowing capacity early means you search with confidence, not guesswork. Pre qualification is distinct from mortgage pre approval, which involves verified documents and a formal credit check. Pre-approval letters in NZ are typically valid for 60–90 days, giving you a clear window to make offers. Getting this step right sets the tone for your entire home buying experience.

What is home loan pre qualification and how does it differ from pre approval?

Pre qualification and mortgage pre approval are two different stages of the same process, and confusing them costs buyers time and negotiating power. Understanding both gives you a real edge in the NZ property market.

Pre qualification often requires no credit check and is based on unverified, self-reported financial data. That means it is a quick estimate, not a commitment. Pre approval, by contrast, involves a full credit check, verified payslips, bank statements, and a conditional lending decision from the lender. Pre approval carries significantly more weight when you make an offer on a property.

The table below shows the core differences at a glance.

| Feature | Pre qualification | Pre approval |

|---|---|---|

| Credit check required | No | Yes |

| Based on verified data | No | Yes |

| Lender commitment | Estimate only | Conditional commitment |

| Negotiation strength | Low | High |

| Processing time | Same day to 48 hours | 2–8 working days |

Mortgage pre approval is key for serious buyers in New Zealand who want to negotiate confidently and make competitive offers. That said, pre qualification is the right first step. It costs you nothing, takes minimal time, and tells you whether it is worth proceeding to full pre approval.

Pro Tip: Start with pre qualification to get a realistic budget range, then move to pre approval before you attend open homes. Sellers and agents take pre approved buyers far more seriously.

What documents and eligibility criteria do NZ lenders require?

Lenders in New Zealand assess several core factors when you apply for pre qualifying for a mortgage. Meeting these criteria cleanly is the fastest path to a positive outcome.

Core eligibility criteria

To be eligible, you generally need to be at least 18 years old, a New Zealand citizen, permanent resident, or hold an eligible visa, and have a stable, verifiable income. Your employment status matters significantly. Permanent employees, contractors, and self-employed applicants are all assessed differently, with self-employed buyers facing closer scrutiny of their financial history.

Lenders also assess your loan-to-value ratio (LVR), which is the size of your loan compared to the property value. Most NZ lenders prefer a 20% deposit, though some products allow deposits as low as 5–10% with income caps and higher interest margins. A lower deposit means more risk for the lender, which often translates to stricter conditions for you.

Required documentation

Applicants need to provide photo ID, 3–6 months of bank statements, the last 3 months of payslips, proof of deposit, and a full list of liabilities. Self-employed buyers must also supply two years of financial statements. Having these ready before you apply removes delays and signals to lenders that you are organised and serious.

The full document checklist includes:

- Valid photo ID (passport or driver’s licence)

- Last 3 months of payslips (or 2 years of financial statements if self-employed)

- 3–6 months of bank statements from all accounts

- Evidence of your deposit (savings history, KiwiSaver balance, or gift letter)

- Details of existing debts (credit cards, personal loans, car finance, student loans)

- Proof of any additional income (rental income, investments, or benefits)

Pro Tip: Create a single digital folder with all your documents before you contact any lender. Lenders respond faster when you can supply everything in one go, and it reduces the risk of your application stalling mid-process.

Accuracy matters as much as completeness. Lenders cross-check your declared income and expenses against your bank statements. Inconsistencies, even minor ones, raise red flags and slow the process down.

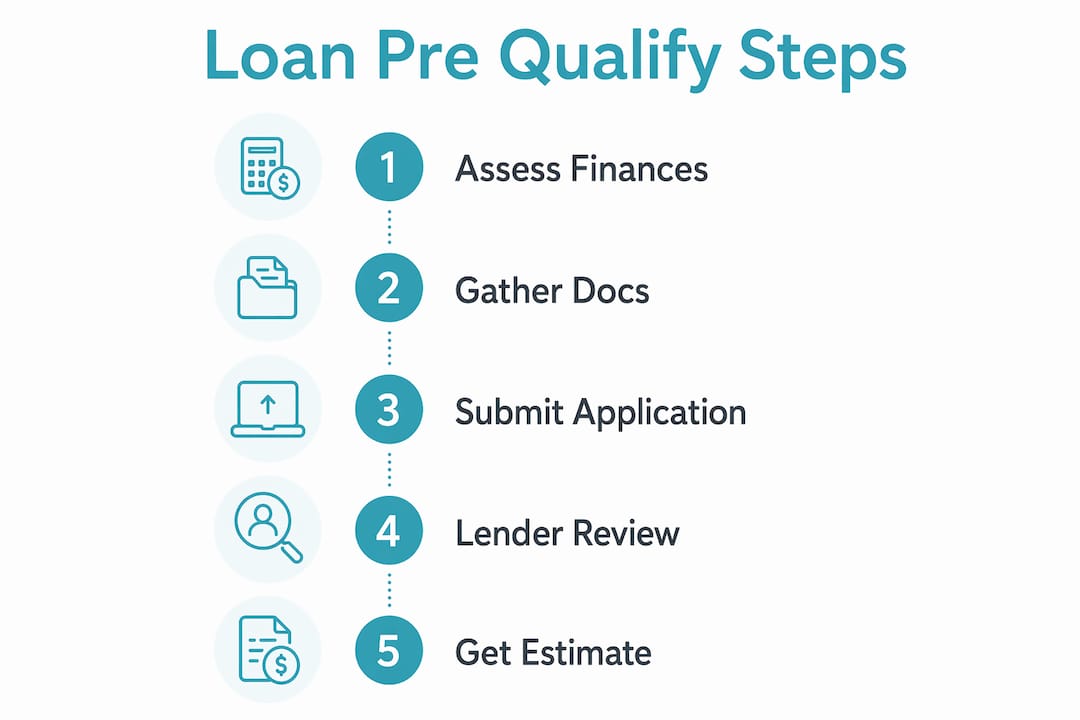

What is the home loan pre qualification application process in NZ?

The application process for a home loan eligibility check in New Zealand follows a clear sequence. Knowing each step helps you manage expectations and avoid unnecessary delays.

- Gather your documents. Compile your ID, payslips, bank statements, deposit evidence, and liabilities list before you begin. A complete application moves faster.

- Choose your approach. You can apply directly through a bank or use a mortgage adviser. Mortgage advisers can match your profile to the most suitable lender before any credit check is run, which protects your credit score.

- Submit your application. Provide your financial details either online, in person, or through your adviser. Be thorough and honest at every point.

- Respond to lender queries promptly. Lenders often request additional documents or clarification. Delays in responding extend your processing time significantly.

- Receive your conditional estimate. The lender issues a pre qualification result, outlining your estimated borrowing capacity and any conditions attached.

- Progress to pre approval. Once you are satisfied with your estimate, submit your full verified documents for formal pre approval before making offers.

Standard pre approval in NZ takes 2–8 working days, though complex applications or self-employed buyers may take 1–2 weeks. Once issued, your pre approval is valid for 60–90 days. If your financial situation remains stable, renewal is generally straightforward.

A mortgage adviser acts as your guide through this process. They know which lenders are most likely to approve your profile and can submit applications that are structured to succeed. For buyers with complex situations, such as variable income or a low deposit, this expertise is genuinely valuable.

Why do home loan pre qualification applications get declined?

A declined pre qualification is not the end of the road. Understanding why lenders say no is the first step to fixing the issue.

Banks assess income stability, debts, deposits, and spending patterns closely, and self-employed applicants face additional scrutiny. The most common reasons for decline include:

- High existing debt. A debt-to-income ratio that exceeds lender thresholds signals financial stress. Credit card limits count against you even if you never use them.

- Unstable or insufficient income. Recent job changes, gaps in employment, or income that varies significantly month to month all raise lender concerns.

- Irregular spending patterns. Unarranged overdrafts, frequent gambling transactions, or large unexplained withdrawals in your bank statements reduce lender confidence.

- Incomplete or inaccurate documentation. Missing payslips, undisclosed debts, or inconsistencies between declared income and bank statements can result in an immediate decline.

- Low deposit or LVR restrictions. Deposits below 20% attract stricter lending criteria. Low deposit loans require stricter income caps and may incur higher interest rates to offset lender risk.

- Poor credit history. Missed payments, defaults, or multiple credit applications in a short period all damage your credit profile.

Pro Tip: Pull a copy of your credit report from a provider like Centrix or Equifax NZ before you apply. Knowing what lenders will see gives you the chance to address any issues first.

Pre approval is conditional and can be withdrawn if your financial situation changes between application and settlement. Avoid taking on new debt, changing jobs, or making large purchases after your pre approval is issued.

How to strengthen your home loan pre qualification application

A strong application is built over months, not days. The buyers who succeed in competitive NZ markets are the ones who prepare well before they ever contact a lender.

Practical steps to improve your position include:

- Review your bank statements for 3–6 months before applying. Lenders read your statements like a financial diary. Reduce discretionary spending, close unused credit cards, and avoid unarranged overdrafts.

- Pay down high-interest debts. Reducing your total liabilities improves your debt-to-income ratio and increases the amount a lender is willing to offer you.

- Maintain steady employment. Lenders favour applicants with at least 3–6 months in their current role. If you are considering a job change, time it carefully relative to your application.

- Build your deposit consistently. A genuine savings history, shown through regular transfers to a savings account, demonstrates financial discipline to lenders.

- Use a mortgage adviser to match your profile. Mortgage advisers help match applicants to lenders before credit checks are run, improving success rates without exposing your credit score to multiple hard enquiries.

- Prepare a complete digital document folder. A well-organised submission reduces back-and-forth with lenders and speeds up the process considerably.

Getting pre approval early builds real confidence when you are ready to make offers. Sellers take pre approved buyers seriously, and in a competitive market, that can be the difference between securing a property and missing out. For a full preparation checklist, the NZ home loan preparation guide from Mortgagemanagers is a practical starting point.

For buyers with more complex financial situations, specialist lenders exist who assess applications differently from the major banks. A mortgage adviser familiar with the NZ market, including options available through providers like Prosper Home Loans, can help identify the right fit for your circumstances.

Key takeaways

Home loan pre qualification is the essential first step for any NZ buyer, and completing it correctly, with accurate documents and a stable financial profile, directly determines the strength of your subsequent pre approval.

| Point | Details |

|---|---|

| Pre qualification vs pre approval | Pre qualification is an unverified estimate; pre approval is a conditional commitment backed by a credit check. |

| Document readiness | Prepare photo ID, 3–6 months of bank statements, payslips, deposit evidence, and a full liabilities list before applying. |

| Processing timelines | Standard pre approval takes 2–8 working days; self-employed applications may take 1–2 weeks. |

| Validity period | Pre approval is valid for 60–90 days; renew promptly if your search extends beyond that window. |

| Strengthen your application | Reduce debts, stabilise income, and use a mortgage adviser to match your profile to the right lender. |

My honest view on pre qualification in the NZ market

The biggest mistake I see buyers make is treating pre qualification as a formality. They rush through it, underestimate what lenders actually scrutinise, and then feel blindsided when their pre approval comes back lower than expected or gets declined entirely.

Pre qualification is your chance to see your finances through a lender’s eyes before it counts. The buyers who use it well spend 2–3 months tidying up their financial picture first. They close unused credit cards, build a clean savings pattern, and get their documents in order. By the time they submit a formal application, there are no surprises.

Working with a mortgage adviser at this stage is not a luxury. It is a practical advantage. Advisers know which lenders are currently most flexible on certain criteria, and they can position your application to succeed without burning your credit score on multiple hard enquiries. That insider knowledge is genuinely hard to replicate on your own.

My advice is simple. Start earlier than you think you need to, be completely honest about your financial position, and get professional guidance if anything in your situation is less than straightforward. The NZ property market rewards prepared buyers.

— Stuart

How Mortgagemanagers can guide your pre qualification

Mortgagemanagers is a locally owned Auckland advisory firm that helps buyers across New Zealand navigate the pre qualification and pre approval process with clarity and confidence.

The team at Mortgagemanagers works with a wide panel of lenders, which means they can access home loan options that banks cannot always offer directly. Whether you are a first home buyer, self-employed, or working with a low deposit, Mortgagemanagers matches your financial profile to the lender most likely to say yes. Their advisers handle the paperwork, manage lender communication, and keep your application moving. To get started, speak with a personal mortgage adviser who understands the NZ market and your individual situation.

FAQ

What is home loan pre qualification in New Zealand?

Home loan pre qualification is a preliminary estimate of your borrowing capacity based on self-reported financial information. It does not require a credit check and gives you a starting point for your property budget.

How long does pre approval take in NZ?

Standard pre approval takes 2–8 working days, with complex or self-employed applications taking up to 1–2 weeks depending on documentation completeness.

How long is a pre approval valid for?

Pre approval is typically valid for 60–90 days in New Zealand. Renewal is possible if your financial circumstances have not changed significantly.

Does pre qualification affect my credit score?

Pre qualification generally does not require a credit check, so it does not affect your credit score. Pre approval does involve a credit check, which creates a hard enquiry on your credit file.

What deposit do I need to pre qualify for a home loan in NZ?

Most NZ lenders prefer a 20% deposit, though some products accept deposits as low as 5–10% with income restrictions and potentially higher interest rates.