Finding a path to homeownership can feel out of reach for many australian buyers, especially when faced with the challenge of saving a large deposit. Recent figures show that nearly one in three australian first home buyers rely on low deposit loans to enter the market. Understanding how these loans work and what lenders expect allows you to approach the process with clarity and confidence. This guide breaks down the essential steps so you can move forward with your home buying journey.

Table of Contents

- Step 1: Assess Your Financial Eligibility For Low Deposit Loans

- Step 2: Gather The Required Documents And Deposit Funds

- Step 3: Compare Lenders Offering Low Deposit Mortgages In NZ

- Step 4: Apply For Your Chosen Low Deposit Home Loan

- Step 5: Verify Your Loan Approval And Next Home Buying Steps

Quick Summary

| Key Insight | Explanation |

|---|---|

| 1. Assess Your Financial Eligibility | Ensure stable income, low debt levels, and a sound credit history to qualify for low deposit loans. |

| 2. Organise Required Documentation | Gather payslips, tax returns, and bank statements to demonstrate financial stability and readiness. |

| 3. Compare Lenders Thoroughly | Create a spreadsheet to evaluate interest rates and fees from different lenders to find the best mortgage option. |

| 4. Prepare for Loan Application | Schedule a meeting with your lender, bringing all necessary documentation and being ready to address any questions. |

| 5. Verify Loan Approval Details | Thoroughly review loan terms and prepare necessary documentation for property settlement after approval. |

Step 1: Assess your financial eligibility for low deposit loans

Taking the first step towards securing a low deposit home loan requires a strategic approach to understanding your financial standing. According to Kāinga Ora, successfully navigating low deposit loan options hinges on demonstrating three key financial attributes: stable income, manageable debt levels, and a solid credit history.

To begin your assessment, gather comprehensive financial documentation that showcases your income reliability. This includes recent payslips, tax returns, and employment verification. Lenders will scrutinise your income stability to confirm you can consistently manage mortgage repayments. Calculate your debt-to-income ratio by totalling monthly debt obligations and dividing them by your gross monthly income. Ideally, this ratio should be under 40% to improve your loan approval prospects.

Your credit history serves as a financial report card that lenders will carefully examine. Obtain a free credit report to understand your current standing and address any potential red flags. Low Deposit Home Loans can be more challenging to secure, so ensuring a clean credit record is crucial. If you discover any historical credit issues, develop a strategic plan to improve your credit score before applying. This might involve paying down existing debts, resolving any outstanding defaults, and maintaining consistent bill payments.

A practical tip for success: consider working with a mortgage adviser who specialises in low deposit lending. They can provide personalised guidance tailored to your unique financial situation and help you prepare a compelling loan application. By understanding and proactively addressing your financial eligibility, you move one significant step closer to transforming your homeownership dreams into reality.

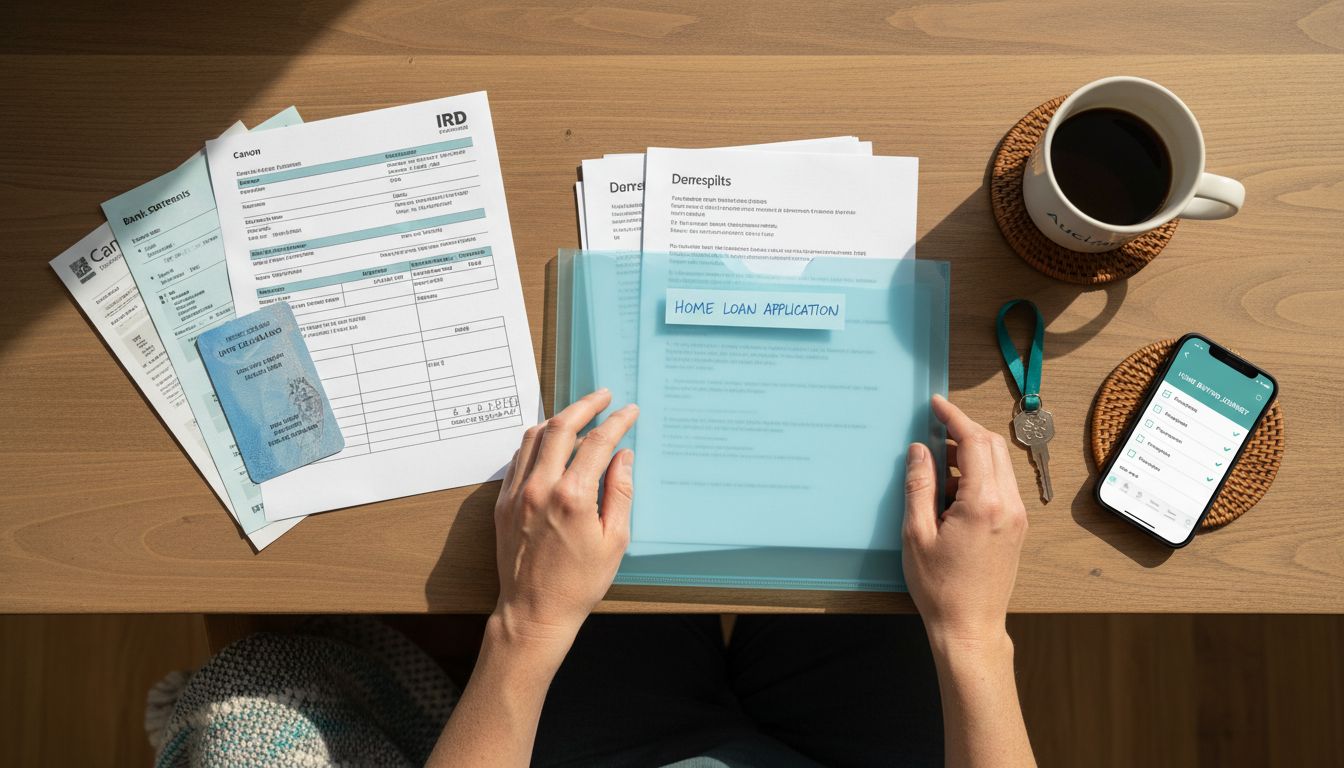

Step 2: Gather the required documents and deposit funds

Securing a low deposit home loan requires meticulous preparation and organisation of your financial documentation. This critical step involves collecting and preparing a comprehensive set of paperwork that demonstrates your financial readiness and ability to manage a mortgage.

Start by assembling a robust documentation package that typically includes proof of income, identification, and financial history. Collect recent payslips covering the past three to six months, providing a clear snapshot of your earning stability. Include your most recent tax returns, which offer lenders a comprehensive view of your annual income. Gather bank statements showing consistent savings patterns and your growing deposit fund. Prepare employment verification documents from your current employer, which should outline your job tenure, position, and salary details.

For your deposit funds, create a strategic savings plan that demonstrates financial discipline. Open a dedicated savings account and consistently contribute towards your home loan deposit. Lenders prefer to see genuine savings accumulated over time rather than lump sum deposits from gifts or one off windfalls. Getting a Home Loan with a 5% Deposit recommends maintaining a clear trail of your savings to enhance your loan application credibility.

A practical tip to streamline your document gathering process is to create a dedicated folder both digitally and physically. Scan and save digital copies of all important documents and keep original paperwork in a secure location. By being organised and proactive, you transform a potentially overwhelming task into a smooth, manageable journey towards homeownership.

Step 3: Compare lenders offering low deposit mortgages in NZ

Navigating the landscape of low deposit mortgage options requires a strategic and thorough approach to comparing different lenders and their unique offerings. According to The First Home Buyers Club, understanding the specific requirements and conditions set by various banks is crucial to finding the most suitable low deposit mortgage for your financial situation.

Begin your comparison by creating a comprehensive spreadsheet that tracks key lending criteria across multiple financial institutions. Focus on critical factors such as interest rates, low equity fees, maximum loan to value ratios, and specific lending conditions for low deposit loans. You Can Still Get A Home With A 10% Deposit suggests paying close attention to additional fees and charges that can significantly impact the overall cost of your mortgage. Some lenders may offer more competitive rates or more flexible terms for borrowers with slightly higher deposits or stronger financial profiles.

Consider scheduling initial consultations with mortgage advisers or bank representatives to gain deeper insights into their low deposit lending policies. Many lenders have nuanced approaches to assessing low deposit loan applications, and a direct conversation can reveal options not immediately apparent in standard marketing materials. Be prepared to discuss your specific financial circumstances, employment stability, and savings history. Some financial institutions may have special programs or more lenient criteria for first home buyers or specific professional categories.

A practical tip for successful lender comparison is to request formal loan estimates from multiple providers. This will give you a precise breakdown of potential costs, including interest rates, establishment fees, and any additional charges associated with low deposit lending. By methodically comparing these detailed estimates, you can make an informed decision that aligns with your financial goals and homeownership aspirations.

Step 4: Apply for your chosen low deposit home loan

Submitting your low deposit home loan application marks a pivotal moment in your homeownership journey. According to Trade Me Property, the application process involves careful preparation and strategic presentation of your financial profile to maximise your approval chances.

Begin by scheduling a comprehensive application meeting with your chosen lender. Bring all previously prepared documentation including proof of income, bank statements, identification, and detailed savings records. There Are Options For Low Deposit Home Loans recommends being transparent about your financial history and prepared to discuss any potential credit challenges. During this meeting, the lender will conduct a thorough assessment of your financial circumstances, evaluating your income stability, debt levels, credit history, and capacity to manage mortgage repayments.

Prepare yourself for potential additional requests for information or clarification. Lenders specialising in low deposit lending often require more detailed documentation to mitigate their risk. This might include extra employment verification, explanations of past financial events, or supplementary evidence of your financial reliability. Be responsive and prompt in addressing any queries to demonstrate your commitment and financial discipline.

A practical tip for success is to maintain financial stability during the application process. Avoid making significant financial changes like switching jobs, making large purchases, or opening new credit accounts. These actions can potentially complicate your loan application and raise red flags for lenders. By presenting a consistent and stable financial profile, you significantly improve your chances of securing your low deposit home loan.

Step 5: Verify your loan approval and next home buying steps

Receiving loan approval represents a significant milestone in your homeownership journey. According to Kāinga Ora, this stage requires careful attention to understanding your legal obligations and preparing for the final property settlement process.

Begin by thoroughly reviewing your loan approval documentation, paying close attention to all terms and conditions. Mortgage Approval Process Guide NZ Home Loans recommends carefully examining the approval letter to understand the specific conditions of your loan. Confirm the approved loan amount, interest rate, loan term, and any specific requirements or conditions attached to the approval. This is the time to seek clarification on any points you do not fully understand, ensuring you have a comprehensive grasp of your financial commitment.

Prepare for the property settlement by organising your financial and legal documentation. This includes arranging building insurance, which is typically a requirement for loan approval, and scheduling a comprehensive property valuation and inspection. You will need to coordinate with your solicitor or legal representative to manage the property transfer process. Be prepared to provide additional documentation and respond promptly to any requests from your lender or legal team to ensure a smooth settlement process.

A practical tip for success is to maintain open communication with your mortgage adviser and lender during this critical transition period. Keep all your financial documents easily accessible, avoid making any significant financial changes, and be ready to provide updated information if requested. By staying proactive and organised, you will navigate the final stages of your home loan approval with confidence and ease.

Take Control of Your Homeownership Journey with Expert Low Deposit Loan Support

Navigating the complexities of securing a low deposit home loan can feel overwhelming when you face challenges like understanding your financial eligibility, organising your documents, and comparing multiple lenders. This guide highlights how crucial it is to demonstrate a stable income, maintain a strong credit history, and carefully prepare your application to improve your chances of approval. If you are feeling uncertain about meeting these demands or want personalised advice tailored to your unique situation, expert guidance can make all the difference.

At Mortgage Managers, we specialise in assisting Kiwis just like you to unlock the path to homeownership with low deposit home loans. Based in Hobsonville, we provide strategic support across Auckland and nationally. Our professional mortgage advisers help you assess your financial readiness, organise your paperwork, and navigate lender comparisons to secure the best low deposit mortgage for your needs. Don’t wait while opportunities pass by — visit us today to take your first confident step towards owning your home with a low deposit home loan.

INFOGRAPHIC:infographic_content] You can also learn more about the advantages of [getting a home loan with a 5% deposit and explore the full range of low deposit home loan options. Make your dream real with trusted advice and support now.

Frequently Asked Questions

What are low deposit mortgages and how do they work?

Low deposit mortgages allow borrowers to purchase a home with a smaller upfront deposit, typically around 5% to 10% of the property’s value. To begin, assess your financial eligibility by reviewing your income, existing debts, and credit history, and gather necessary documentation for application.

How can I improve my chances of approval for a low deposit mortgage?

To enhance your approval chances, maintain a stable income, manage your debt-to-income ratio below 40%, and ensure your credit history is clean. Focus on paying down debts and keeping bills paid on time to strengthen your financial profile.

What documents do I need to apply for a low deposit home loan?

You will need to prepare proof of income such as payslips and tax returns, identification, and bank statements to confirm your savings history. Create a dedicated folder to keep these documents organised for your mortgage application.

How do I compare different lenders for low deposit mortgages?

To effectively compare lenders, create a spreadsheet that tracks interest rates, fees, and lending conditions across multiple financial institutions. Schedule consultations with lenders to discuss their specific low deposit lending policies and gather formal loan estimates for a thorough comparison.

What steps should I take after receiving loan approval for a low deposit mortgage?

After loan approval, review the terms and conditions carefully, organise necessary documentation for property settlement, and coordinate with your legal representative. Ensure you maintain financial stability by avoiding major changes that could impact your loan acceptance during this period.