TL;DR:

- A mortgage statement summarizes your current home loan status, including balance, interest rate, and recent transactions.

- It helps borrowers track progress, spot errors, and plan refinancing by reviewing components like the balance, payments, and transaction history.

A mortgage statement is a formal document from your lender that summarises your home loan’s current status, including your outstanding balance, interest rate, repayment schedule, and recent transaction history. For New Zealand borrowers, understanding mortgage documents like this one is not optional. It is the clearest window you have into whether your loan is tracking as expected. New Zealand’s standard mortgage term runs 25–30 years, and with banks stress-testing new borrowing at rates between 7.5%–8.5%, knowing exactly what your statement says gives you real control over your financial position.

What does an example of mortgage statement look like in New Zealand?

A typical New Zealand mortgage statement follows a consistent structure across most major lenders. It opens with account identification details, then moves through your current loan balance, interest rate, repayment amounts, and a transaction log for the period covered.

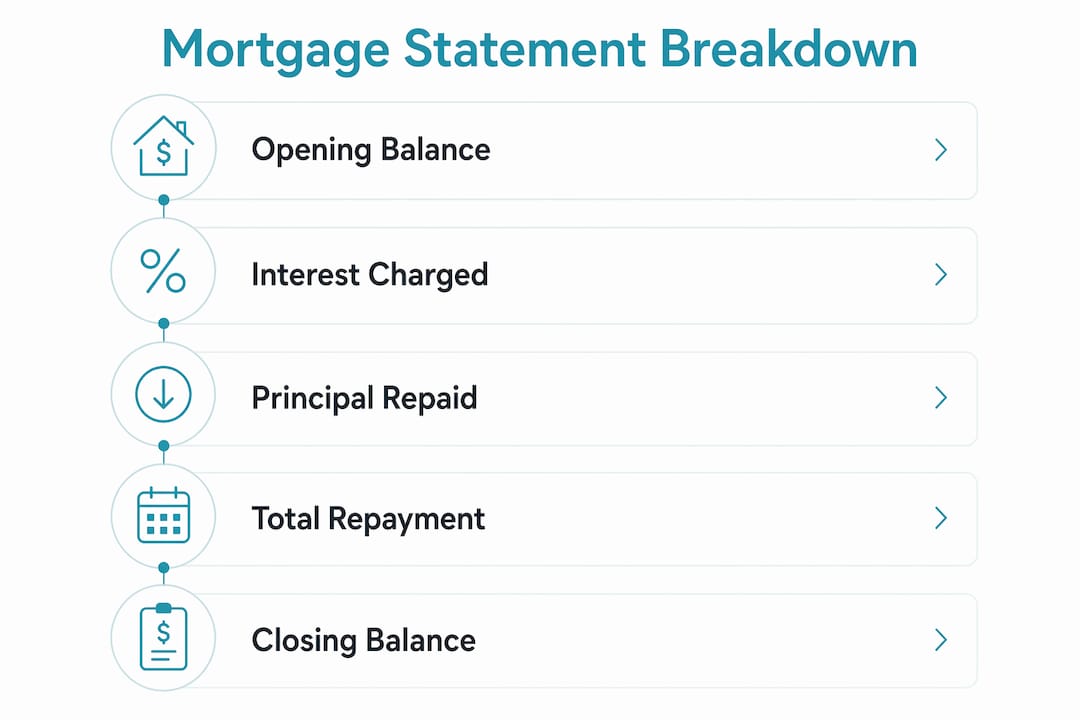

The core components you will find on a standard NZ mortgage statement include:

- Statement number and date: Identifies the period covered and provides a reference for any queries with your lender.

- Opening and closing balance: Shows your loan balance at the start and end of the statement period. The difference reflects principal repaid during that time.

- Current interest rate: Displays whether your loan is on a fixed or floating rate, along with the maturity date for any fixed term.

- Repayment amount and frequency: Shows your scheduled payment, whether weekly, fortnightly, or monthly.

- Transaction history: Lists every debit and credit during the period. Common codes include D/D (direct debit for automatic loan payments), INT (interest charged), and TFR (transfers between accounts).

- Interest charged: The dollar amount of interest applied to your account during the period.

- Principal repaid: The portion of your repayments that actually reduced your loan balance.

- Fees: Any account or administration fees charged by your lender.

NZ bank statements show every transaction in and out of your account for a specific period, and most NZ banks provide statements monthly via your banking app or as a downloadable PDF. That accessibility means you have no excuse for not reviewing yours regularly.

A practical mortgage statement example might show an opening balance of $680,000, with $3,200 in interest charged, $996 in principal repaid, and a closing balance of $679,004. The transaction log would list each direct debit with its date, the INT entry for interest, and any fees applied.

Pro Tip: If you see a transaction code you do not recognise on your statement, contact your lender immediately. Unexpected fees or unrecognised entries can signal an error or, in rare cases, a processing issue that compounds over time.

How to read the repayment breakdown on your mortgage statement

The repayment breakdown is the section that confuses most borrowers. Your total repayment amount stays the same every period, but the split between interest and principal changes constantly.

New Zealand table loans are the most common structure, and they work on a fixed repayment with a dynamic internal split. As you pay down the principal, the interest component decreases, and more of your fixed repayment goes toward reducing the balance. This is the defining feature of a table loan, and it explains why your balance seems to drop slowly at first.

Here is how that plays out in practice:

- Month one, high interest share. On a $700,000 loan at 6.00% over 30 years, the monthly repayment is roughly $4,196. In that first month, around $3,500 is interest and only $696 reduces the principal. The balance barely moves.

- Year five, gradual shift begins. By year five, you have paid down a meaningful portion of principal. The interest charged each month is slightly lower, so a larger share of that same $4,196 repayment reduces the balance.

- Year twenty, the split flips. By year 20, the majority of each repayment goes toward principal. The interest component has shrunk significantly because the outstanding balance is much lower.

- Final years, mostly principal. In the last few years of a 30-year loan, nearly all of each repayment is pure principal reduction. The interest cost is minimal.

- Fixed term versus loan term. Your fixed rate period (typically 6 months to 5 years) is not the same as your loan term. Many borrowers panic when their fixed term expires, not realising they simply need to refix or switch to floating. The 30-year loan continues regardless.

Understanding this progression is what separates borrowers who feel anxious about their mortgage from those who feel confident. The slow early reduction of your balance is not a problem. It is exactly how a table loan is designed to work.

Pro Tip: Use your statement’s closing balance each year as a benchmark. Compare it to the previous year’s closing balance to see your actual annual principal reduction. That number will grow each year, which is reassuring to track.

How to use your mortgage statement for refinancing and financial planning

Your mortgage statement is more than a record. It is a planning tool. Reviewed carefully, it tells you whether you are on track, whether your loan structure still suits your situation, and whether you are ready to approach a lender for refinancing.

When preparing for refinancing, keep these points in mind:

- Gather 3–6 months of statements. Lenders require transaction history across all related accounts, not just your mortgage account. They look for account conduct indicators such as missed payments, overdraft usage, or high-frequency buy-now-pay-later activity, all of which can trigger automatic declines during affordability assessments.

- Check for unauthorised fees. Review each statement period for fees you did not expect. A small recurring fee that appears without explanation can add up significantly over a year.

- Assess your LVR position. Your closing balance divided by your property’s current value gives you your loan-to-value ratio (LVR). Owner-occupiers generally need a 20% deposit to avoid restricted LVR lending. If your LVR has improved, you may qualify for better rates.

- Plan extra repayments. Your statement shows exactly how much principal you are reducing each period. If you can increase that amount, even slightly, the compounding effect over 25–30 years is substantial. Some lenders allow you to pay your home loan off faster by making lump-sum payments against the principal.

- Consider an offset mortgage. If your lender offers an offset facility, linking your savings account reduces the principal on which interest is calculated. Your statement will reflect this as a lower interest charge each period.

- Document everything before meeting an adviser. Bring at least three months of mortgage statements, plus statements for any other accounts, to any meeting with a mortgage adviser. The more complete your picture, the faster and more accurately an adviser can assess your options.

Reviewing your statement every month takes less than ten minutes. That habit builds the financial awareness that makes refinancing conversations much more productive.

Common questions when reviewing your mortgage statement

Several terms and figures on a mortgage statement regularly cause confusion. Knowing what they mean removes the anxiety and puts you in control.

| Term | What it means |

|---|---|

| Loan term | The full repayment period, typically 25–30 years in New Zealand. This is not the same as your fixed rate period. |

| Fixed rate period | The time your interest rate is locked in, usually 6 months to 5 years. When it expires, you refix or move to a floating rate. |

| Principal | The amount you originally borrowed, reduced by each repayment’s principal component. |

| Interest | The cost of borrowing, expressed as a percentage per year and charged on the outstanding principal balance. |

| LVR | Loan-to-value ratio. Your loan balance as a percentage of the property’s value. A lower LVR generally means better lending terms. |

| Stress-test rate | The rate lenders use to assess whether you could afford repayments if rates rise. As of 2026, NZ banks typically apply stress-test rates of 7.5%–8.5%. |

A few other clarifications worth noting:

- Why does my repayment amount stay the same? Because table loans are structured that way. The total repayment is fixed; only the internal split between interest and principal changes as the balance reduces.

- Why does my balance drop so slowly at first? On a large loan at a moderate interest rate, the interest component in early repayments is substantial. This is normal and expected, not a sign that something is wrong.

- What are government charges on my statement? Some statements include government charges such as registration fees or duties applied at settlement. These appear as one-off entries, not recurring charges.

Understanding these terms means you can read any mortgage statement breakdown with confidence, rather than guessing at what the numbers mean.

Key takeaways

A mortgage statement is your most reliable tool for tracking loan progress, spotting errors, and preparing for refinancing decisions in New Zealand.

| Point | Details |

|---|---|

| Statement components | Every NZ mortgage statement includes your balance, interest rate, repayment schedule, and a coded transaction history. |

| Table loan split | Repayments stay fixed, but the interest-to-principal split shifts over time as your balance reduces. |

| Loan term vs fixed term | Your 25–30 year loan term and your fixed rate period (6 months to 5 years) are entirely different things. |

| Refinancing preparation | Lenders need 3–6 months of transaction history across all accounts, not just your mortgage, to assess refinancing suitability. |

| Regular review habit | Checking your statement monthly helps you spot fees, track LVR improvements, and plan extra repayments effectively. |

What I have learned from years of reading mortgage statements with clients

The most common mistake I see is borrowers assuming their loan is not working because the balance barely moves in the first few years. They look at their statement after 12 months of repayments and feel disheartened. What they are actually seeing is the table loan structure doing exactly what it is designed to do. The interest is front-loaded because the balance is at its highest. That is not a flaw. It is maths.

The second mistake is confusing the fixed rate period with the loan term. I have sat with clients who genuinely believed their mortgage was ending when their two-year fixed rate expired. Fixed rate periods explained clearly show that refixing is simply choosing a new rate for the next period. The 30-year loan continues underneath, unchanged.

The third mistake is ignoring fees. A $10 monthly account fee sounds trivial. Over 30 years, it adds up to $3,600, and that is before you account for the interest you could have saved by applying that money to principal instead. Your statement shows every fee. Read it.

My honest advice is to treat your mortgage statement like a quarterly health check. You do not need to obsess over it, but you do need to understand it. Borrowers who engage with their statements regularly make better refinancing decisions, catch errors earlier, and generally feel far less anxious about their mortgage. That confidence is worth a lot.

— Stuart

How Mortgagemanagers can help you make sense of your mortgage

Reading a mortgage statement becomes much easier when you have an expert beside you. Mortgagemanagers is a locally owned Auckland-based team of mortgage advisers who work with New Zealand borrowers across Auckland, the North Shore, West Auckland, and remotely throughout the country.

Whether you are reviewing your first statement, preparing for refinancing, or trying to understand why your balance is moving the way it is, the team at Mortgagemanagers can walk you through it clearly. They interpret the numbers, explain your options, and help you make decisions that suit your actual financial situation. Reach out to Mortgagemanagers for a conversation that cuts through the confusion and gives you a clear picture of where your loan stands.

FAQ

What is a mortgage statement?

A mortgage statement is a document from your lender that shows your current loan balance, interest rate, repayment schedule, and recent transaction history for a set period.

What does a sample mortgage bill typically include?

A sample mortgage bill includes your opening and closing balance, interest charged, principal repaid, repayment amount, transaction codes such as D/D and INT, and any fees applied during the period.

Why does my loan balance reduce so slowly at first?

Table loans in New Zealand front-load the interest component, so early repayments cover mostly interest. As the balance reduces, more of each fixed repayment goes toward principal.

What is the difference between my loan term and my fixed rate period?

Your loan term is the full repayment period, typically 25–30 years. Your fixed rate period is the shorter window, usually 6 months to 5 years, during which your interest rate is locked in.

How many months of statements do I need for a refinancing application?

Lenders typically require 3–6 months of transaction history across all related accounts to assess your account conduct and confirm your suitability for refinancing.