TL;DR:

- Getting a mortgage in New Zealand requires proof of income, a sufficient deposit, and a clean credit history. Lenders also evaluate your ability to meet the debt-to-income ratio limit and pass stress tests, with pre-approval offering a clear budget signal. Preparing detailed documents and understanding deposit options, like Kāinga Ora and KiwiSaver, helps buyers secure final approval and negotiate better terms.

Getting a mortgage loan in New Zealand requires proof of income, a sufficient deposit, a satisfactory credit history, and the ability to meet a lender’s serviceability tests. These are the four pillars every New Zealand lender assesses before approving a home loan. The Reserve Bank of New Zealand (RBNZ) also sets rules around how much you can borrow relative to your income. Kāinga Ora offers low-deposit pathways for eligible first home buyers. Understanding these requirements before you apply puts you firmly in control of the process, from pre-approval through to settlement.

What do you need to get a mortgage loan: documents and proof

Lenders need to verify your financial position before they will approve a cent. The documents you provide are their evidence, so accuracy and recency matter enormously.

Income proof is the starting point. Income verification differs depending on your employment status. PAYE employees typically provide recent payslips and an IRD earnings summary. Self-employed borrowers must supply two years of financial statements and tax returns. Lenders want to see consistency, not just a strong recent month.

Credit history is reviewed in detail. Your credit report shows missed payments, defaults, and recent credit enquiries. Errors on credit reports should be disputed before you apply, because even minor defaults can complicate approvals. Pull your credit report from a New Zealand credit bureau such as Centrix or Equifax NZ well before you lodge an application.

Deposit evidence is also required. You will need bank statements showing a genuine savings history, KiwiSaver statements if you plan to make a first home withdrawal, and a gift letter if any part of your deposit comes from family.

Living expenses receive close scrutiny. Banks assess living costs using either the Household Expenditure Measure (HEM) or your actual declared expenses, whichever is higher. They will comb through your bank statements looking at dining, subscriptions, and discretionary spending. Reducing unnecessary expenses in the three to six months before you apply makes a measurable difference.

Here is a summary of the core documents you need to prepare:

- Recent payslips (last 3 months) or two years of financial statements if self-employed

- IRD income summary or tax returns

- Three to six months of bank statements

- KiwiSaver statement and proof of savings

- Photo ID and proof of address

- Statements for all existing loans, credit cards, and buy-now-pay-later accounts

Pro Tip: Organise your documents into a single folder before you approach any lender. Incomplete applications cause delays and can signal disorganisation to a lender’s credit team.

How much deposit do you need and what are your options?

The deposit is often the biggest hurdle for first home buyers. Standard bank lending typically requires a 20% deposit for an owner-occupied home, though this varies by lender and borrower profile. On a $750,000 property, that is $150,000 upfront.

Low-deposit options do exist. Kāinga Ora’s First Home Loan allows eligible buyers to purchase with as little as 5% deposit, with the government underwriting the risk for participating lenders. Eligibility criteria apply, including income caps and property price limits, so check the current thresholds on the Kāinga Ora website before you plan around this pathway.

KiwiSaver is a powerful deposit tool. If you have been a KiwiSaver member for at least three years, you may be eligible to withdraw most of your balance for a first home purchase. Many buyers combine a KiwiSaver withdrawal with personal savings to reach the required deposit threshold.

| Deposit pathway | Minimum deposit | Key requirement |

|---|---|---|

| Standard bank lending | 20% | Strong credit and income proof |

| Kāinga Ora First Home Loan | 5% | Income and price cap eligibility |

| KiwiSaver first home withdrawal | Varies | 3+ years KiwiSaver membership |

| Family gift contribution | Varies | Signed gift letter required |

A deposit below 20% may trigger additional lender conditions or a higher interest rate. Some lenders also require Lenders Mortgage Insurance (LMI) for low-deposit loans, which adds to your upfront costs.

Pro Tip: If you are using KiwiSaver, apply for the withdrawal early. Processing can take several weeks, and delays at this stage can hold up your entire settlement.

What is mortgage pre-approval and why does it matter?

Mortgage pre-approval is a conditional loan offer from a lender, based on a preliminary assessment of your financial position. It is not a guarantee of final approval, but it is the clearest signal you can get that a lender is willing to lend to you at a certain amount.

Pre-approval typically takes 2–7 business days to process and remains valid for 90 days. During that window, you can make offers on properties with confidence. Sellers and real estate agents take pre-approved buyers more seriously, particularly in competitive markets like Auckland.

The pre-approval process involves the same core checks as a full application. The lender reviews your income, expenses, credit history, and deposit. What it does not include is a valuation of a specific property. That step comes later, once you have a property under contract.

Pre-approval is not a guarantee. Final approval depends on the lender’s valuation of the specific property and a formal loan application. If the bank values the property lower than your purchase price, you may face a funding gap. Understanding this risk before you sign anything is critical.

Key benefits of securing pre-approval before you start house hunting:

- Sets a realistic budget so you do not waste time on properties outside your range

- Strengthens your position when making an offer

- Identifies any credit or documentation issues early, giving you time to resolve them

- Speeds up the formal application once you find the right property

For a detailed walkthrough of the pre-approval process, Mortgagemanagers has a pre-approval checklist built specifically for New Zealand first home buyers.

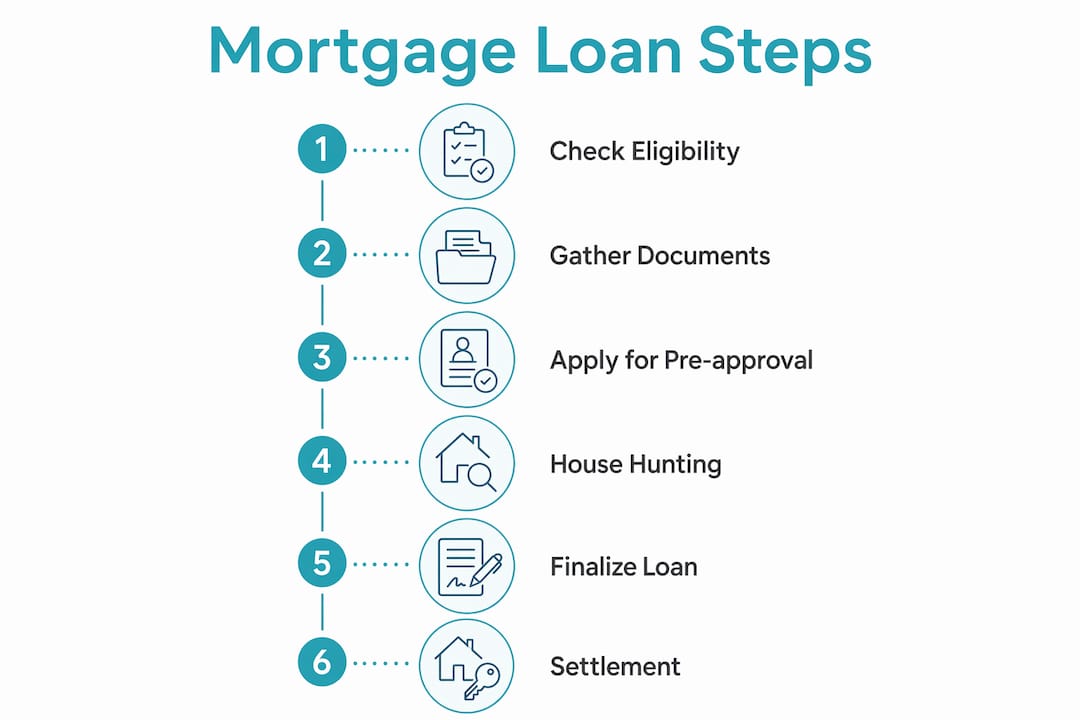

What steps follow pre-approval through to settlement?

Once you have pre-approval and a signed Sale and Purchase agreement, the formal mortgage application process begins. The whole process from pre-approval to settlement typically takes 30–60 days, though this depends on how quickly each party moves.

Here are the key steps in order:

- Sign the Sale and Purchase agreement with a finance condition clause included. This clause gives you the right to withdraw without penalty if your lender declines the loan or the property valuation falls short.

- Submit your formal mortgage application to your lender, including all updated documents and the signed agreement.

- Bank orders a property valuation. The lender appoints a registered valuer to confirm the property’s market value. If the valuation comes in lower than the purchase price, you will need to cover the gap or renegotiate.

- Receive formal loan approval. Once the valuation and application checks are complete, the lender issues unconditional approval.

- Finalise insurance. Most lenders require home and contents insurance to be in place before settlement. Life and income protection insurance is also worth arranging at this stage.

- Sign loan documents with your solicitor or conveyancer. A solicitor is legally required in New Zealand property transactions to prepare legal documents, register the mortgage, and manage settlement funds.

- Settlement day. Funds are transferred, the mortgage is registered, and keys are handed over.

The finance condition clause in your Sale and Purchase agreement is the single most important legal protection you have as a buyer. Without it, you risk losing your deposit if your lender declines the loan or the property valuation falls short of the purchase price. Never sign an unconditional offer unless you have formal loan approval in hand.

A common pitfall is letting the finance condition deadline lapse without confirming your loan status. Keep in close contact with your lender and adviser throughout this period.

How do lenders assess your ability to repay?

Lenders do not just look at your income in isolation. They run a full serviceability assessment to determine whether you can comfortably manage repayments now and if interest rates rise.

New Zealand banks apply a Debt-to-Income (DTI) ratio cap of 6x gross annual income for owner-occupier borrowers, a rule introduced by the RBNZ in july 2024. This means if your household earns $120,000 per year, the maximum you can borrow is $720,000 across all debts combined. Credit cards, personal loans, student loans, and buy-now-pay-later balances all count toward this figure.

Banks also stress test your repayments at interest rates of 7.5%–8.5%, well above current market rates. This confirms you could still service the loan if rates increase significantly. If you fail the stress test at your desired loan amount, the lender will reduce the amount they are willing to offer.

| Assessment factor | What lenders check | Why it matters |

|---|---|---|

| Gross income | Payslips, tax returns, IRD summary | Determines maximum DTI borrowing capacity |

| Living expenses | HEM vs. actual bank statement expenses | Reduces net income available for repayments |

| Existing debts | Loans, credit cards, BNPL balances | Counted in full against DTI limit |

| Stress test rate | 7.5%–8.5% floor rate | Confirms repayment capacity if rates rise |

| Credit score | Credit report from Centrix or Equifax NZ | Signals repayment reliability to lenders |

Your credit score is a significant factor. A strong score signals reliability. A score with missed payments or defaults signals risk, and lenders will either decline or apply stricter conditions. Checking your credit report and correcting any errors before you apply is one of the most effective things you can do to improve your approval chances.

Pro Tip: Pay down or close unused credit cards and buy-now-pay-later accounts before applying. Lenders count the full credit limit as a potential liability, not just the outstanding balance.

For guidance on how specialist property finance advisers approach complex borrower situations, the frameworks used internationally offer useful context on what lenders prioritise.

Key takeaways

Securing a mortgage loan in New Zealand requires verified income, a sufficient deposit, a clean credit history, and the ability to pass a lender’s DTI and stress test assessments.

| Point | Details |

|---|---|

| Documents matter | Prepare payslips, bank statements, IRD summaries, and KiwiSaver records before approaching any lender. |

| Deposit options exist | Standard lending requires 20%, but Kāinga Ora’s First Home Loan allows eligible buyers to start with 5%. |

| Pre-approval is conditional | Pre-approval takes 2–7 days and lasts 90 days, but final approval depends on property valuation. |

| DTI cap limits borrowing | The RBNZ caps owner-occupier borrowing at 6x gross annual income, including all existing debts. |

| Finance clause protects you | Always include a finance condition in your Sale and Purchase agreement to protect your deposit. |

Stuart’s take on preparing for a successful application

The single biggest mistake I see buyers make is treating pre-approval as the finish line. It is not. It is the starting gun. Final approval depends on the bank’s valuation of the specific property you choose, and a lower valuation can create a funding gap that catches buyers completely off guard. I have seen buyers fall in love with a property, sign an unconditional offer, and then scramble to find additional funds because the bank valued the home $40,000 below the purchase price. The finance condition clause in your Sale and Purchase agreement is your protection against exactly this scenario. Use it every time, without exception.

Financial organisation is the other area where buyers consistently underestimate the impact. Lenders are not just checking your income. They are reading your bank statements like a story about your financial habits. Three months of disciplined spending before you apply tells a very different story than three months of dining out and impulse purchases. You have more control over this than you realise.

Working with a mortgage adviser early in the process is genuinely worthwhile, particularly if your situation is not straightforward. Self-employed borrowers, buyers with existing debts, or those using non-standard deposit sources all benefit from having someone who knows each lender’s credit policy inside out. The mortgage approval process has real nuance, and a good adviser navigates that nuance on your behalf.

— Stuart

Working with Mortgagemanagers on your home loan

Knowing what you need is one thing. Pulling it all together and presenting it to the right lender is another.

Mortgagemanagers is a locally owned Auckland-based mortgage advisory business, and the team works with buyers across West Auckland, the North Shore, Hobsonville, and remotely throughout New Zealand. As personal shoppers for your home loan, the advisers know each lender’s criteria in detail and match your financial profile to the lender most likely to approve your application on the best available terms. Whether you are a first home buyer working through your deposit options or a self-employed borrower with a complex income structure, Mortgagemanagers can help you put your best application forward. Reach out early, before you start house hunting, and you will be in a far stronger position when the right property comes along.

FAQ

What credit score do you need for a mortgage in New Zealand?

New Zealand lenders do not publish a single minimum credit score, but a clean credit history with no missed payments or defaults significantly improves your approval chances. Dispute any errors on your credit report before applying.

Can you get a mortgage with less than 20% deposit in New Zealand?

Yes. Kāinga Ora’s First Home Loan allows eligible buyers to purchase with as little as 5% deposit, subject to income and property price caps. Some lenders also offer low-deposit lending outside this scheme, though conditions and rates differ.

How long does the mortgage loan application process take?

Pre-approval typically takes 2–7 business days. The full process from pre-approval to settlement generally takes 30–60 days, depending on how quickly documents are provided and valuations are completed.

What is the DTI limit for New Zealand home loans?

The RBNZ sets a Debt-to-Income ratio cap of 6x gross annual income for owner-occupier borrowers. All existing debts, including credit cards and personal loans, count toward this limit.

Do self-employed borrowers face different mortgage requirements?

Self-employed borrowers must provide two years of financial statements and tax returns instead of payslips. Lenders assess income based on net profit, so consistent earnings across both years strengthens the application considerably.