TL;DR:

- A mortgage is a secured loan used to purchase property, with lenders offering lower interest rates due to security. Most New Zealand loans are fixed-rate table loans with 25–30 year terms, where early repayments save interest, and active management at fixed-term expiry is crucial. Borrowers should understand costs, choose suitable loan types, and work with advisers to optimize their mortgage and avoid costly mistakes.

A mortgage is a secured loan used to buy property, where the property itself acts as security for the lender. Because the lender holds that security, they can offer lower interest rates than unsecured personal loans. Your obligation is to repay both the principal (the amount borrowed) and interest over an agreed term. If repayments stop, lenders can initiate a mortgagee sale to recover the debt. Understanding how does a mortgage work is the foundation of every confident home purchase in New Zealand.

How does a mortgage work in New Zealand?

Most New Zealand home loans are structured as table loans with 25–30 year terms. Your repayment amount stays fixed, but the split between interest and principal shifts over time. In the early years, the bulk of each payment covers interest. As the loan matures, more of each payment chips away at the principal.

This front-loading of interest is not a trick. It reflects the mathematical reality of amortisation. A $600,000 loan at 6% over 25 years means your first repayments are mostly interest, with principal repayment accelerating only in the later years.

Fixed interest rates in New Zealand lock in your rate for terms ranging from 6 months to 10 years, depending on the lender. Floating rates move with the market and offer more flexibility, including the ability to make lump-sum repayments without penalty. Exiting a fixed term early triggers break fees that can reach tens of thousands of dollars, so timing matters.

- Choose your interest rate type. Fixed gives certainty; floating gives flexibility.

- Select your loan term. Shorter terms mean higher repayments but less total interest paid.

- Set your repayment frequency. Weekly or fortnightly repayments reduce interest faster than monthly.

- Understand the amortisation schedule. Ask your lender or adviser for a full breakdown before signing.

Pro Tip: Switching to fortnightly repayments instead of monthly effectively adds one extra monthly payment per year, cutting years off your loan without feeling the pinch.

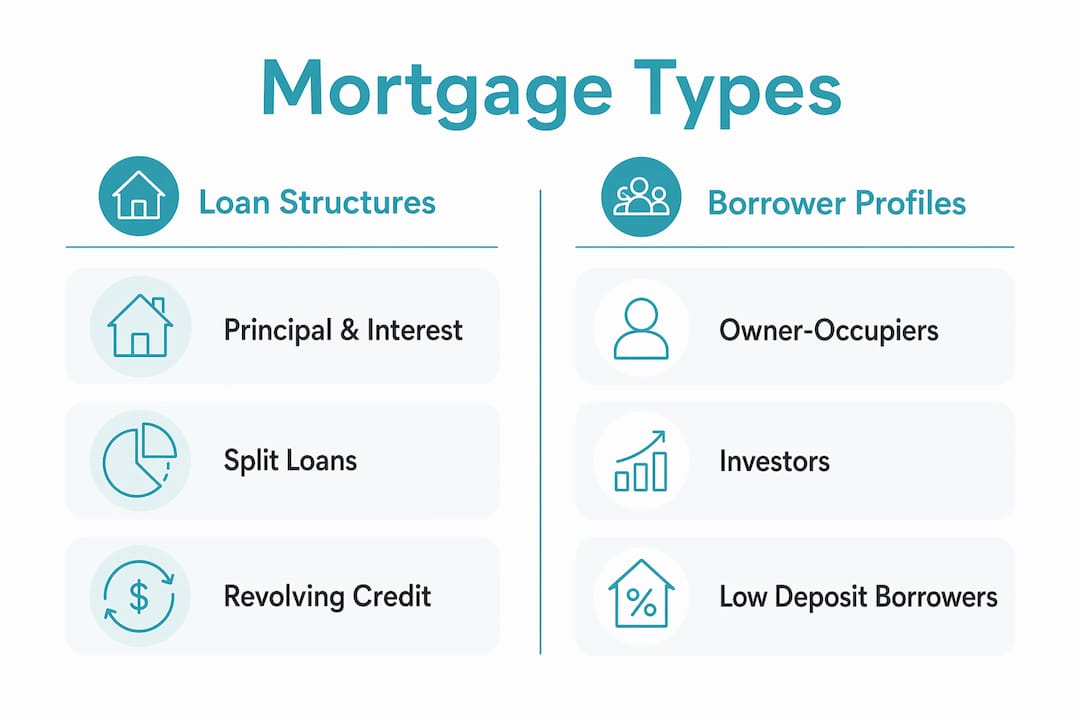

What mortgage types are available in New Zealand?

New Zealand borrowers have several loan structures to choose from, and the right one depends on your income pattern, risk tolerance, and financial goals.

Principal and interest loans are the standard. You repay both the borrowed amount and interest with every payment, so your debt reduces steadily. Interest-only loans require you to pay only the interest for a set period, typically used by investors to manage cash flow. The trade-off is that your principal does not reduce during that period, meaning you pay more interest overall.

Split loans combine fixed and floating portions on the one mortgage. You lock in certainty on part of the loan while keeping flexibility on the rest. This structure is popular with borrowers who want to make extra repayments without triggering break fees on the entire balance.

A revolving credit mortgage works like a large overdraft. Interest is calculated daily on your outstanding balance. When your salary lands in the account, it immediately reduces the balance and cuts the interest charged that day. Disciplined borrowers can save significantly with this structure, but it requires genuine spending discipline.

Your loan-to-value ratio (LVR) also shapes your options. Borrowers with less than 20% deposit typically pay a low equity margin (LEM) of 0.25%–1.00% added to their interest rate. On a large loan, that premium adds thousands of dollars annually.

Pro Tip: If you have a 15% deposit, ask your adviser whether a split loan structure can reduce your LEM exposure while still giving you repayment flexibility.

| Loan type | Best suited to | Key trade-off |

|---|---|---|

| Principal and interest | Owner-occupiers | Steady debt reduction; higher repayments |

| Interest-only | Property investors | Lower short-term payments; no principal reduction |

| Split loan | Borrowers wanting flexibility | Balances certainty and flexibility across portions |

| Revolving credit | High-income, disciplined borrowers | Daily interest savings; requires spending control |

What costs come with a mortgage beyond the deposit?

The deposit is only the beginning. Total upfront buying costs in New Zealand typically range from $8,000 to $15,000, excluding the deposit itself. Knowing these costs in advance prevents nasty surprises on settlement day.

Typical upfront costs include:

- Legal and conveyancing fees: $2,000–$3,500

- Building inspection: $500–$1,200

- LIM report: $200–$400

- Mortgage registration fee: approximately $200

- Valuation (if required): $700–$1,500

Beyond settlement, ongoing costs include home and contents insurance, rates, body corporate levies (for apartments), and general maintenance. These are not mortgage costs directly, but they affect your ability to service the loan comfortably. A full breakdown of buying costs helps you plan your total budget, not just your deposit.

Break fees and discharge fees apply when you exit or restructure a fixed loan early. Break fees are calculated based on the difference between your contracted rate and current wholesale rates, meaning they can be negligible or very large depending on market conditions. Discharge fees are smaller administrative charges, typically a few hundred dollars.

Borrowers with low deposits also face the LEM surcharge on their interest rate. A 0.5% LEM on a $600,000 loan adds $3,000 per year to your interest bill. That cost disappears once your equity crosses 20%, so tracking your LVR over time pays off.

Some lenders charge annual account fees or package fees. These are negotiable, particularly when you use a mortgage adviser who can compare offers across multiple lenders.

What are the steps to get a mortgage in New Zealand?

The mortgage application process follows a clear sequence. Understanding each stage reduces stress and helps you move quickly when you find the right property.

- Get pre-approved. Pre-approval confirms how much a lender will lend based on your income, expenses, and credit history. It is conditional, not guaranteed, but gives you a realistic budget before you start bidding.

- Find a property and make an offer. Your offer can be conditional on finance, giving you time to confirm full approval once a specific property is identified.

- Complete the credit and valuation assessment. The lender assesses the property’s value and your full financial position. A registered valuation may be required, particularly for properties with unusual features or low-deposit applications.

- Receive formal approval. Once the lender is satisfied, they issue a formal loan offer. Your solicitor reviews the mortgage documents alongside the sale and purchase agreement.

- Settlement and drawdown. Mortgage funds are released on settlement day after your solicitor confirms all conditions are met. Ownership transfers, and repayments typically begin the following month.

- Manage your loan at rollover. When your fixed term expires, you must actively renegotiate your rate. Loans that roll over without renegotiation default to the bank’s standard floating or generic fixed rate, which is rarely the most competitive option available.

A mortgage adviser helps you navigate each stage, from selecting the right loan structure to managing the paperwork and comparing lender offers. Their role is particularly valuable at rollover, when many borrowers unknowingly accept a higher rate simply because they did not ask.

Key takeaways

A mortgage is a secured loan repaid over 25–30 years through structured payments that cover both interest and principal, with costs, structures, and rates that require active management at every stage.

| Point | Details |

|---|---|

| Mortgages are secured loans | Property security enables lower rates but gives lenders mortgagee sale rights if repayments fail. |

| Table loans dominate in NZ | Fixed repayments over 25–30 years front-load interest, so early extra repayments save the most. |

| LEM adds real cost | Deposits below 20% trigger a 0.25%–1.00% rate premium, adding thousands annually until equity grows. |

| Upfront costs exceed the deposit | Budget $8,000–$15,000 for legal fees, inspections, LIM reports, and registration on top of your deposit. |

| Rollover is a critical moment | Actively renegotiate at fixed term expiry to avoid defaulting to uncompetitive standard bank rates. |

What I have learned from watching borrowers manage mortgages

The single most costly mistake I see New Zealand borrowers make is treating their mortgage as a “set and forget” arrangement. They sign the documents, make the repayments, and then do nothing when the fixed term expires. The bank rolls them onto a standard rate, and they lose hundreds or thousands of dollars a year without realising it.

The second insight that surprises most people is how much early extra repayments matter. Paying an extra $200 per month on a $600,000 loan at 6% over 25 years saves around $57,000 in interest and shortens the loan by roughly 3.5 years. That is not a marginal gain. It is a life-changing financial outcome from a modest behavioural change made early.

Split loans and revolving credit structures are underused by first-home buyers who default to the simplest option. Simplicity has value, but a split loan can give you the certainty of a fixed rate on most of your debt while keeping a floating portion open for extra repayments. That flexibility costs nothing extra if structured well.

My honest view on break fees: do the maths before you refinance. The savings from a lower rate must outweigh the break cost and any new loan fees. Sometimes they do. Often they do not. A good adviser runs those numbers for you before you commit.

— Stuart

Working with Mortgagemanagers to find the right home loan

Choosing the right mortgage structure is one of the most consequential financial decisions you will make. Getting it wrong costs real money over decades.

Mortgagemanagers is a locally owned and operated mortgage advisory business based in Hobsonville, Auckland, with access to lenders across New Zealand. The team works with you to compare loan structures, explain costs, negotiate fees, and manage your mortgage at every rollover. Whether you are buying your first home or refinancing an existing loan, expert mortgage advice means you are never left guessing which option suits your situation. Talk to the team at Mortgagemanagers to get started.

FAQ

What is a mortgage in New Zealand?

A mortgage is a secured loan where the property you buy acts as security for the lender. If repayments stop, the lender has the legal right to sell the property to recover the debt.

How do I calculate my mortgage repayments?

Repayments depend on your loan amount, interest rate, and loan term. Most New Zealand banks and advisers provide online calculators, or your mortgage adviser can model different scenarios for you.

What deposit do I need for a mortgage in New Zealand?

Most lenders require at least 20% deposit to avoid the low equity margin (LEM) surcharge. Some lenders accept lower deposits, but borrowers pay a rate premium of 0.25%–1.00% until equity reaches 20%.

What happens when my fixed rate expires?

If you do not renegotiate, your loan defaults to the bank’s standard floating or generic fixed rate, which is rarely competitive. Actively reviewing your rate at rollover is one of the most effective ways to reduce your mortgage cost.

What are the steps to get a mortgage in New Zealand?

The key steps are: get pre-approved, make an offer on a property, complete the lender’s credit and valuation assessment, receive formal approval, and draw down funds on settlement day. A mortgage adviser guides you through each stage.