They say that over 60 percent of home buyers admit they feel stressed about understanding mortgage repayments, and few (if any) really know how to calculate mortgage repayments.

Choosing the right mortgage and accurately calculating repayments can shape your financial security for years to come so it’s important.

With every interest rate change and loan option, the stakes only grow higher. You can either stand still or really make some headway in paying your mortgage off faster while the interest rates are lower. By learning what steps to follow and what details matter most, you can take control of your mortgage and avoid costly surprises later on.

Table of Contents

- Step 1: Gather Key Mortgage Information

- Step 2: Select The Appropriate Repayment Structure

- Step 3: Apply Current Interest Rates

- Step 4: Calculate Regular Repayment Amounts

- Step 5: Check And Verify Repayment Results

Quick Summary

| Key Insight | Explanation |

|---|---|

| 1. Gather key mortgage details | Collect total loan amount, interest rates, loan term, and repayment frequency for accuracy. |

| 2. Choose repayment structure wisely | Decide between fixed and floating rates based on financial stability and risk tolerance. |

| 3. Research current interest rates | Gather quotes from multiple lenders and evaluate total costs, not just the lowest interest rates. |

| 4. Calculate regular repayments clearly | Use gathered information to determine monthly payments and explore different repayment frequencies. |

| 5. Verify your calculations thoroughly | Cross-check calculations using multiple methods for accuracy and reliable budgeting. |

Step 1: Gather key mortgage information

Calculating mortgage repayments requires collecting precise financial details that will form the foundation of your loan assessment. Understanding key mortgage information enables you to create an accurate financial roadmap for your home ownership journey.

Start by compiling critical financial documentation and specifics about your potential mortgage. You will need to gather specific information such as the total loan amount you are seeking, current interest rates offered by financial institutions, the proposed loan term (typically ranging from 15 to 30 years in New Zealand), and your preferred repayment frequency (weekly, fortnightly, or monthly). Each of these components plays a significant role in determining your exact mortgage repayments.

Pro Tip: Request an updated copy of your credit report before beginning the mortgage calculation process. A clean credit history can help you secure more favourable interest rates, which directly impacts your potential repayment amounts. Accurate and comprehensive financial information will provide the most reliable mortgage repayment estimates, helping you make informed decisions about your home financing strategy.

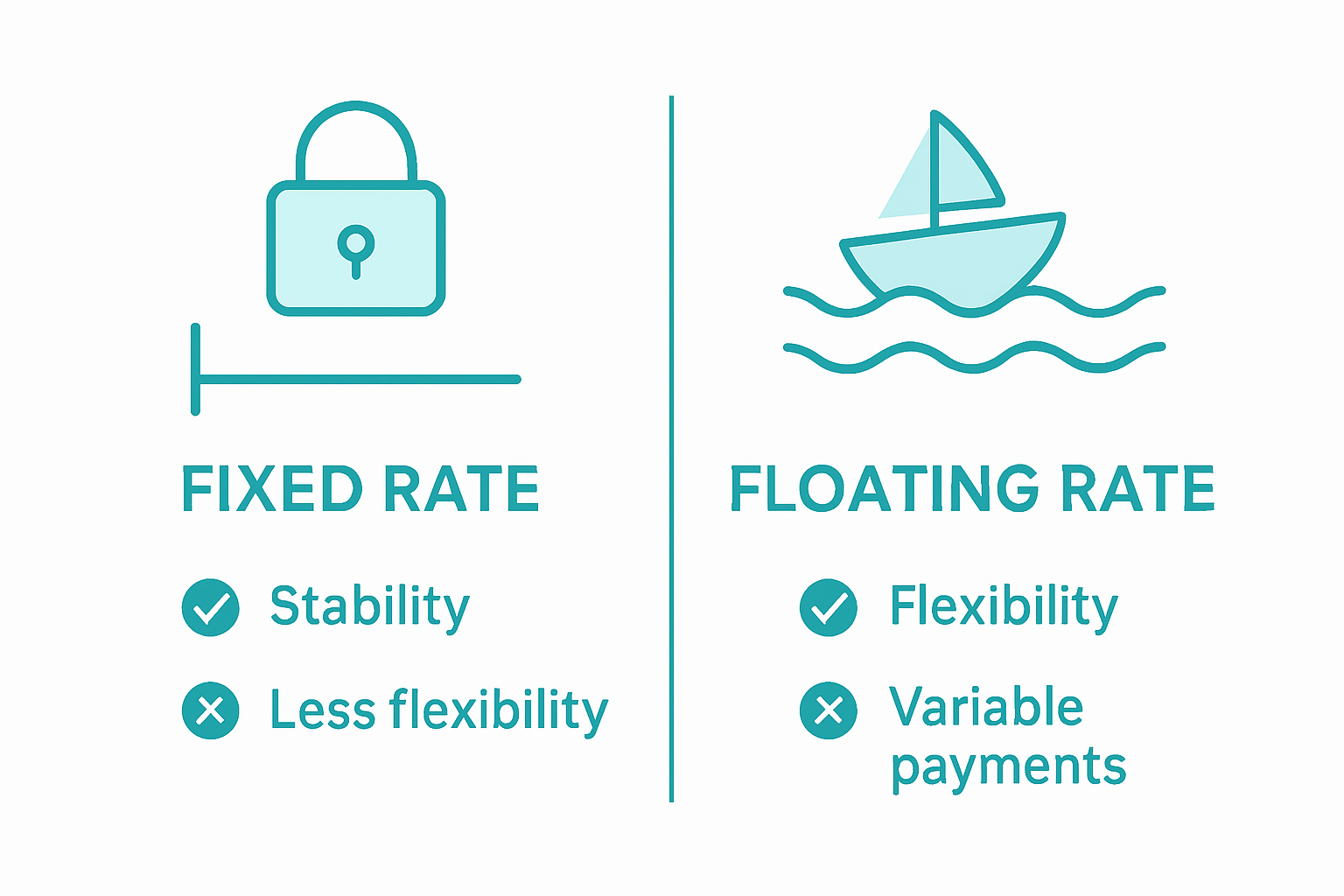

Step 2: Select the appropriate repayment structure

Selecting the right mortgage repayment structure is crucial in managing your financial strategy and long-term home loan commitments.

Choosing between fixed and floating interest rates will significantly impact your financial planning and monthly budgeting.

In New Zealand, you typically have two primary repayment structure options:

Fixed rate loans provide stability with consistent repayment amounts over a predetermined period, usually between one to five years. This option allows you to budget precisely, knowing exactly what you will pay each month.

Floating rate loans, conversely, fluctuate with market conditions, offering more flexibility but potentially introducing financial uncertainty.

Pro Tip: Consider your personal financial situation and risk tolerance when selecting a repayment structure. If you prefer predictability and steady financial planning, a fixed rate might suit you best. If you anticipate potential income increases or want the ability to make additional repayments without penalties, a floating rate could provide more financial adaptability. Remember that some lenders also offer split loan options, allowing you to divide your mortgage between fixed and floating rates for balanced financial management.

Step 3: Apply current interest rates

Applying current interest rates is a critical step in calculating your mortgage repayments accurately. Navigating home loan interest rates requires careful research and comparison across multiple financial institutions in New Zealand.

To effectively apply current interest rates, start by gathering quotes from various banks and lending institutions. Look beyond the headline rate and consider factors such as comparison rates, additional fees, and potential flexibility in repayment terms. Different lenders offer varying rates based on your credit history, loan amount, deposit size, and overall financial profile. Some institutions might provide more competitive rates for first home buyers or those with substantial deposits.

Pro Tip: Do not solely focus on the lowest interest rate. Consider the total cost of the loan, including establishment fees, ongoing charges, and potential break costs. Request a comprehensive breakdown of all expenses from potential lenders to make an informed decision. Some mortgage advisers can help you navigate these complex comparisons, potentially saving you significant money over the life of your home loan.

Step 4: Calculate regular repayment amounts

Calculating your regular mortgage repayments is a crucial step in understanding your financial commitment and long-term budget planning. Mortgage repayments require careful consideration of multiple financial factors that will impact your monthly obligations.

To calculate your regular repayment amounts, you will need to use a combination of key information gathered in previous steps. Then use our mortgage calculator (above) to see what your repayments would be and then you can look at the options if you increased the repayments even just a little.

This calculation provides a basic framework for understanding your potential financial commitment.

Pro Tip: Consider exploring different repayment frequencies to optimise your loan paydown strategy. While monthly payments are standard, switching to fortnightly repayments can potentially reduce your overall interest payments and shorten your loan term. Some borrowers find that aligning their repayments with their pay cycle can create more manageable cash flow and help them make additional contributions towards their principal balance.

Pro Tip (2): Consider rounding up your repayment and look at the savings that you can make, and how much earlier you will have the mortgage paid off by. Imagine how much better it would be to have the mortgage paid off a few years earlier – it would certainly make life much easier. Remember that each extra dollar goes directly to paying off the principal and that then reduces the future interest cost.

Step 5: Check and verify repayment results

Verifying your mortgage repayment calculations is a critical step to ensure financial accuracy and prevent potential budgeting mistakes. Understanding mortgage verification techniques will help you confirm the reliability of your financial projections.

To thoroughly check your repayment results, use our online mortgage calculator. You can also have your numbers cross referenced with a professional mortgage adviser. Discuss with the adviser how different variables like interest rates, loan terms, and repayment frequencies might impact your total repayment amount.

Pro Tip: Listen to your advisers opinions, question any assumptions, the calculation methodology, and remember that over time interest rates will change. This approach not only helps you validate your current calculations and also provides a valuable reference point for future financial planning and potential refinancing decisions.

Take Control of Your Mortgage Repayments with Expert Guidance

Calculating mortgage repayments in New Zealand can feel overwhelming with so many variables like interest rates, loan terms and repayment structures to consider. If you want to avoid costly mistakes and gain confidence in your financial planning, connecting with local experts is the key. This article lays out important steps but partnering with Mortgage Managers in Hobsonville provides personalised advice tailored to your unique situation.

Take the stress out of managing your home loan journey by speaking to Auckland mortgage advisers who understand how to optimise your repayments and help you find competitive rates. Discover how our team can support you with expert mortgage advice that aligns with your goals. Act now to secure a smarter financial future – start your conversation at Mortgage Managers and explore How to Calculate a Mortgage with professional support every step of the way.

Frequently Asked Questions

What key information do I need to calculate mortgage repayments in New Zealand?

To calculate mortgage repayments, gather details such as the total loan amount, current interest rates, loan term, and preferred repayment frequency. Start by collecting this information to create an accurate financial roadmap for your mortgage assessment.

How do I choose between fixed and floating mortgage interest rates?

Select fixed rates for stable repayment amounts and predictability, or opt for floating rates for flexibility and potential savings if interest rates decrease. Assess your financial situation and risk tolerance to make a decision that aligns with your budgeting needs.

How can I effectively apply current interest rates to my mortgage repayment calculations?

Gather quotes from various lenders and consider not just the headline rate but also fees and terms. Compare these details to determine the best overall loan cost and provide an accurate basis for your repayment calculations.

What is the process for calculating my regular mortgage repayment amounts?

To calculate regular repayments, multiply the loan amount by the interest rate and divide by the number of payments per year. For example, a $400,000 loan at an interest rate of 5.5% paid monthly will require careful calculations to determine your monthly obligations. But you can use our mortgage calculator which is online and free.

How can I verify my mortgage repayment calculations?

Verify your calculations by cross-referencing with multiple verification methods such as online calculators and mortgage adviser estimates. This double-checking process helps ensure accuracy and guards against potential budgeting mistakes.

What should I include in a spreadsheet to track my mortgage calculations?

Create a comprehensive spreadsheet that tracks your mortgage calculations, initial assumptions, and any variations in scenarios. Highlight key figures like loan amount, interest rates, and verification sources to provide a valuable reference for future financial planning.

Other Recommended Reading

As you will now know, it’s important that you know how to calculate mortgage repayments BUT it’s also important to know how the various bank home loans differ and which are the best home loans.

- Mortgage Repayments Explained: Complete NZ Guide

- Learn The Importance of Understanding Mortgage Repayments

- Little Changes Save Over $100,000 On Your Mortgage

- Is It True That Fortnightly Repayments Pay My Home Loan Off Faster? – Mortgage Managers