TL;DR:

- Getting a home loan in New Zealand requires meeting deposit, income, credit, and debt criteria set by lenders and regulations.

- Pre-approval is essential as it provides a financial snapshot before property viewing, but finances must stay stable until settlement.

Getting a home loan in New Zealand means securing mortgage finance from a bank or lender by proving you can repay the debt and meeting their eligibility criteria. The industry term is a “mortgage,” and understanding how do I get a loan for a house starts with knowing what lenders actually look for. The Reserve Bank of New Zealand sets lending rules that all banks must follow, including loan-to-value ratio (LVR) and debt-to-income (DTI) limits. Government-backed schemes like Kāinga Ora’s First Home Loan open doors for buyers who cannot yet reach a 20% deposit. Pre-approval is the single most important first step you can take before attending a single open home.

What are the requirements to qualify for a home loan in New Zealand?

Qualifying for a mortgage in New Zealand depends on four core factors: your deposit size, income stability, credit history, and existing debt levels. Lenders assess all four together, not in isolation. A strong score in one area can sometimes offset a weakness in another, but you need to meet minimum thresholds across the board.

Deposit requirements

Standard bank lending requires a minimum 20% deposit, which is the LVR limit set by the Reserve Bank of New Zealand. Some low-deposit exceptions exist, but they are capped by regulation. The Kāinga Ora First Home Loan allows eligible first-home buyers to purchase with as little as 5% deposit, making it one of the most accessible entry points into the market.

Income and employment

Banks require consistent income and typically want to see three to six months of clean financial behaviour through bank statements, payslips, or tax returns. PAYE employees generally receive faster processing because their income is straightforward to verify. Self-employed applicants must supply two full years of financial statements, including tax returns and business accounts, before most lenders will consider their application.

Debt-to-income limits

The Reserve Bank of New Zealand caps most owner-occupier borrowing at six times gross annual household income. A household earning $120,000 combined can borrow a maximum of $720,000 before any other serviceability tests apply. That ceiling shapes your property search before you even speak to a lender.

Documents you will need

Gathering paperwork early saves weeks. Most lenders ask for:

- Photo ID (passport or driver’s licence)

- Three to six months of bank statements

- Two to three recent payslips (PAYE) or two years of tax returns (self-employed)

- Evidence of your deposit savings or KiwiSaver balance

- A list of all current debts, credit cards, and liabilities

- Proof of any other income sources (rental, investments)

The Financial Markets Authority advises borrowers to stress-test their own affordability at higher interest rates before applying. Lenders do this anyway, so doing it yourself first removes surprises.

How do credit scores affect your ability to get a mortgage?

Your credit score is the fastest signal a lender uses to judge repayment risk. A high score opens more lenders and better rates. A low score narrows your options and raises your costs.

Credit score thresholds in New Zealand

Major banks generally require credit scores of 500–600 or above for standard mortgage approval. Scores below that threshold push you toward non-bank lenders, which carry higher interest rates and stricter deposit requirements. Non-bank lenders typically require deposits of 20–30% and charge interest rates 1–4% higher than mainstream banks.

Options if your credit is poor

A low credit score does not automatically end your home-buying plans. Non-bank lenders such as Liberty Financial, Resimac, and First Mortgage Trust specialise in mortgages for borrowers with credit issues, with interest rates typically between 6.5% and 9.5% depending on risk profile. The key is knowing which lender suits your exact situation, and that is where a mortgage broker earns their value. Brokers understand lender policies in detail and can place your application with the right institution the first time, which protects your credit score from multiple hard enquiries.

Steps to improve your credit before applying:

- Pay all bills and existing debts on time for at least three months

- Close unused credit cards and reduce credit limits

- Avoid applying for any new credit in the months before your mortgage application

- Check your credit report through Centrix, Equifax, or Illion for errors and dispute any inaccuracies

- Reduce your credit card balances to below 30% of their limits

Pro Tip: A mortgage broker who specialises in bad credit home loans can access non-bank lenders you cannot approach directly, and they submit one application rather than several, keeping your credit score intact.

What home loan options are available for low deposit borrowers?

Low deposit borrowers have more options than most people realise. The key is understanding which scheme fits your income, your savings, and the property you want to buy.

Kāinga Ora First Home Loan

The Kāinga Ora First Home Loan is the most accessible government-backed scheme for New Zealand first-home buyers. Eligible buyers can purchase with a 5% deposit, with income caps set at $95,000 for single buyers and $150,000 for multiple buyers or those with dependants. A Lender’s Mortgage Insurance (LMI) fee of 1.2% applies to the loan amount. That fee is the cost of borrowing with a smaller deposit, and it is typically added to the loan balance rather than paid upfront.

KiwiSaver first home withdrawal

KiwiSaver first home withdrawal lets eligible members withdraw nearly their full balance after three years of membership to boost their deposit. The funds transfer directly to your solicitor on settlement day, and a minimum of $1,000 must remain in the account. For many Kiwi buyers, this withdrawal is the difference between reaching a 5% deposit and falling short.

Comparing your options

| Feature | Standard 20% deposit loan | Kāinga Ora First Home Loan |

|---|---|---|

| Minimum deposit | 20% | 5% |

| LMI fee | None | 1.2% of loan amount |

| Income cap | None | $95,000 single / $150,000 joint |

| Property price cap | None | Regional caps apply |

| Lender type | Any bank | Participating lenders only |

For a full list of low deposit lender options available to Kiwi buyers, Mortgagemanagers maintains an updated guide covering current participating lenders and eligibility rules.

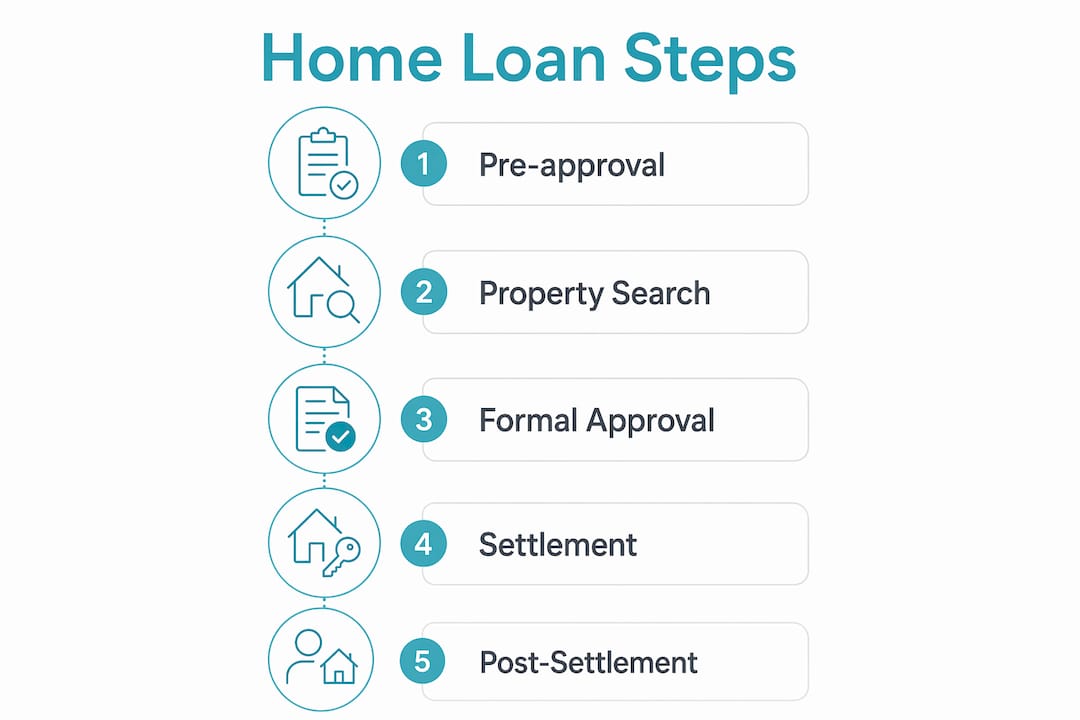

How to apply for a home loan: pre-approval through to settlement

The mortgage application process follows a clear sequence. Understanding each stage removes the anxiety of not knowing what comes next.

Step 1: Get pre-approval

Pre-approval is a conditional offer from a lender based on your current financial position. Mortgage pre-approval typically takes 6–8 working days and remains valid for 60–90 days. Pre-approval is not a loan guarantee. It is a snapshot of your finances at a point in time, and any significant change, such as a new job, a new debt, or a drop in income, can trigger reassessment before formal approval.

Pro Tip: Do not make any major financial changes after receiving pre-approval. Changing jobs, taking on a car loan, or making large purchases can void your conditional offer and restart the process.

Step 2: Formal approval

Once you have found a property and signed a sale and purchase agreement, your lender moves to formal approval. This stage takes 5–10 working days and includes a registered property valuation. The lender confirms the property is worth what you are paying and that it meets their security requirements. Stay within the borrowing limit set during pre-approval to avoid delays.

Step 3: Settlement

Settlement typically occurs 10–30 days after formal approval, depending on the terms agreed in your sale and purchase contract. Your solicitor handles the legal transfer of funds and title. KiwiSaver withdrawals, if applicable, must be requested well in advance because processing takes time. Missing the settlement date carries financial penalties, so keep your solicitor informed at every stage.

The full mortgage approval process from pre-approval to settlement is something Mortgagemanagers walks clients through in detail, so nothing catches you off guard.

Common mistakes and tips to improve your approval chances

Most declined applications share the same avoidable mistakes. Knowing them in advance puts you well ahead of the average applicant.

- Inconsistent savings: Lenders want to see stable savings patterns and no new high-interest debt for at least three months before application. Sporadic deposits and withdrawals raise red flags.

- New debt before applying: Taking on a car loan, a personal loan, or a new credit card in the months before your application reduces your borrowing capacity and signals financial instability.

- Applying to multiple lenders at once: Each application creates a hard enquiry on your credit file. Multiple enquiries in a short period lower your score and make lenders nervous.

- Underestimating your expenses: Lenders examine your actual spending, not just your income. Subscriptions, dining out, and discretionary spending all count against your serviceability.

- Skipping a mortgage broker: A broker accesses multiple lenders, matches your profile to the right product, and submits one clean application. For complex cases, this is not optional; it is the most direct path to approval.

Pro Tip: If your application is declined, ask the lender for the specific reason in writing. Most will provide it, and that information tells you exactly what to fix before you apply again.

The Financial Markets Authority recommends that all borrowers assess their ability to service a loan under rising interest rate scenarios before committing. Lenders do this stress test themselves, and borrowers who do it first arrive at the table with realistic expectations.

Key takeaways

Qualifying for a mortgage in New Zealand requires a minimum 5–20% deposit, stable income, a credit score above 500, and a debt-to-income ratio within Reserve Bank of New Zealand limits.

| Point | Details |

|---|---|

| Deposit minimum | Standard loans need 20%; Kāinga Ora First Home Loan allows 5% for eligible buyers. |

| Credit score matters | Scores below 500–600 push you to non-bank lenders with higher rates and deposits. |

| Pre-approval first | Get pre-approval before property hunting; it is valid for 60–90 days and conditional on stable finances. |

| KiwiSaver boosts deposit | First-home buyers can withdraw nearly their full KiwiSaver balance after three years to fund their deposit. |

| Brokers reduce risk | A mortgage broker submits one application to the right lender, protecting your credit score and saving time. |

What I have learned after years of watching Kiwis buy their first home

The single biggest mistake I see first-home buyers make is treating pre-approval as a finish line. It is actually the starting gun. Your finances need to stay completely stable from the moment you receive that conditional offer until the day you settle. I have watched buyers lose their pre-approval because they bought a new car two weeks before settlement. That is a painful and entirely preventable situation.

The second thing I have noticed is that buyers with complicated situations, whether that is self-employment, a patchy credit history, or a low deposit, often give up too early. They get knocked back by one bank and assume the answer is no across the board. The reality is that the New Zealand lending market has genuine options for these borrowers. Non-bank lenders exist precisely for this reason, and a good mortgage adviser knows exactly which lender suits which borrower.

Government schemes like the Kāinga Ora First Home Loan have genuinely changed what is possible for first-home buyers. A 5% deposit was unthinkable for most buyers a generation ago. The income caps mean it is not for everyone, but for those who qualify, it is a real and practical path into homeownership.

My honest observation on market conditions: interest rates and lending rules shift, but the fundamentals of a strong application never do. Clean finances, consistent savings, and a realistic budget will always get you further than any scheme or product on its own.

— Stuart

How Mortgagemanagers can help you find the right home loan

Mortgagemanagers is a locally owned mortgage advisory business based in Hobsonville, Auckland, with the ability to work with clients remotely across New Zealand. The team specialises in matching borrowers to the right lender, whether you are a first-home buyer with a 5% deposit, a self-employed applicant with two years of financials, or a borrower working through a credit challenge.

Getting mortgage advice before you start looking at properties is the single most effective thing you can do to improve your approval chances. Mortgagemanagers offers a no-cost broker service, meaning the lender pays the adviser fee, not you. Reach out to the team to get a clear picture of what you can borrow, which lenders suit your situation, and what steps to take before your first open home.

FAQ

What is the minimum deposit to get a home loan in New Zealand?

The standard minimum deposit is 20% of the purchase price. Eligible first-home buyers can access the Kāinga Ora First Home Loan with as little as 5% deposit, subject to income and property price caps.

How long does mortgage pre-approval take in New Zealand?

Pre-approval typically takes 6–8 working days and remains valid for 60–90 days. Any significant change to your finances during that period may require reassessment before formal approval is granted.

Can I get a mortgage with bad credit in New Zealand?

Yes. Non-bank lenders such as Liberty Financial, Resimac, and First Mortgage Trust offer mortgages to borrowers with lower credit scores, though deposits of 20–30% and higher interest rates typically apply. A mortgage broker is the most effective way to access these lenders.

What documents do I need to apply for a home loan?

You will need photo ID, three to six months of bank statements, recent payslips or two years of tax returns if self-employed, evidence of your deposit, and a list of all current debts and liabilities.

Does KiwiSaver help with buying a first home?

Yes. After three years of KiwiSaver membership, eligible first-home buyers can withdraw nearly their full balance to contribute toward their deposit. The funds are paid directly to your solicitor on settlement day, with a minimum of $1,000 required to remain in the account.