TL;DR:

- Choosing a fixed mortgage rate locks your payments for a set period, providing budget certainty regardless of market changes. Fixed terms typically range from 6 months to 5 years, with early break fees potentially costing thousands if you exit early. Short-term fixes often outperform long ones in a falling rate environment, offering flexibility and savings for New Zealand homeowners.

Choosing a mortgage rate is one of the biggest financial decisions you’ll make, yet many first-home buyers across New Zealand feel genuinely confused about what a fixed interest rate actually means for them. The idea of locking in a rate sounds simple enough, but the details, such as which term to choose, what happens if you break it early, and whether fixed or floating suits your situation, trip people up constantly. This guide cuts through that confusion. By the end, you’ll understand exactly how fixed interest rates work, what they cost, and how to use them to your advantage.

Table of Contents

- What is a fixed interest rate and how does it work?

- How fixed rates compare with floating rates in New Zealand

- What are the costs and risks of fixed interest rates?

- How to choose the right fixed term for your mortgage

- Using fixed rates strategically: tips for first home buyers and homeowners

- Perspective: why short-term fixed rates often trump long locks in NZ today

- How mortgage advisers help you navigate fixed interest rates

- Frequently asked questions

What is a fixed interest rate and how does it work?

At its core, a fixed interest rate mortgage locks your interest rate in place for a set period. Your repayments stay the same week after week, fortnight after fortnight, regardless of what happens in the wider economy. As MoneyBalance explains, a fixed interest rate mortgage in New Zealand locks your rate for a period typically ranging from 6 months to 5 years, with repayments staying exactly the same regardless of RBNZ OCR changes or wholesale market movements.

That consistency is the whole point. When the Reserve Bank of New Zealand (RBNZ) moves the Official Cash Rate (OCR) up or down, your fixed rate mortgage does not budge. You know precisely what you owe each payment cycle, which makes budgeting far easier, especially in your first years of homeownership.

Here is what you need to know about why mortgage rates change and how fixed terms are structured in New Zealand:

- Fixed terms available: 6 months, 1 year, 2 years, 3 years, 4 years, and 5 years. The 1 and 2-year terms are by far the most popular among Kiwi borrowers.

- Repayments: Fixed throughout the entire term, giving you a predictable budget.

- At the end of your term: You choose to refix at a new rate, move to a floating rate, or refinance with a different lender.

- Break fees: Penalties charged if you exit the fixed term early, whether by selling, refinancing, or making large unplanned repayments.

- OCR protection: During your fixed term, OCR increases cannot touch your rate. Neither can decreases.

The fixed term is your financial breathing space. It removes one major variable from your monthly budget, which is worth a great deal when you are also managing rates, insurance, and the general costs of owning a home for the first time.

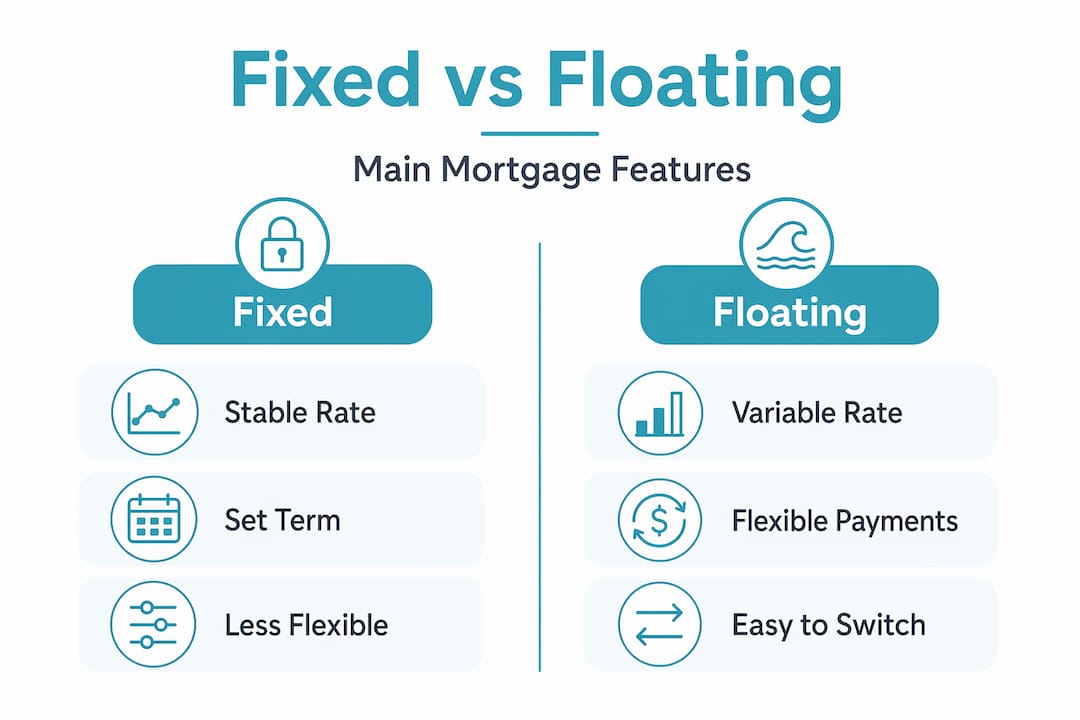

How fixed rates compare with floating rates in New Zealand

Now that you understand fixed rates, it helps to see exactly how they stack up against floating rates. A floating rate (also called a variable rate) moves in line with market conditions and the OCR. When the RBNZ cuts rates, your floating mortgage can get cheaper. When it raises them, your repayments go up.

The rate difference right now is significant. Current NZ mortgage rates show typical fixed rates of 5.55%–5.60% for 1-year terms and 5.30%–5.55% for 2-year terms, while floating rates average 6.99%–7.09%, making short-term fixed rates 1%–2% lower than floating in most cases. That gap translates directly into hundreds of dollars saved each month on a typical Auckland home loan.

| Feature | Fixed rate | Floating rate |

|---|---|---|

| Rate stability | Locked for set term | Changes with OCR/market |

| Current typical rate | 5.30%–5.60% (1-2 yr) | 6.99%–7.09% |

| Budget certainty | High | Low |

| Extra repayments | Restricted | Flexible |

| Break fees | Yes, can be significant | Generally none |

| Best for | Certainty seekers, rate-rise worries | Flexibility, lump sums, falling rates |

The main advantage of floating is flexibility. You can make large extra repayments, switch lenders, or pay off your loan at any time without penalty. That freedom has real value if, for example, you are expecting a bonus, an inheritance, or planning to sell within the next year or two.

The main disadvantage? The impact of interest rates can hit hard when the OCR rises suddenly. Your repayments increase immediately, and there is no protection.

Pro Tip: Fix for a short term (1 year) when you expect rates to rise or stay elevated. Consider floating only if you expect stable or falling rates and genuinely need the repayment flexibility. Most Kiwis in the current environment are better served by fixing.

What are the costs and risks of fixed interest rates?

Fixed rates offer certainty, but that certainty comes with conditions. Breaking a fixed mortgage before the term ends can be expensive, and it catches many borrowers off guard.

Break fees exist because when you exit a fixed mortgage early, your lender loses the interest income they expected to earn. They calculate the fee based on the difference between your fixed rate and the current wholesale rate for the remaining term. As Lifetimes NZ outlines, break fees for early exit range from 1%–3% of the balance for one year remaining on the term, increasing for longer terms, and can be tens of thousands of dollars on typical loans. Banks provide free quotes.

On a $600,000 mortgage with 18 months remaining on a fixed term, a break fee could easily reach $10,000–$18,000 depending on the rate differential. Always get a written quote before making any decisions.

Here is how to protect yourself from unexpected break fee costs:

- Request a free break fee quote from your lender before you commit to anything. Quotes are typically valid for 3–7 days.

- Understand your remaining term. The longer you have left on your fixed period, the higher the potential break fee.

- Factor in rate differentials. If current wholesale rates have fallen since you fixed, your break fee will be higher.

- Check extra repayment limits. Most fixed loans allow limited overpayments (often up to $500 per week or $10,000 per year) without triggering fees.

- Plan major life events. If you are likely to sell or refinance your mortgage within the fixed term, either choose a shorter term or build the break fee cost into your planning.

Pro Tip: Always get a written break fee estimate from your bank before deciding to refix, refinance, or sell. It is free, takes minutes, and can save you thousands by helping you time your decisions correctly.

How to choose the right fixed term for your mortgage

Choosing a fixed term is not just about chasing the lowest advertised rate. It is about matching your term to your life. Your plans for the next few years matter enormously here.

The most common approach among NZ homeowners is to favour fixed rates for budget protection, particularly amid OCR volatility. Floating suits those planning sales or lump sums within 1–2 years, while 1–2 year fixes often outperform longer terms in falling rate cycles.

| Term | Typical rate (2026) | Best suited for |

|---|---|---|

| 6 months | ~5.75% | Rate uncertainty, planning to reassess soon |

| 1 year | 5.55%–5.60% | Expecting rate drops, want short commitment |

| 2 years | 5.30%–5.55% | Balance of certainty and flexibility |

| 3 years | ~5.80% | Stable budget, no major changes planned |

| 5 years | ~5.95% | Long-term certainty, rate-rise protection |

Here are the scenarios where each approach tends to work best:

- Short fixes (6 months to 1 year): Ideal if you expect rates to fall further or if you are unsure about your near-term plans. You give up a little certainty but gain the ability to refix at a potentially lower rate soon.

- Medium fixes (2 to 3 years): The sweet spot for most Kiwi borrowers right now. You lock in a competitive rate for long enough to budget with confidence without overcommitting.

- Long fixes (4 to 5 years): Worth considering only if you are certain rates will rise significantly and you have no plans to sell or make large repayments. The cost of breaking a 5-year term early is serious.

Timing your fix around RBNZ OCR announcements can also work in your favour. Banks often adjust their fixed rates in anticipation of OCR moves, so acting just before an expected cut can mean the difference between a good rate and a great one.

Pro Tip: Consider splitting your mortgage across two terms, for example, 50% on a 1-year fix and 50% on a 2-year fix. This approach averages your rate, reduces risk, and ensures at least part of your loan is always coming up for renewal, giving you opportunities to capture better rates as they emerge.

Using fixed rates strategically: tips for first home buyers and homeowners

Knowledge about fixed rate terms and break fees is most powerful when you put it to work. Here is how to approach your mortgage with genuine strategy rather than just picking the lowest number on a rate sheet.

As MoneyBalance notes, first-home buyers often overlook restrictions on extra repayments under fixed mortgages. Split structures allow combining fixed certainty with floating repayment flexibility, which is a practical way to get the best of both worlds.

For first-home buyers entering the market in 2026, a short 1-2 year fix provides a practical buffer against rate movements while preserving the ability to restructure when the rate environment becomes clearer.

Here are the steps to use fixed rates strategically:

- Review your budget honestly. Know exactly what repayment amount your household can sustain comfortably. This sets the ceiling for your loan structure decisions.

- Assess your plans for the next 2–3 years. Are you likely to sell, renovate, or receive a large sum? These scenarios influence your ideal term.

- Split your loan if it suits. Mixing terms creates natural rollover points so you are never entirely exposed to rate movements at once.

- Watch the OCR calendar. The RBNZ reviews the OCR roughly every six weeks. If a cut is expected, it may pay to wait a short while before refixing.

- Lock rates in advance if possible. Some lenders allow you to get better fixed rates by reserving a rate up to 60 days before your current term expires, protecting you if rates shift before rollover.

- Never break a fixed term without a written cost estimate. The savings you imagine from switching might be completely wiped out by the break fee.

The split mortgage structure deserves particular attention. By splitting a $700,000 loan into, say, $400,000 on a 1-year fix and $300,000 on a 2-year fix, you reduce your risk exposure while ensuring regular review points where you can adjust your strategy.

Perspective: why short-term fixed rates often trump long locks in NZ today

Here is the truth that does not always make it into the rate comparison tables. Many borrowers assume that locking in a long fixed rate is the “safe” choice. In a falling rate environment, it is often the most expensive one.

The current NZ market has seen significant OCR movement, with the RBNZ cutting rates through late 2024 and into 2025. Short-term fixed rates outperformed longer terms during these falling rate cycles. Break fees make long fixes risky if rates drop further. Borrowers who locked into 3 or 5-year terms at the peak found themselves unable to access lower rates without paying thousands to exit early.

The risks of locking long in a volatile market include:

- Missing rate cuts at your rollover point, because you are still locked into a higher rate.

- High break fees if your circumstances change and you need to exit before term.

- Opportunity cost of not being able to refix at significantly lower rates that may emerge in the next 12–18 months.

The advantages of staying short (1–2 year terms) right now include flexibility to capture falling rates at each rollover, lower break fee exposure if your plans change, and access to the most competitive rates currently available in the NZ market.

We have seen too many Kiwi homeowners lock into a 5-year fix for peace of mind, only to watch rates fall and feel trapped. Our view is that careful fixed rate planning almost always outperforms the set-and-forget approach. Use a rate ladder, keep your terms short, and review every time a term expires.

How mortgage advisers help you navigate fixed interest rates

Knowing the theory is one thing. Applying it to your specific loan, lender, and life situation is where things get complex, and where expert guidance genuinely earns its keep.

At Mortgage Managers, we work with first-home buyers and existing homeowners across Auckland, the North Shore, West Auckland, and throughout New Zealand to help them make confident fixed rate decisions. Getting mortgage advice early in your property journey means you understand your options before pressure mounts. Our advisers compare rates across multiple lenders, model split structures, calculate break fee scenarios, and help you time your fixes around OCR announcements. Think of us as your mortgage adviser support team, working on your behalf to find the right structure at the right time. Whether you are buying your first home or reviewing your existing loan, reach out to Mortgage Managers for personalised advice on fixing your mortgage that could save you thousands.

Frequently asked questions

What exactly happens to my mortgage repayments during a fixed interest rate term?

Your repayments stay the same throughout the fixed term, regardless of any OCR changes or market shifts, giving you full budget certainty from day one.

Can I make extra repayments on a fixed rate mortgage without incurring fees?

Most fixed rate mortgages limit extra repayments, and fixed loans generally offer less flexibility than floating loans for additional payments, so check your specific loan terms before making large lump sum contributions.

What are break fees and how can they affect me if I refinance early?

Break fees are penalties for exiting a fixed mortgage before the term ends. Break fees range from 1%–3% for one year remaining and up to 5%–10% or more for longer terms, potentially costing tens of thousands on a standard home loan.

When is it generally better to choose a fixed interest rate over a floating rate?

Experts recommend fixing when you expect rates to rise or want repayment certainty, while floating suits those who need flexibility or believe rates will remain stable or fall.

How can I estimate the cost before breaking a fixed rate mortgage?

Banks provide free break fee quotes valid for 3–7 days, calculated on your remaining balance, term, and current wholesale rates, so you can assess whether breaking your fix makes financial sense before committing.