More than half of first home buyers in Auckland now consider mortgage top ups to fund home renovations, even when their budgets are tight or their deposits are small. Unlike many australian first-time buyers who face stricter lending rules, New Zealanders are finding creative ways to stretch their home loan potential. This article clears the confusion around how mortgage top ups work for real families, so you can plan your renovation and avoid costly mistakes.

Table of Contents

- What Is A Mortgage Top Up In New Zealand?

- Types Of Mortgage Top Ups For Renovations

- Lender Criteria And Application Requirements

- How The Top Up Process Works Step-By-Step

- Costs, Risks And Common Pitfalls To Avoid

Key Takeaways

| Point | Details |

|---|---|

| Mortgage Top Up Definition | A mortgage top up allows homeowners in New Zealand to access additional funds by increasing their existing home loan, using property equity for financial needs. |

| Types of Loans | Homeowners have various mortgage top up options for renovations, including table loans, revolving credit, offset loans, and specialised renovation loans, each suited for different financing needs. |

| Lender Evaluation Criteria | Lenders assess income stability, existing debt, and credit history before approving a top up, so a comprehensive financial portfolio is essential for a successful application. |

| Costs and Risks | It’s crucial to understand potential financial risks, such as underestimating costs and overextending borrowing, and to prepare a financial buffer for unexpected expenses. |

What Is a Mortgage Top Up in New Zealand?

A mortgage top up represents an additional borrowing option that allows homeowners to access extra funds by increasing their existing home loan. This financial strategy enables Kiwi property owners to leverage their property’s equity for various purposes, such as home renovations, debt consolidation, or major life investments.

In New Zealand, mortgage top ups function as an extension of your current home loan, essentially allowing you to borrow more money against the value of your property. Home loan top up options provide flexibility for homeowners who need additional funds without establishing an entirely new loan structure. The process involves reassessing your property’s current value and determining how much additional borrowing capacity you have based on your existing equity and financial circumstances.

Typically, mortgage top ups involve several key considerations. Lenders will evaluate factors like your current loan balance, property valuation, income stability, and overall creditworthiness. Unlike personal loans or credit cards, mortgage top ups are secured against your home, which often means lower interest rates and more favourable repayment terms. However, this also means increasing your existing mortgage balance and potentially extending your loan term.

Hot Tip: Before pursuing a mortgage top up, calculate your potential additional borrowing capacity and understand how the increased loan will impact your long term financial planning.

Types of Mortgage Top Ups for Renovations

New Zealand homeowners have several mortgage top up options available for renovation financing, each designed to meet different financial needs and renovation project requirements. Understanding these various types can help you select the most appropriate borrowing strategy for your home improvement goals.

One popular option is the table loan, which provides structured repayments with either fixed or floating interest rates. These loans are particularly suitable for homeowners who prefer predictable monthly payments and want clear visibility into their renovation financing. Another flexible alternative is the revolving credit loan, which functions similar to an overdraft account, allowing borrowers to access funds as needed during their renovation project and potentially reduce overall interest costs.

Additionally, offset loans offer a unique approach by linking your mortgage to your savings account, enabling you to offset your loan balance against your savings and potentially reduce the interest you pay. This can be particularly advantageous for renovation projects where you might have intermittent income or staged payment requirements. Some lenders also provide specialised renovation loan products that include progress payment structures tailored specifically for home improvement projects.

Pro Tip: Before selecting a mortgage top up for renovations, carefully assess your project’s specific financial requirements, cash flow needs, and long-term repayment capacity to choose the most suitable loan structure.

Here’s a comparison of common mortgage top up options for New Zealand renovations:

| Loan Type | Repayment Structure | Interest Rate Feature | Best For |

|---|---|---|---|

| Table Loan | Fixed regular payments | Fixed or floating rates | Stable repayment schedules |

| Revolving Credit | Flexible withdrawals | Floating rate | Projects with variable costs |

| Offset Loan | Linked to savings balance | Floating rate | Maximising interest savings |

| Special Renovation | Staged payments | Varies by lender | Large, phased renovations |

Lender Criteria and Application Requirements

Navigating the mortgage top up application process requires a comprehensive understanding of the lender criteria that financial institutions use to evaluate renovation financing requests. New Zealand lenders conduct thorough assessments to ensure borrowers can manage additional financial commitments responsibly and sustainably.

Under the responsible lending requirements, financial institutions must meticulously review several key factors before approving a mortgage top up. These typically include detailed documentation of your current income, employment stability, existing debt obligations, credit history, and the specific purpose of your renovation project. Lenders will closely examine your debt-to-income ratio, assessing whether the additional borrowing will create financial strain or remain manageable within your current economic circumstances.

The application process for a mortgage top up involves providing comprehensive financial documentation, including recent payslips, tax returns, bank statements, detailed renovation plans, and property valuation reports. Lenders will also evaluate the potential increase in your property’s value resulting from the proposed renovations. This assessment helps them determine the risk and potential long-term value of the proposed financing. Some institutions may require additional documentation such as contractor quotes, architectural plans, or detailed project timelines to support your application.

Pro Tip: Prepare a comprehensive financial portfolio before applying, including updated income documentation, a clear renovation plan, and a realistic budget to demonstrate your financial preparedness and increase your chances of approval.

How the Top Up Process Works Step-by-Step

Understanding the mortgage top up process can help New Zealand homeowners navigate their renovation financing more effectively. The journey from initial consideration to final fund approval involves several strategic steps that require careful planning and documentation.

Mortgage top up applications typically follow a structured pathway. Initially, homeowners must comprehensively assess their current mortgage and existing equity. This involves calculating how much additional borrowing capacity they have and determining the potential value added by their proposed renovation project. During this preliminary stage, gathering essential financial documents becomes crucial, including recent payslips, tax returns, bank statements, and detailed renovation plans.

The next phase involves direct engagement with your financial institution or mortgage broker. Here, you’ll present your renovation proposal, demonstrating the project’s feasibility and potential property value enhancement. Lenders will conduct thorough assessments, including credit checks, income verification, and a comprehensive review of your debt-to-income ratio. They’ll evaluate not just your current financial standing but also the long-term financial implications of the proposed top up. This might involve obtaining updated property valuations, reviewing contractor quotes, and assessing the renovation’s potential impact on your home’s market value.

Pro Tip: Create a comprehensive renovation portfolio before approaching lenders, including detailed project plans, professional quotes, and a clear financial breakdown to demonstrate your preparedness and increase your approval chances.

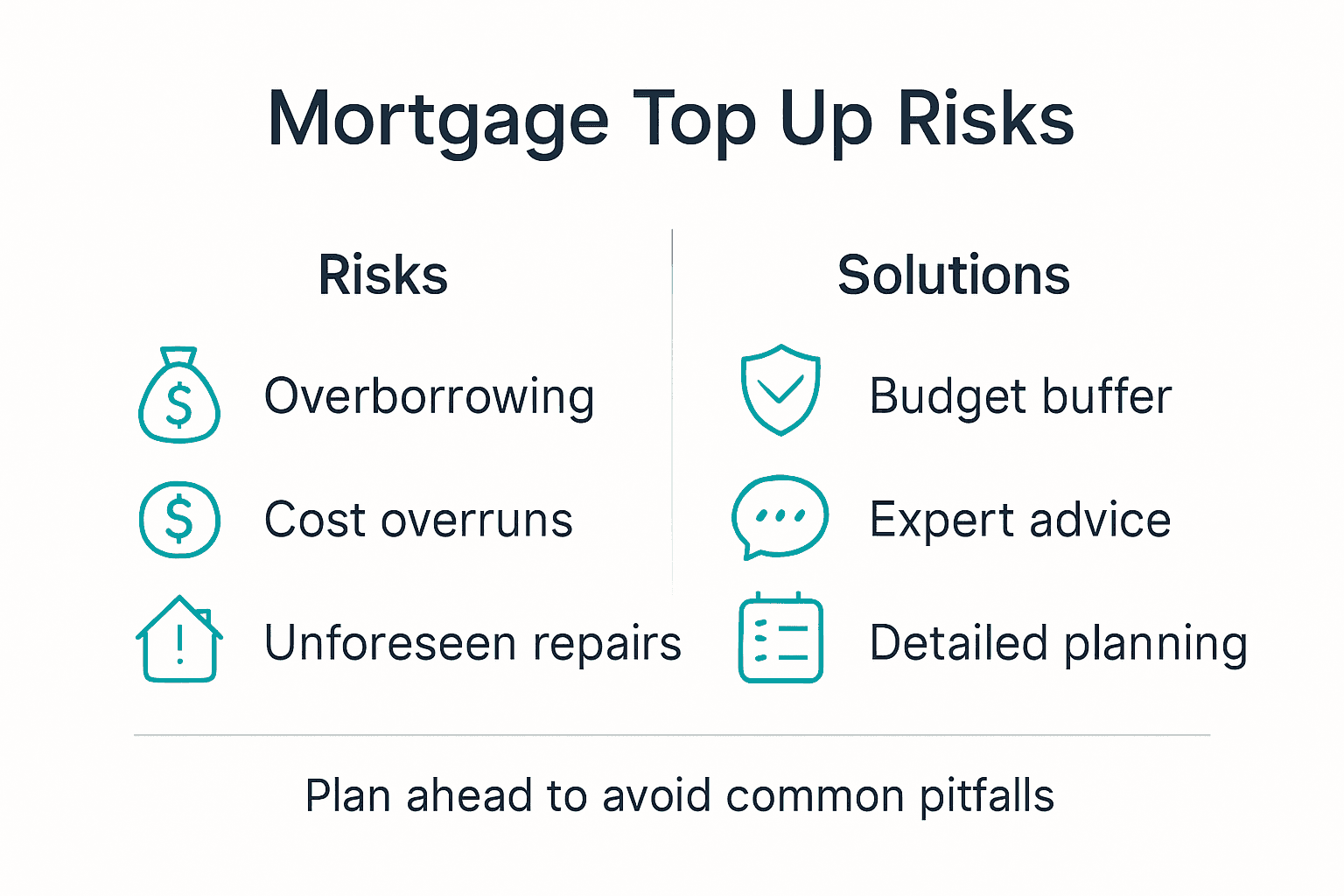

Costs, Risks and Common Pitfalls to Avoid

Mortgage top ups for renovation projects involve complex financial considerations that can significantly impact your long-term financial health. Financial risks are inherent in any borrowing strategy, and understanding these potential challenges is crucial for making informed decisions about your home improvement financing.

Renovation financing pitfalls often stem from underestimating project costs and overextending financial capabilities. Many homeowners encounter unexpected expenses that can rapidly escalate beyond initial budgets. Common risks include inadequate contingency planning, underestimating renovation complexity, and failing to account for potential structural issues or hidden property defects. These challenges can lead to substantial financial strain, potentially increasing your mortgage debt beyond anticipated levels and creating long-term repayment challenges.

Financial experts recommend careful evaluation of your borrowing capacity and a thorough understanding of the potential impact on your overall financial landscape. This involves critically assessing your current income stability, future earning potential, and the potential return on investment from your renovation project. Some key considerations include potential changes in interest rates, the impact of additional borrowing on your debt-to-income ratio, and the potential market value increase of your property. Homeowners should also be aware of potential penalties, additional fees, and the long-term implications of extending their mortgage term.

Key risks and expert strategies for managing mortgage top up renovations:

| Risk or Challenge | Potential Impact | Expert Risk Management Tip |

|---|---|---|

| Underestimating costs | Budget blowout, extra debt | Add a 15–20% contingency buffer |

| Overextending borrowing | Strain on repayments, stress | Assess current and future income |

| Ignoring future rate changes | Unexpected increases in repayments | Consider fixed vs floating loans |

| Incomplete documentation | Delayed or denied application | Prepare a thorough financial dossier |

| Not planning for contingencies | Project delays or halted works | Set aside emergency savings |

Pro Tip: Create a comprehensive financial buffer of at least 15-20% above your estimated renovation costs to manage unexpected expenses and protect yourself from potential financial overextension.

Expert Help with Your Mortgage Top Up for Renovations

If you are feeling overwhelmed by the complexities of securing a mortgage top up for your renovation project you are not alone. Many New Zealand homeowners struggle with understanding lender criteria managing costs and choosing the right loan structure to suit their needs. Whether it is navigating fixed versus floating rates or preparing comprehensive financial documents having trusted guidance can make all the difference.

Mortgage Managers is a local financial services business based in Hobsonville specialising in mortgage advice for Kiwis across Auckland and remotely throughout New Zealand. Our experienced mortgage advisers understand the unique challenges of renovation finance and can help you explore your options including home loan top ups tailored to your situation.

Take control of your renovation funding today by consulting with experts who make the process clear and manageable. Discover how we can help you get the best possible outcome on your mortgage top up by visiting Mortgage Managers. Act now to secure finance solutions that fit your long term goals and bring your dream home improvements within reach.

Frequently Asked Questions

What is a mortgage top up?

A mortgage top up is an additional borrowing option that allows homeowners to access extra funds by increasing their existing home loan. It enables property owners to leverage their property’s equity for various purposes such as renovations or debt consolidation.

How does the mortgage top up process work in New Zealand?

The mortgage top up process involves assessing your current mortgage and equity, gathering financial documents, and presenting a detailed renovation proposal to lenders. They will evaluate factors such as creditworthiness, income stability, and the potential increase in your property’s value due to renovations.

What types of mortgage top ups are available for renovations?

Common types of mortgage top ups for renovations include table loans, revolving credit loans, offset loans, and specialised renovation loans. Each option offers different repayment structures and features, catering to various financial needs and project types.

What are the risks associated with mortgage top ups for renovations?

Risks include underestimating project costs, overextending borrowing, and ignoring future interest rate changes. Effective risk management strategies, such as adding a contingency buffer and preparing thorough documentation, can help mitigate these challenges.