Most first home buyers in Auckland are surprised to learn that more than 85 percent of mortgages in New Zealand use amortisation schedules very different from common australian loan structures. Understanding how your repayments are split between interest and principal is key to avoiding costly mistakes and building equity in your home from day one. This quick guide breaks down how New Zealand loan payments work so you can make smarter decisions and compare options with confidence.

Table of Contents

- Amortisation Defined In Home Loan Contexts

- Types Of Loan Repayments In New Zealand

- How Amortisation Schedules Shape Payments

- Impact On Total Loan Costs And Equity

- Risks And Common Pitfalls To Avoid

Key Takeaways

| Point | Details |

|---|---|

| Understanding Amortisation | Amortisation entails systematic loan repayment, blending principal and interest, which is crucial for managing long-term home debt. |

| Types of Loan Repayments | Explore various repayment structures such as table loans and offset loans to find options that best accommodate your financial situation. |

| Amortisation Schedules | These schedules define how each payment is allocated, affecting equity build-up and total interest paid; request a detailed schedule from your lender. |

| Avoiding Pitfalls | Be mindful of the complexities of loan terms, including early repayment penalties and variable interest rates, to safeguard your financial health. |

Amortisation Defined In Home Loan Contexts

Amortisation is a fundamental financial concept that lies at the heart of how home loans work in New Zealand. When you take out a mortgage, amortisation describes the systematic process of gradually paying off your loan through regular repayments that cover both principal and interest. Unlike other types of loans where you might only pay interest, home loans are structured to ensure you steadily reduce your total debt over time.

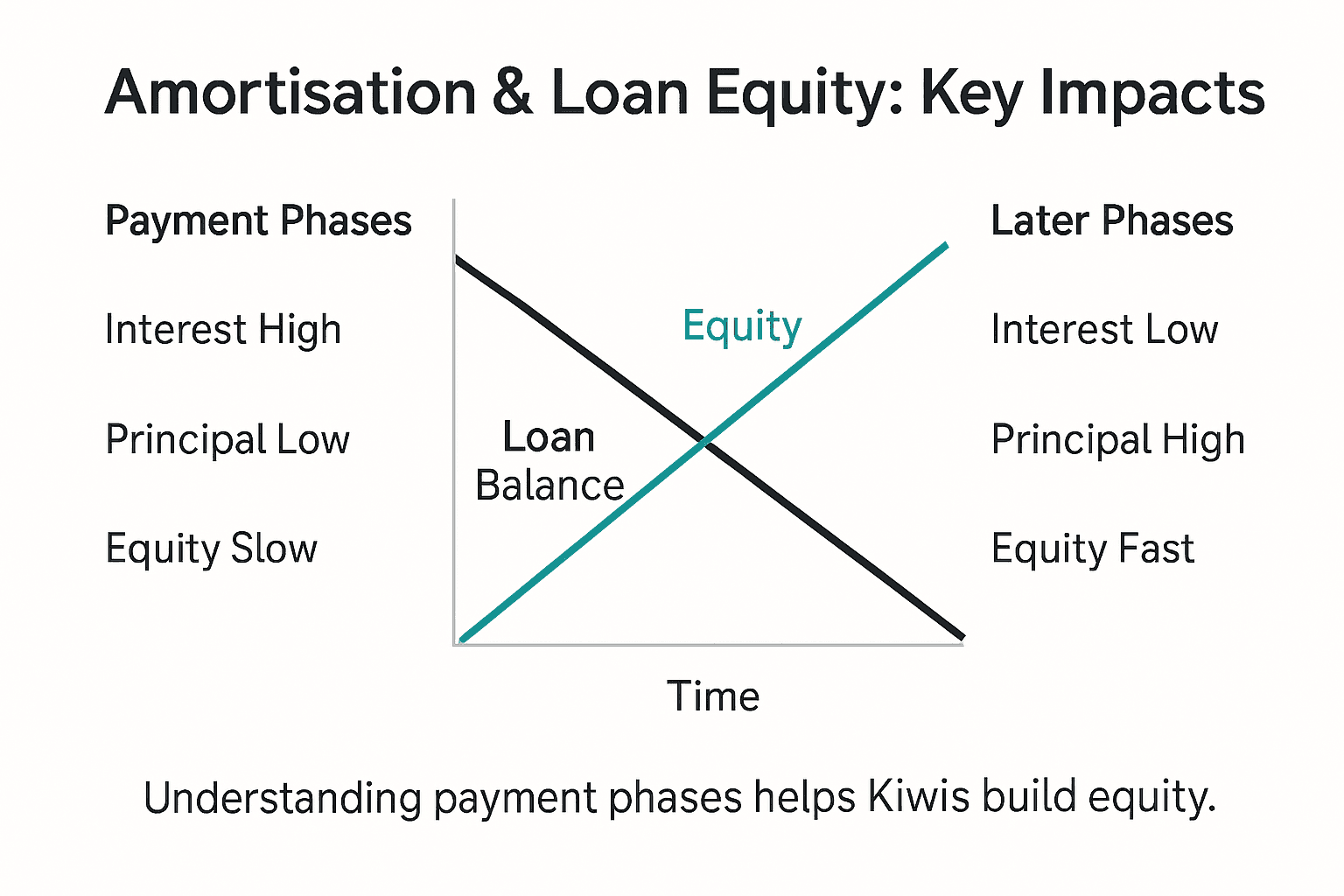

In practical terms, amortisation means that each payment you make is split between two key components: interest and principal. Early in your loan term, a larger portion of your repayment goes towards covering the interest charged by the bank. As lending statistics from the Reserve Bank of New Zealand indicate, this structure significantly impacts how households manage their financial planning and debt reduction strategies. As you continue making payments, the balance gradually shifts so that more of each payment goes towards reducing the principal amount.

Understanding amortisation is crucial for New Zealand homeowners because it helps you visualise how your loan balance decreases over time. Most table loans in New Zealand follow this amortisation model, where your scheduled repayments are calculated to ensure the entire loan is paid off by the end of the loan term. This means that with consistent payments, you’ll steadily build equity in your home while reducing your overall debt.

Pro tip: Consider using an online mortgage calculator to visualise how amortisation impacts your specific loan, helping you understand exactly how much of each payment goes towards principal versus interest.

Types Of Loan Repayments In New Zealand

New Zealand offers several distinct home loan repayment structures, each designed to meet different financial needs and borrowing preferences. Understanding these options is crucial for making informed decisions about your mortgage strategy. According to lending statistics from the Reserve Bank of New Zealand, the most common types of loan repayments include table loans, revolving credit loans, offset loans, reducing loans, and interest-only loans.

Table loans represent the most traditional repayment structure in New Zealand. These loans feature regular, consistent repayments that gradually reduce both principal and interest over the loan term. Revolving credit loans offer more flexibility, functioning similarly to an overdraft where you can deposit and withdraw funds while keeping your overall loan balance manageable. Offset loans provide another innovative approach, allowing you to link your savings account to your mortgage, effectively reducing the interest charged by offsetting your savings against the loan balance.

Interest-only and reducing loans offer alternative approaches for borrowers with specific financial goals. Interest-only loans permit borrowers to pay only the interest for a set period, which can be beneficial for investors or those experiencing temporary financial constraints. Reducing loans, by contrast, are structured to progressively decrease the principal amount more aggressively, potentially helping borrowers reduce their overall interest payments over time.

Here’s a summary comparing popular home loan repayment types in New Zealand and their typical uses:

| Loan Type | Repayment Method | Typical Use Case | Flexibility Level |

|---|---|---|---|

| Table Loan | Fixed regular payments | First-time buyers | Moderate |

| Revolving Credit | Variable, like a large overdraft | Cash flow management | High |

| Offset Loan | Savings offset loan balance | Maximising interest savings | Moderate |

| Interest-Only Loan | Interest payments only | Property investors | Low (temporary period) |

| Reducing Loan | Principal decreases rapidly | Fast debt reduction | Moderate |

Pro tip: Consult with a mortgage adviser to carefully assess which loan repayment structure aligns best with your unique financial circumstances and long-term wealth-building objectives.

How Amortisation Schedules Shape Payments

Amortisation schedules are the financial roadmap that determines exactly how each mortgage payment is applied, revealing the intricate dance between principal and interest throughout your loan’s lifecycle. Using mortgage calculation tools helps borrowers understand their precise payment breakdown, showing how initially, most of your payment goes towards interest rather than reducing the actual loan balance.

The structure of these schedules is particularly fascinating for New Zealand homeowners. In the early years of a typical table loan, a significantly larger proportion of each payment is allocated to interest, with only a small amount chipping away at the principal. As time progresses, this balance gradually shifts. Towards the latter half of your loan term, most of your payment starts working to reduce the principal balance, meaning you build equity more rapidly and pay less in total interest.

Flexible features can dramatically reshape your amortisation schedule. Making additional principal payments, arranging lump sum contributions, or adjusting your payment frequency can accelerate your loan repayment and potentially save thousands in interest over the loan’s lifetime. Mortgage repayment strategies outlined in New Zealand financial guides demonstrate how strategic approaches can significantly impact your long-term financial health, allowing borrowers to take control of their debt reduction journey.

Pro tip: Request a detailed amortisation schedule from your lender to visualise exactly how each payment impacts your loan balance and interest costs.

Impact On Total Loan Costs And Equity

The intricate relationship between amortisation, total loan costs, and home equity represents a critical financial landscape for New Zealand homeowners. Household economic surveys reveal significant variations in mortgage payment structures, demonstrating how strategic repayment approaches can substantially impact long-term financial outcomes. Understanding these dynamics allows borrowers to make informed decisions that minimise interest expenses and accelerate equity accumulation.

In the early stages of a mortgage, a larger proportion of each payment goes towards interest rather than reducing the principal balance. This means Kiwi homeowners initially build equity more slowly, with the majority of their monthly payment serving to cover the bank’s lending costs. As the loan progresses, the balance shifts, enabling more of each payment to directly reduce the principal. Strategic approaches such as making additional principal payments or choosing shorter loan terms can dramatically reduce total interest paid and speed up equity growth.

Research from Massey University highlights how lower interest rates and strategic repayment can significantly improve home loan affordability, providing New Zealand homeowners with opportunities to optimise their financial strategy. By understanding amortisation schedules, borrowers can implement techniques that reduce overall loan costs, such as making extra payments, refinancing at lower rates, or selecting loan terms that align with their long-term financial goals.

The following table highlights key factors that influence total loan costs and equity growth for New Zealand homeowners:

| Factor | Impact on Loan Costs | Effect on Equity | Strategic Benefit |

|---|---|---|---|

| Interest Rate | Higher rates increase costs | Slower equity build | Lower rates save money |

| Extra Payments | Reduces interest paid | Faster equity build | Shortens repayment period |

| Loan Term Length | Longer terms increase cost | Slower equity build | Short terms reduce interest |

| Lump Sum Contributions | Immediate reduction in debt | Quick equity increase | Flexibility in repayment |

Pro tip: Create a personalised spreadsheet tracking your loan’s amortisation schedule to visualise how each additional payment accelerates your equity build-up and reduces total interest costs.

Risks And Common Pitfalls To Avoid

Navigating home loan amortisation requires careful attention to potential financial risks that can derail your long-term financial stability. Understanding potential risks highlighted by banking ombudsman guidelines helps Kiwi borrowers prevent costly mortgage mistakes, particularly around maintaining consistent repayments and understanding loan terms. Missing payments or failing to communicate with your lender can quickly escalate into serious financial challenges, potentially leading to mortgagee sales or significant credit damage.

One of the most significant pitfalls involves misunderstanding the complex structure of loan amortisation. Many borrowers underestimate how much of their early payments go towards interest rather than reducing principal, which can create unrealistic expectations about equity build-up. Fixed-rate loans often come with early repayment penalties that can substantially increase costs if borrowers attempt to change their repayment strategy without understanding the contractual implications. This complexity demands careful scrutiny of loan documents and a thorough comprehension of potential financial implications.

The New Zealand Law Society’s Property Law Section Guidelines emphasise the critical importance of clear financial disclosure and professional advice, particularly when navigating the intricate landscape of home loan amortisation. Borrowers should be wary of hidden fees, complex penalty structures, and loan terms that might limit their financial flexibility. Additional risks include variable interest rates that can unexpectedly increase repayment amounts, potential changes in personal financial circumstances, and inadequate insurance or financial buffers to manage potential disruptions to income.

Pro tip: Request a comprehensive loan breakdown from your mortgage adviser, ensuring you fully understand all potential penalties, interest rate variations, and repayment flexibility before signing any loan agreement.

Take Control of Your Home Loan Amortisation with Expert Guidance

Understanding amortisation can feel overwhelming especially when each payment splits into interest and principal differently over time. You want to avoid costly pitfalls like surprise interest hikes or unclear repayment schedules that slow your equity growth. At Mortgage Managers we specialise in helping Kiwis across Auckland and beyond navigate these challenges with personalised mortgage advice tailored to your unique financial goals.

Take the stress out of managing your home loan by partnering with knowledgeable advisers who explain every detail clearly. Whether you want to visualise your amortisation schedule understand the best repayment structure for your situation or explore ways to reduce total interest quickly we can help. Don’t wait until loan confusion costs you more – visit Mortgage Managers today and discover how to optimise your mortgage repayments with confidence. Your smarter financial future starts with one simple step.

Frequently Asked Questions

What is amortisation in the context of home loans?

Amortisation refers to the process of gradually paying off a home loan through regular repayments that include both principal and interest, helping to reduce total debt over time.

How do different loan repayment types affect amortisation?

Different loan repayment types, such as table loans, revolving credit loans, and interest-only loans, impact how your payments are structured, which can influence how quickly you lower your principal and the total interest paid over the loan term.

What is an amortisation schedule and why is it important?

An amortisation schedule outlines how each mortgage payment is divided between principal and interest over time. It is important because it helps homeowners understand how their loan balance decreases and how interest costs accumulate during the loan’s lifecycle.

What factors should I consider to manage loan costs effectively?

When managing loan costs, consider the interest rate, loan term length, and the potential benefits of making extra payments or lump sum contributions, as these factors can significantly affect total interest paid and the speed of equity growth.