Kiwis need bad credit home loans explained and so we provided this article.

Over 70% of borrowers with credit challenges believe home ownership is out of reach, yet many australian and New Zealand lenders now offer pathways that defy this assumption. Access to property financing remains a real concern for families facing setbacks like job loss or medical emergencies. This guide demystifies bad credit home loans, exploring how they provide hope, tangible options, and renewed confidence for those ready to rebuild and invest in their own future.

Table of Contents

- What Are Bad Credit Home Loans?

- Types Of Bad Credit Lending In NZ

- Eligibility Criteria And Application Process

- Low Deposit Solutions And Alternatives

- Risks, Costs And Common Pitfalls

Key Takeaways

| Point | Details |

|---|---|

| Bad Credit Home Loans Support Financial Inclusion | These loans cater to New Zealanders with challenging credit histories, providing alternative pathways to homeownership. |

| Higher Costs and Risks Involved | Borrowers may face significantly higher interest rates and fees, necessitating thorough financial assessment before proceeding. |

| Comprehensive Application Process | Lenders require detailed documentation, including proof of income and explanations of past credit issues, to assess applicants effectively. |

| Low Deposit Solutions Available | Numerous options, such as the First Home Loan scheme, help first-time buyers enter the market with limited upfront capital. |

What Are Bad Credit Home Loans?

Bad credit home loans are specialised mortgage products designed to help New Zealanders with challenging credit histories secure property financing. Unlike traditional mortgages, these financial solutions acknowledge that past financial challenges do not necessarily predict future repayment capabilities. Home loan options for individuals with credit difficulties often come with unique considerations that protect both borrowers and lenders.

Typically, bad credit home loans differ from standard mortgages in several key aspects. Lenders assess applications more comprehensively, considering factors beyond traditional credit scores. These loans frequently feature higher interest rates to offset the increased risk, and may require larger deposit amounts or additional security. Borrowers might need to demonstrate consistent income, stable employment, and a commitment to improving their financial position.

The core purpose of bad credit home loans is financial inclusion. They recognise that credit challenges can arise from various life circumstances such as job loss, medical emergencies, or unexpected economic disruptions. By providing alternative pathways to homeownership, these loans help New Zealanders rebuild their financial credibility and achieve their property ownership dreams. Each loan is uniquely structured, taking into account the individual’s specific financial history and current economic circumstances.

Key characteristics of bad credit home loans include:

- Higher interest rates compared to standard mortgages

- More rigorous application and assessment processes

- Potential requirement for additional security or guarantors

- Opportunities to demonstrate financial rehabilitation

- Flexible terms tailored to individual financial situations

Types Of Bad Credit Lending In NZ

New Zealand offers several distinctive lending options for individuals with challenging credit histories. Lending solutions for those with credit difficulties range from secured loans to specialised financial products designed to support borrowers facing traditional banking barriers. These alternatives recognise that credit challenges are complex and should not permanently exclude individuals from financial opportunities.

Secured Loans represent a primary lending category for bad credit borrowers. In these arrangements, borrowers provide valuable assets like property or vehicles as collateral, which reduces the lender’s risk and increases approval chances. Unsecured Loans offer another pathway, though typically featuring higher interest rates to compensate for the increased lending risk. These loans do not require specific collateral but demand rigorous assessment of the borrower’s income stability and repayment capacity.

Microfinance and short-term lending options provide additional alternatives for New Zealanders navigating credit challenges. Payday loans, while offering rapid access to funds, often come with extremely high interest rates and should be approached cautiously. Specialised microfinance institutions focus on providing smaller loan amounts with more flexible assessment criteria, helping borrowers rebuild their financial credibility through responsible lending practices.

Key types of bad credit lending in New Zealand include:

- Secured personal loans with property or asset collateral

- Unsecured personal loans with higher interest rates

- Microfinance loans for smaller funding requirements

- Payday loans for short-term emergency financing

- Guarantor loans involving a secondary responsible party

Ultimately, each lending option carries unique advantages and considerations, requiring borrowers to carefully evaluate their specific financial circumstances and long-term goals.

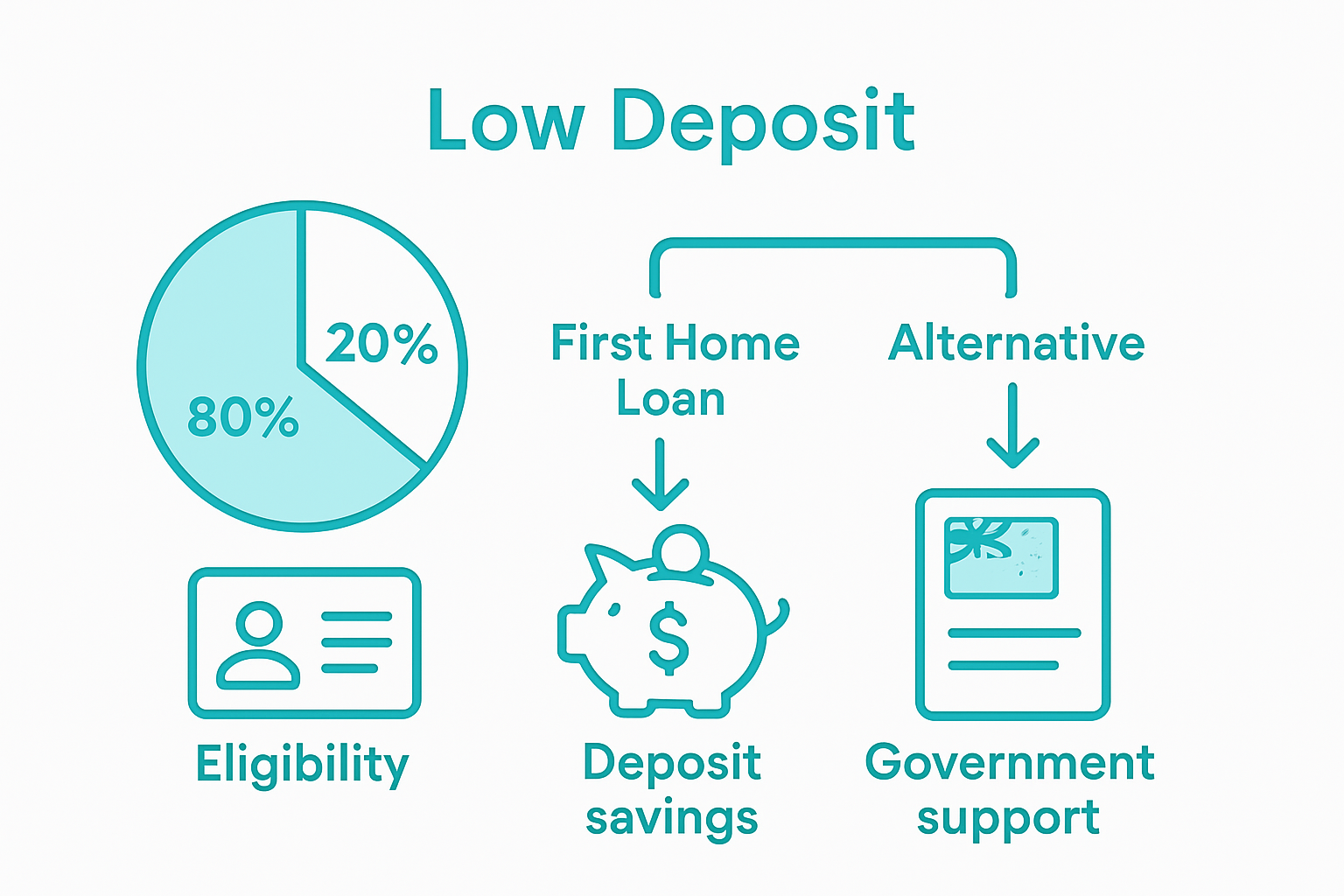

Eligibility Criteria And Application Process

Bad credit home loan applications involve a comprehensive assessment process that goes beyond traditional lending criteria. Detailed lending requirements for borrowers emphasise the importance of demonstrating financial stability and repayment capacity. Lenders carefully evaluate multiple aspects of a borrower’s financial profile to mitigate potential risks associated with lending to individuals with challenging credit histories.

Income Verification stands as a critical component of the application process. Borrowers must typically provide comprehensive documentation including recent payslips, tax returns, and employment verification. Lenders look for consistent and stable income streams that suggest the ability to meet regular mortgage repayments. Self-employed applicants may need to supply additional documentation, such as business financial statements and income tax records, to substantiate their earning potential.

Credit history assessment takes a nuanced approach for bad credit home loans. While previous credit challenges are acknowledged, lenders focus on recent financial behaviour and demonstrated improvement. Applicants are often required to explain past credit issues, provide evidence of financial rehabilitation, and show current financial responsibility. This might include presenting a record of consistent bill payments, reducing existing debt, and maintaining a stable employment history. Some lenders may require additional security measures, such as a guarantor or larger deposit, to offset the perceived lending risk.

Key eligibility criteria typically include:

- Proof of stable and consistent income

- Detailed explanation of previous credit challenges

- Evidence of financial improvement and responsible money management

- Acceptable debt-to-income ratio

- Potential requirement for additional security or guarantor

- Minimum age requirement (usually 18 years or older)

- New Zealand residency or appropriate visa status

The application process for bad credit home loans is designed to be thorough yet supportive. Prospective borrowers should prepare comprehensive documentation and be prepared to provide detailed insights into their financial journey, demonstrating their commitment to financial stability and responsible borrowing.

Low Deposit Solutions And Alternatives

New Zealand offers several innovative pathways for borrowers seeking home ownership with limited upfront capital. Low deposit lending options for first-time buyers provide strategic alternatives to traditional high-deposit mortgage requirements. These solutions recognise that many aspiring homeowners face significant challenges in accumulating substantial savings.

The First Home Loan scheme emerges as a cornerstone of low deposit solutions, enabling eligible first-time buyers to enter the property market with as little as 5% deposit. This government-backed initiative dramatically reduces the initial financial barrier, making homeownership more accessible. Shared ownership schemes offer another compelling alternative, allowing buyers to purchase a percentage of a property while paying rent on the remaining portion, effectively lowering the required upfront investment.

Guarantor loans represent a powerful option for borrowers with limited deposits or challenging credit histories. In these arrangements, a trusted family member or close associate provides additional security by offering their own property or financial backing. This approach allows lenders to mitigate risk while giving borrowers a meaningful pathway to property ownership. Alternative lending institutions increasingly consider non-traditional credit assessments, recognising that past financial challenges do not necessarily predict future financial responsibility.

Key low deposit solutions include:

- First Home Loan scheme (5% deposit)

- Shared ownership programmes

- Guarantor loan arrangements

- Family support equity contributions

- Specialised low deposit mortgage products

Prospective buyers should carefully assess each option, understanding the unique requirements, potential additional costs, and long-term financial implications of alternative lending approaches.

Risks, Costs And Common Pitfalls

Bad credit home loans present a complex financial landscape with significant potential risks that borrowers must carefully navigate. Understanding lending risks and consumer protections is crucial for making informed financial decisions. These specialised loan products often come with substantially higher costs and more stringent conditions compared to traditional mortgage offerings.

Interest Rates represent the most immediate financial challenge for bad credit borrowers. Lenders typically impose significantly elevated interest rates to compensate for the perceived higher risk, which can translate to substantially increased total loan costs over the mortgage’s lifetime. Some loans may include variable rate structures that can fluctuate unpredictably, potentially creating additional financial strain. Borrowers must meticulously calculate the long-term financial implications, understanding that even a small percentage increase can result in tens of thousands of additional dollars paid over the loan’s duration.

Predatory lending practices pose another critical risk for vulnerable borrowers. Some unscrupulous lenders exploit individuals with challenging credit histories by embedding complex fee structures, punitive penalty clauses, and restrictive conditions within loan agreements. Comprehensive loan term assessment becomes essential to avoid potential financial traps. Borrowers should be particularly wary of loans that include excessive establishment fees, ongoing administrative charges, or penalties for early repayment.

Key risks and potential pitfalls include:

- Significantly higher interest rates

- Substantial establishment and ongoing fees

- Potential for variable interest rate fluctuations

- Risk of loan default and property repossession

- Complex and potentially exploitative loan terms

- Limited refinancing opportunities

Prospective borrowers must approach bad credit home loans with comprehensive research, professional financial advice, and a thorough understanding of their long-term financial capacity and goals.

Secure Your Home Ownership Journey Despite Credit Challenges

Struggling with bad credit can make the dream of owning a home feel out of reach. This article highlights important options like bad credit home loans, low deposit solutions, and the need to understand eligibility criteria and risks. At Mortgage Managers we understand that past credit difficulties do not define your future financial potential. Based in Hobsonville we help New Zealanders across Auckland and beyond navigate these complex lending options with confidence and personalised support.

Take control of your home ownership goals with expert advice tailored to your unique situation. Visit Mortgage Managers today to explore how we can connect you with flexible lending solutions that match your needs. Whether you’re looking for low deposit options, guarantor loans or advice on improving your eligibility criteria we are ready to help you move forward with clarity and confidence. Don’t let credit setbacks hold you back make your move now and start building your future home.

Frequently Asked Questions

What are bad credit home loans?

Bad credit home loans are mortgage products specifically designed for individuals with challenging credit histories, allowing them to secure property financing despite previous financial difficulties.

How do bad credit home loans differ from traditional mortgages?

Bad credit home loans often feature higher interest rates, more rigorous application processes, and may require additional security or larger deposits, as lenders consider a broader spectrum of financial history.

What are the eligibility criteria for applying for a bad credit home loan?

Eligibility typically includes proof of stable and consistent income, a detailed explanation of past credit challenges, evidence of financial improvement, and potentially additional security or a guarantor.

What are the risks associated with bad credit home loans?

Key risks include significantly higher interest rates, substantial fees, the potential for variable rate fluctuations, and the risk of loan default and property repossession if payments are not met.

Recommended

- Bad Credit Home Loans – Mortgage Managers

- 7 Mortgage Approval Tips for Bad Credit in New Zealand – Mortgage Managers

- You Have Bad Credit But Need A Home Loan – Mortgage Managers

- Types of Home Loans NZ: Complete 2024 Guide | Mortgage Managers

- Getting A Mortgage With Japanese Knotweed – Japanese Knot Weed