TL;DR:

- The Reserve Bank of New Zealand influences lending beyond interest rates through liquidity management and collateral rules. These functions impact mortgage rates, bank lending capacity, and borrower options, especially during market stress. Understanding both OCR adjustments and liquidity operations helps borrowers and advisers navigate evolving credit conditions effectively.

Most New Zealanders know the Reserve Bank sets interest rates. What far fewer realise is that the role of reserve bank in lending extends well beyond that single lever. The Reserve Bank of New Zealand (RBNZ) also manages liquidity in the financial system, sets collateral rules for banks, and acts as a backstop during market stress. Each of these functions shapes what mortgage rates you see, how readily banks lend, and what options you have when buying your first or next home.

Table of Contents

- Key takeaways

- How the Reserve Bank influences lending

- Liquidity facilities and how they support bank lending

- Impact on home loan conditions for borrowers

- OCR vs liquidity operations: what is the difference?

- Practical tips for NZ home buyers

- My take: what most people get wrong about the Reserve Bank

- Work with advisers who track these changes

- FAQ

Key takeaways

| Point | Details |

|---|---|

| OCR drives mortgage rates | Changes to the Official Cash Rate flow through to home loan rates, affecting your borrowing costs directly. |

| Liquidity tools matter too | The Reserve Bank’s liquidity facilities stabilise funding conditions and help prevent sudden tightening of credit. |

| Non-bank lenders are affected | Reserve Bank policies on collateral and liquidity access influence smaller and non-bank lenders, widening your options. |

| Two distinct tools at work | OCR adjustments and liquidity operations serve different purposes and affect lending in different ways at different times. |

| Advisers track these shifts | A good mortgage adviser monitors Reserve Bank changes and connects you to lenders best positioned in any given environment. |

How the Reserve Bank influences lending

The most direct expression of central bank lending policies is the Official Cash Rate. The OCR is the interest rate the Reserve Bank charges commercial banks for overnight lending, and it sets the floor for the cost of money across the entire financial system. When the OCR rises, banks pay more to fund themselves, and that cost gets passed on to you through higher mortgage rates. When it falls, funding becomes cheaper, and lending rates tend to follow.

The transmission from OCR to your mortgage rate is not instant or mechanical, but it is reliable. Banks price their fixed and floating rates based on wholesale funding costs, which track the OCR closely. Swap rates, term deposit competition, and offshore funding costs also play a role, which is why mortgage rates change for reasons that are not always obvious.

The RBNZ’s recent cutting cycle illustrates this well. The OCR was lowered to 2.25%, and the average mortgage yield fell to 5.4%, with expectations it could drop further to around 4.7% by September 2026. That is a material reduction in borrowing costs for households carrying home loans. For someone with a $600,000 mortgage, even a one percentage point reduction in their rate translates to thousands of dollars in annual savings.

Understanding how the OCR works also helps you time your decisions. Fixed rate terms are priced on where markets expect the OCR to go, not just where it sits today. So if cuts are already priced in, locking in a short fixed term may give you access to lower rates sooner rather than later.

Liquidity facilities and how they support bank lending

Here is the part most people miss entirely. Beyond setting the OCR, the Reserve Bank provides a set of liquidity facilities that shape how smoothly money moves through the banking system. These tools are less visible than an OCR announcement, but their impact on reserve bank credit conditions is just as real.

The main tools include the Exchange Settlement Account System (ESAS), the Bond Lending Facility, and the Overnight Reverse Repo. Each is priced relative to the OCR to create what economists call an interest rate corridor. As of February 2026, ESAS balances earn the Overnight Deposit Rate, the Bond Lending Facility is priced at OCR minus 50 basis points, and the Overnight Reverse Repo is priced at OCR plus 50 basis points. This corridor guides banks in managing their settlement cash and reduces volatility in short-term funding costs.

| Facility | Pricing relative to OCR | Primary purpose |

|---|---|---|

| ESAS (Overnight Deposit) | At Overnight Deposit Rate | Remunerates surplus settlement cash held by banks |

| Bond Lending Facility | OCR minus 50 bps | Provides securities lending to ease collateral shortages |

| Overnight Reverse Repo | OCR plus 50 bps | Supplies short-term liquidity to banks against collateral |

| Committed Liquidity Facility (CLF) | Activated under stress | Backstop liquidity for banks in market disruption |

The Reserve Bank is also reviewing its broader liquidity framework. Proposed changes include expanding repo tenors, tightening activation thresholds, and increasing Committed Liquidity Facility amounts to provide stronger stress backstops. This represents a shift from reactive crisis management to proactive, predictable liquidity provision.

Pro Tip: When you hear the Reserve Bank is reviewing its liquidity settings, that is worth paying attention to. Even if the OCR does not change, an expansion of liquidity support can reduce banks’ funding uncertainty, which sometimes feeds through to more competitive mortgage pricing.

Impact on home loan conditions for borrowers

So what does all this mean when you are sitting across from a bank manager or comparing home loan rates online? The functions of reserve banks translate into real-world outcomes for borrowers in several ways.

Stable liquidity provision from the Reserve Bank reduces the risk of sudden mortgage pullbacks. When banks know they can access short-term funding reliably, they are more willing to maintain their lending capacity even during uncertain periods. Liquidity backstops lower uncertainty, supporting sustained credit availability even if the OCR remains unchanged. This is particularly important for borrowers during periods of economic volatility, when banks might otherwise tighten their criteria to manage funding risk.

Here is what this means practically for you:

- Mortgage availability stays more consistent. When liquidity is well managed, banks are less likely to abruptly pull back on home lending even in uncertain conditions.

- Rate competition between lenders stays active. Stable wholesale funding costs mean banks compete more actively on retail lending rates rather than prioritising margin protection.

- Non-bank lenders can remain competitive. Wider collateral eligibility and CLF access help smaller lenders maintain funding, which broadens your options beyond the major banks.

- Your borrowing criteria may reflect funding conditions. During funding stress, lenders may tighten loan-to-value requirements or serviceability tests even if the OCR does not move.

Pro Tip: If you are close to your borrowing limits, do not assume that a stable OCR means all lenders will hold their criteria steady. Funding market conditions can shift lending appetite even when official rates stay put. A mortgage adviser can alert you to these shifts before they affect your application.

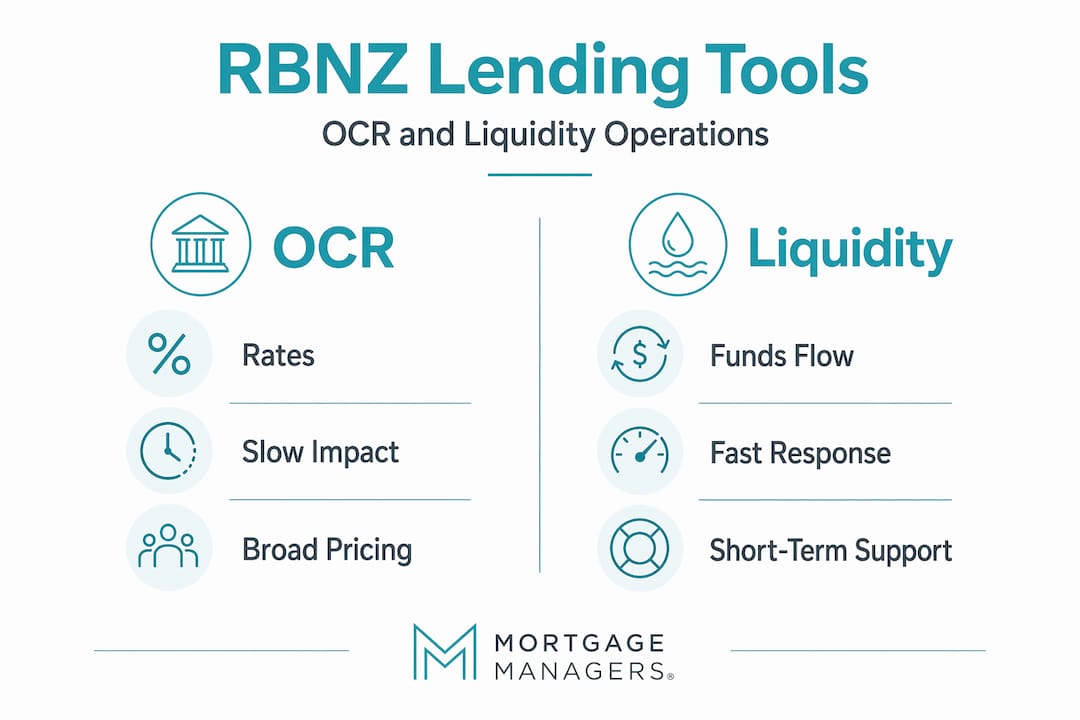

OCR vs liquidity operations: what is the difference?

The Reserve Bank holds two distinct sets of tools when it comes to how reserve banks influence loans, and understanding the difference helps you read market conditions more clearly.

| Feature | OCR adjustments | Liquidity operations |

|---|---|---|

| Primary target | Price of money (interest rates) | Availability of money (funding supply) |

| Typical frequency | Eight formal reviews per year | Ongoing, daily market operations |

| Market impact | Shifts retail lending and deposit rates | Reduces funding volatility and collateral stress |

| Best suited for | Managing inflation and economic growth | Smoothing market stress and ensuring credit flow |

| Borrower impact | Changes your actual mortgage rate | Affects lender willingness and capacity to lend |

OCR changes are the blunt instrument. They work slowly, filtering through the system over weeks and months. Liquidity operations are more surgical. They address specific pressure points in the funding system without necessarily moving the headline interest rate. During 2020, for example, central banks globally held rates near zero while simultaneously deploying massive liquidity operations to keep credit flowing. The OCR alone would not have been sufficient.

For New Zealand borrowers, this dual framework means that the Reserve Bank’s influence on your home loan is broader than the number announced at each Monetary Policy Committee meeting. The purpose of central bank in lending encompasses both the price signal and the plumbing that keeps money moving through the system.

Practical tips for NZ home buyers

Now that you understand the mechanics, here is how to put that knowledge to work when making mortgage decisions.

-

Watch OCR announcements closely. The RBNZ holds eight Monetary Policy Committee meetings per year. Each one can shift fixed mortgage rates within days, especially for short-term fixed products. If a cut is expected, some lenders move in advance. Knowing the schedule helps you time a refix or a new application more strategically.

-

Pay attention to liquidity commentary. Reserve Bank financial markets statements and liquidity reviews are not headline news, but they contain signals about credit conditions. A shift toward more generous collateral rules or expanded CLF amounts often precedes improved lending conditions for borrowers.

-

Consider non-bank lenders seriously. Because non-bank lenders access funding partly through Reserve Bank facilitated channels, improvements in liquidity provision can make their rates more competitive. They also apply different credit criteria, which can benefit borrowers who do not fit standard bank templates.

-

Understand your rate is not just the OCR. Mortgage rates track deposit spreads, wholesale swap rates, and funding costs alongside the OCR. A falling OCR does not guarantee your rate falls by the same amount or at the same time.

-

Work with a mortgage adviser who monitors these conditions. Advisers help borrowers navigate both bank and non-bank lender criteria shaped by Reserve Bank policy shifts. They see rate changes and lender appetite shifts across the market in real time, which you simply cannot replicate by checking a comparison site once a month.

Pro Tip: Before you lock in a fixed rate, ask your adviser about current wholesale swap rate expectations. If the market is already pricing in Reserve Bank cuts, a shorter fixed term might land you at a lower rate when it expires than a longer term locked in today.

My take: what most people get wrong about the Reserve Bank

I have spent years watching clients confuse OCR announcements with the full picture of what the Reserve Bank does. In my experience, the liquidity management side of the house is chronically underappreciated, and that misunderstanding costs borrowers.

What I have found is that when the Reserve Bank strengthens its liquidity framework, as it is clearly signalling through its 2026 reviews, banks quietly lower their internal cost of funds. That translates into margin improvements that eventually reach borrowers, sometimes without any OCR move at all. The shift to proactive liquidity management is, in my view, one of the most significant but underreported developments in New Zealand lending right now.

I also think borrowers overestimate their own ability to time the market based on OCR news alone. The Reserve Bank’s influence on credit is layered. You could read every press release and still miss the funding conditions quietly tightening behind the scenes. That is why I always recommend working with an adviser who lives in this environment daily, not just someone who checks a rate table.

The Reserve Bank is not your lender. But it is the reason your lender behaves the way it does.

— Stuart

Work with advisers who track these changes

Reserve Bank policy shapes your mortgage options in ways you may not see directly. At Mortgagemanagers, our team tracks OCR decisions, liquidity framework changes, and lender responses across both bank and non-bank markets. We are based in Hobsonville and work with clients across Auckland, West Auckland, the North Shore, and throughout New Zealand remotely.

When conditions shift, whether through an OCR cut or a quiet change in funding conditions, we know which lenders are positioned to offer you genuine value. Our mortgage advisers act as personal shoppers for your home loan, comparing options across a wide lending panel so you do not have to do it alone. If you want personalised guidance on what current Reserve Bank settings mean for your borrowing capacity, speak with our team today.

FAQ

What is the Reserve Bank’s role in home lending?

The Reserve Bank of New Zealand does not lend directly to home buyers. It sets the OCR and manages liquidity facilities that influence how banks fund themselves, which in turn shapes the mortgage rates and credit conditions you access as a borrower.

How does the OCR affect my mortgage rate?

When the OCR falls, banks’ wholesale funding costs drop, and mortgage rates typically follow. The OCR was cut to 2.25% in late 2025, which pushed the average mortgage yield down to 5.4%, with further reductions expected through 2026.

What are liquidity facilities and do they affect my loan?

Liquidity facilities are tools the Reserve Bank uses to supply short-term funding to banks against collateral. They stabilise funding markets and reduce the chance that banks suddenly tighten lending criteria, even when the OCR itself does not change.

Do Reserve Bank policies affect non-bank lenders too?

Yes. Wider collateral eligibility and Committed Liquidity Facility access help non-bank lenders maintain stable funding, which supports competitive mortgage pricing and broadens your options beyond the major banks.

Should I watch Reserve Bank announcements when planning a home loan?

Absolutely. OCR meetings happen eight times a year and can shift fixed rates quickly. Liquidity framework reviews are less frequent but signal medium-term changes in credit conditions worth knowing about before you refix or apply for a new loan.