TL;DR:

- There are various house loan options in New Zealand in 2026, including fixed, floating, and split mortgages. The choice depends on income stability, risk tolerance, and flexibility needs, with split loans offering a balance between certainty and adaptability. The Kāinga Ora First Home Loan provides low-deposit access for eligible first-home buyers, but approval still requires thorough financial assessment.

House loans are financial products that let you borrow money to purchase property, with the loan secured against that property until you repay the debt. New Zealand borrowers in 2026 have access to a wider range of home loan structures than ever before, from fixed and floating rate mortgages to government-backed schemes like the Kāinga Ora First Home Loan. Understanding the different types of house loans available to you is the single most important step you can take before approaching a lender. The right structure can save you thousands of dollars and protect your budget through uncertain rate cycles.

What are the different types of house loans in New Zealand?

The three core home loan types in New Zealand are fixed-rate, floating-rate, and split mortgages. Each one suits a different borrower profile, and choosing between them shapes your repayments, your flexibility, and your exposure to interest rate movements.

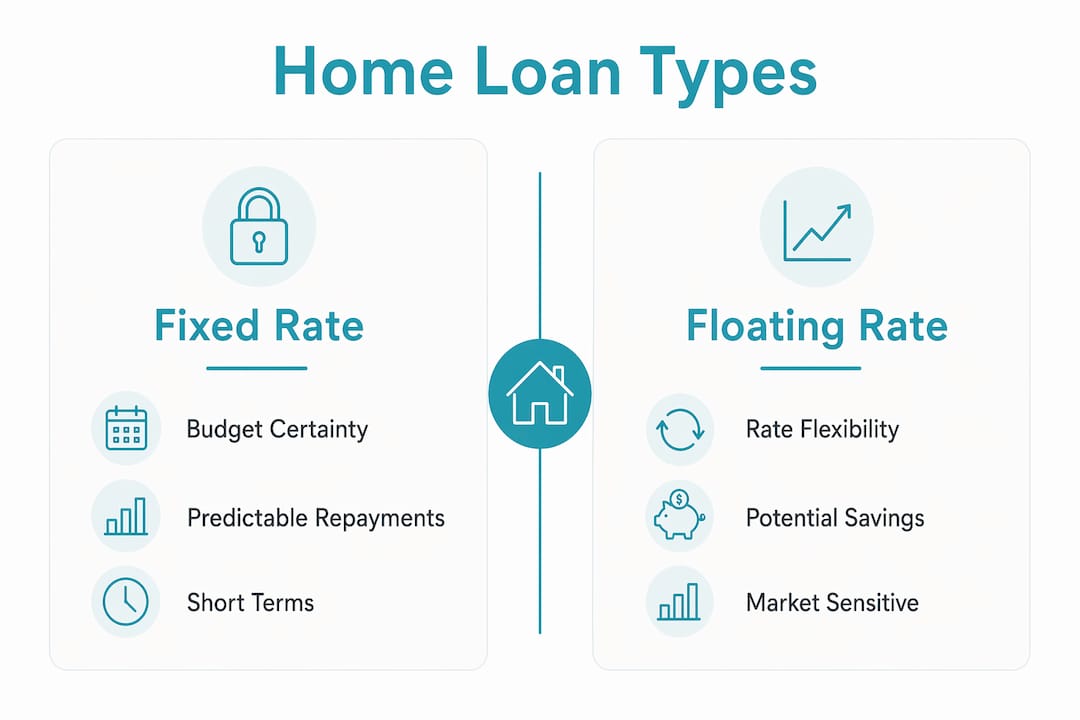

Fixed-rate home loans

A fixed-rate loan locks your interest rate for a set term, typically six months to three years in New Zealand. Your repayments stay the same for the entire fixed period, which makes budgeting straightforward. The trade-off is that you cannot make large lump-sum repayments without paying a break fee, and you cannot switch lenders until the term ends. Fixed rates in 2026 range from 4.49% to 5.39% depending on the term and lender. That spread means the term you choose matters as much as the rate itself.

Floating-rate home loans

A floating rate, also called a variable rate, moves up or down in line with the Reserve Bank of New Zealand’s Official Cash Rate. When the OCR falls, your rate and repayments can drop automatically. When it rises, so does your cost. Floating rates in April 2026 sit between 5.75% and 5.99%, which is higher than most fixed options. That gap reflects a flexibility premium built into the rate, paid in exchange for unlimited penalty-free repayments and the ability to switch lenders at any time.

Split home loans

A split loan divides your mortgage into two or more portions, each with a different rate structure. Split mortgages let you fix part of your debt for certainty while keeping a floating portion for flexibility. This structure reduces your exposure if rates rise sharply, and it lets you make extra repayments on the floating portion without penalty.

Pro Tip: Mortgage advisers commonly recommend keeping 70–80% of your loan on a fixed rate and 20–30% on floating. That split gives you repayment certainty on the bulk of your debt while preserving flexibility for windfalls like bonuses or tax refunds.

| Feature | Fixed rate | Floating rate | Split loan |

|---|---|---|---|

| Rate certainty | Yes, for fixed term | No | Partial |

| Extra repayments | Limited, break fees apply | Unlimited, penalty-free | On floating portion |

| Rate in 2026 | 4.49%–5.39% | 5.75%–5.99% | Blended |

| Best for | Budget-focused borrowers | Flexible income earners | Most borrowers |

How does the Kāinga Ora First Home Loan expand access for buyers?

The Kāinga Ora First Home Loan is a government-backed scheme that lets eligible first-home buyers purchase with a deposit as low as 5%. Kāinga Ora underwrites the lending risk, which means participating banks can approve borrowers who would not qualify under standard low-deposit rules. The scheme removes the need to pay a separate lenders mortgage insurance premium, which is a meaningful saving at settlement.

Eligibility is specific and non-negotiable. Key criteria include:

- Income caps: Single buyers without dependants must earn below $95,000 gross per year. Two or more borrowers, or a single buyer with dependants, must earn below $150,000 combined.

- Property price caps: These vary by region. Auckland sits at $875,000, Wellington at $750,000, and Christchurch at $650,000. Buying even $1 above the cap disqualifies your application.

- Deposit: A minimum 5% deposit is required. This can include personal savings, gifted funds, and a KiwiSaver first-home withdrawal.

- Residency and ownership: You must be a New Zealand citizen or permanent resident and must not currently own any property.

One point many first-home buyers miss: the government guarantee does not replace the bank’s own credit assessment. Lenders still apply their standard serviceability checks, Debt-to-Income ratio limits, and credit reviews. Buy Now Pay Later accounts, car loans, and credit card limits all reduce your borrowing capacity. Clearing short-term debts before applying is one of the most effective ways to strengthen your position.

The First Home Loan differs from a KiwiSaver first-home withdrawal. The withdrawal is a separate mechanism that releases KiwiSaver savings to contribute to your deposit. You can use both together, but they are distinct processes with their own eligibility rules.

For eligible buyers, this scheme is one of the most accessible low-deposit home loan options in New Zealand. Mortgagemanagers works with clients to assess eligibility and prepare applications that meet lender requirements from the outset.

What other specialised home loan types are available in New Zealand?

Beyond fixed, floating, and split loans, New Zealand lenders offer several specialised products that suit specific borrower situations. These are less common but worth understanding before you rule them out.

- Construction loans: These release funds in stages as your build progresses rather than as a lump sum. You pay interest only on the amount drawn down at each stage. Construction loans carry more complexity than standard mortgages, and lenders apply stricter conditions around builder contracts and valuations.

- Bridging loans: A bridging loan covers the gap when you buy a new property before selling your existing one. These are short-term facilities, typically three to six months, and carry higher rates to reflect the added risk. They suit buyers in a strong selling market who need to move quickly.

- Interest-only loans: With an interest-only loan, your repayments cover interest but not principal for a set period, usually one to five years. Monthly payments are lower, but your loan balance does not reduce. Property investors use these to manage cash flow, though owner-occupiers should weigh the long-term cost carefully.

- Revolving credit (flexible) home loans: These work like an overdraft secured against your home. Flexible home loans apply your income directly against your outstanding balance, which reduces the interest charged daily. The catch is that there are no fixed repayments, so they require genuine financial discipline to work effectively.

Pro Tip: Specialised loan types often carry conditions that standard mortgages do not. Before choosing a construction loan or revolving credit facility, ask your mortgage adviser to compare the total interest cost over five years, not just the headline rate.

How do you choose the best home loan type for your situation?

Choosing between types of mortgage loans comes down to four personal factors: income stability, repayment capacity, risk tolerance, and how much flexibility you need day to day.

Work through these questions before you speak to a lender:

- How stable is your income? Salaried employees with predictable pay suit fixed-rate loans. Self-employed borrowers or those with variable income often benefit from a floating or split structure that allows lump-sum repayments when cash flow is strong.

- Do you expect a lump sum in the near future? A bonus, inheritance, or property sale proceeds can reduce your loan significantly. A floating or split structure lets you apply those funds without penalty.

- How would a rate rise affect your budget? If a 1% rate increase would strain your monthly budget, fixing a larger portion of your loan provides a buffer. Loan choice should prioritise your personal tolerance to rate risk over any attempt to predict market movements.

- Are you a first-home buyer with a small deposit? Check your eligibility for the Kāinga Ora First Home Loan before assuming you need a 20% deposit. The 5% deposit threshold opens the market to many buyers who would otherwise need years more saving.

- How long do you plan to hold the property? Short-term holders may prefer floating rates to avoid break fees on exit. Long-term owner-occupiers often benefit from locking in fixed rates during periods of lower rates.

- Have you cleared short-term debts? Buy Now Pay Later accounts and personal loans reduce your borrowing capacity under bank serviceability rules. Addressing these before applying improves your options.

Expert mortgage advisers consistently recommend keeping 20–30% of your loan on a floating rate as a best practice for most borrowers. That structure balances certainty with the ability to make extra repayments as your circumstances change. Your loan structure is not a set-and-forget decision. Reviewing it at each fixed-rate rollover, or when your income or goals shift, keeps your mortgage aligned with your life.

Key takeaways

Choosing the right home loan type requires matching the loan structure to your income stability, risk tolerance, and repayment goals rather than chasing the lowest headline rate.

| Point | Details |

|---|---|

| Fixed vs floating trade-off | Fixed rates offer budget certainty; floating rates offer flexibility at a higher cost in 2026. |

| Split loans suit most borrowers | Keeping 70–80% fixed and 20–30% floating balances certainty with repayment flexibility. |

| Kāinga Ora opens low-deposit access | Eligible first-home buyers can purchase with a 5% deposit and no lenders mortgage insurance premium. |

| Price caps are firm cutoffs | Auckland’s $875,000 cap and regional equivalents strictly determine First Home Loan eligibility. |

| Specialised loans carry hidden costs | Construction, bridging, and interest-only loans require careful comparison of total interest over time. |

What I’ve learned about choosing a home loan in New Zealand’s 2026 market

The most common mistake I see is borrowers choosing a loan structure based on what rates are doing right now rather than what their life looks like over the next three years. Rates will move. Your income, family size, and goals will also move. The loan structure that serves you best is the one that absorbs those changes without forcing you into a corner.

I have seen clients lock 100% of their loan on a fixed rate to chase a low number, only to receive a redundancy payout six months later that they could not apply to the loan without paying a significant break fee. A split structure would have cost them slightly more in interest but saved them far more in lost opportunity.

The Kāinga Ora First Home Loan is genuinely one of the best tools available to eligible buyers, but I caution people not to assume the government backing makes approval automatic. Banks still apply their full credit assessment. Getting your finances in order before you apply, not after, is what separates successful applicants from disappointed ones.

My honest advice: engage a mortgage adviser before you start property hunting, not after you have found a home you love. Knowing your borrowing capacity, your eligible loan types, and your likely rate structure gives you real confidence at the negotiating table. Loan choice is a dynamic process. Treat it that way.

— Stuart

Mortgagemanagers: your guide to the right home loan

Finding the right loan from the many options available takes more than a quick comparison. Mortgagemanagers works as your personal mortgage adviser, assessing your full financial picture and matching you to the loan structure that fits your goals, not just the one that looks good on paper.

Based in Hobsonville and serving clients across Auckland, the North Shore, West Auckland, and remotely throughout New Zealand, Mortgagemanagers helps first-home buyers assess Kāinga Ora First Home Loan eligibility, structure split loans, and prepare applications that meet lender criteria from day one. Whether you are buying your first home or reviewing an existing mortgage, speaking with a qualified mortgage adviser early gives you the clearest path forward.

FAQ

What is the difference between a fixed and floating home loan?

A fixed-rate loan locks your interest rate for a set term, giving you predictable repayments. A floating-rate loan moves with the Reserve Bank of New Zealand’s Official Cash Rate, offering flexibility but at a higher rate in 2026.

How much deposit do I need for a Kāinga Ora First Home Loan?

The Kāinga Ora First Home Loan requires a minimum 5% deposit, which can include personal savings, gifted funds, and a KiwiSaver first-home withdrawal, with no lenders mortgage insurance premium required.

What are the income limits for the Kāinga Ora First Home Loan in 2026?

Single buyers without dependants must earn below $95,000 gross per year. Two or more borrowers, or a single buyer with dependants, must have a combined gross income below $150,000.

What is a split home loan and who does it suit?

A split loan divides your mortgage into fixed and floating portions, balancing repayment certainty with flexibility. It suits most borrowers, particularly those who want to make occasional lump-sum repayments without break fees.

Can I switch my home loan type before my fixed term ends?

Switching from a fixed-rate loan before the term ends typically incurs a break fee, which can be substantial. Floating-rate and revolving credit loans allow switching or extra repayments at any time without penalty.