More than 40 percent of New Zealanders carry multiple debts, yet many overlook solutions their Australian neighbours use to regain control. Juggling several high-interest bills each month can create constant stress and confusion, quickly impacting financial and mental health. Understanding how debt consolidation works empowers you with clear options to streamline your payments, potentially cut your interest, and build a stronger foundation for your family’s future.

Table of Contents

- Debt Consolidation Defined For New Zealanders

- Types Of Debt Consolidation Solutions In NZ

- How Debt Consolidation Works Step By Step

- Eligibility And Common Requirements In New Zealand

- Risks, Costs And Alternatives To Consider

Key Takeaways

| Point | Details |

|---|---|

| Understanding Debt Consolidation | Debt consolidation simplifies multiple debts into a single loan, often with a lower interest rate, thereby reducing financial complexity for New Zealanders. |

| Types of Solutions Available | Options such as personal loans, home loan refinancing, and community microfinance are available to help manage debts effectively. |

| Importance of Financial Assessment | Conduct a thorough financial review before consolidating to ensure it’s the right solution for your situation. |

| Evaluate Risks and Costs | Be mindful of potential pitfalls, including increased overall debt and additional fees, and consider alternative strategies as well. |

Debt Consolidation Defined For New Zealanders

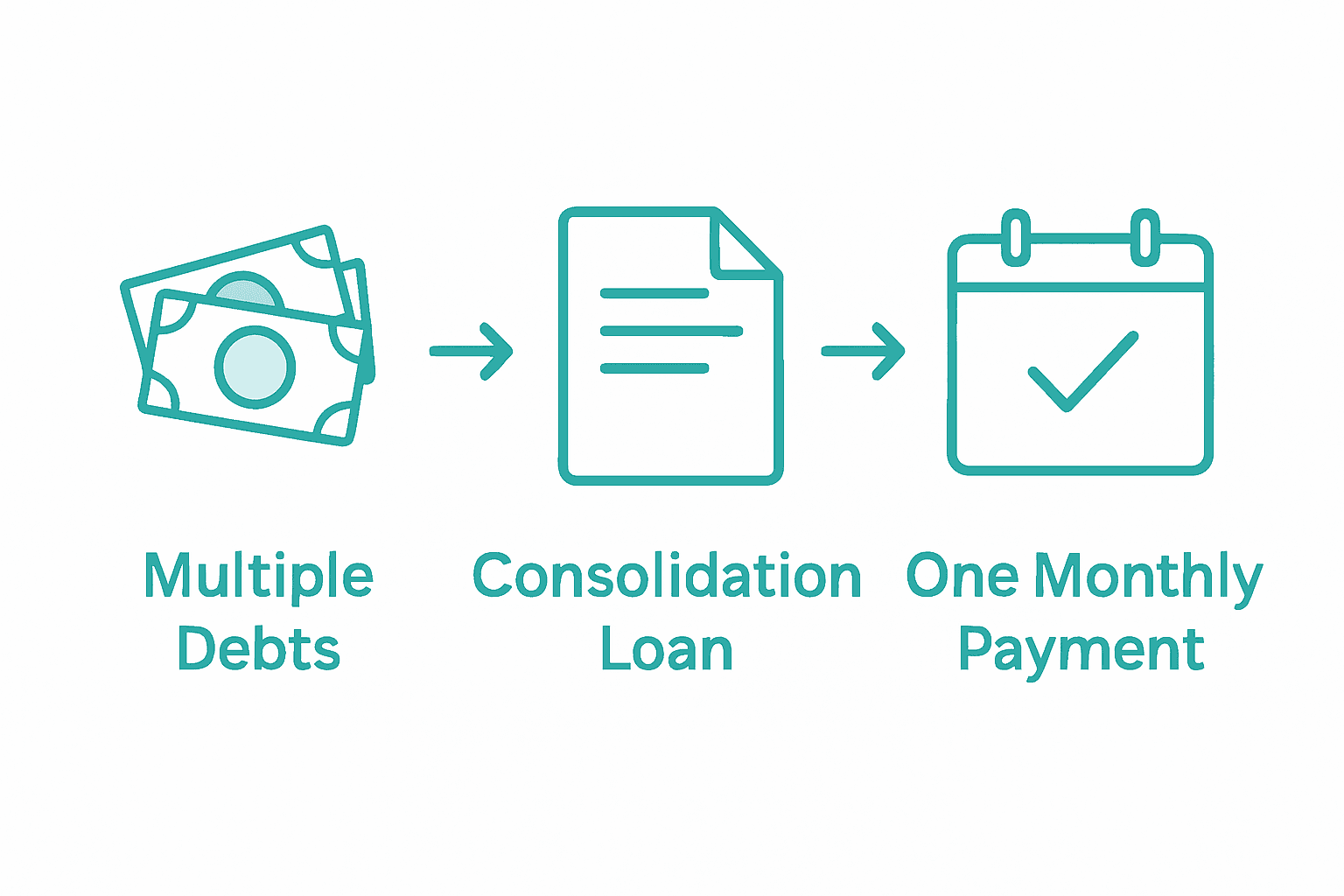

Debt consolidation is a powerful financial strategy that helps New Zealanders simplify and manage multiple debt obligations more effectively. At its core, debt consolidation involves combining several individual debts into a single, more manageable loan, typically with a lower overall interest rate. According to official insolvency guidelines, this process involves merging existing debts into one comprehensive loan, which can significantly streamline your financial management.

The primary goal of debt consolidation is to reduce the complexity and financial burden of managing multiple credit lines. Instead of tracking numerous payments with varying interest rates and due dates, you’ll have a single monthly payment. This approach can help Kiwis better understand their total debt, potentially lower their overall interest expenses, and create a more structured path towards financial recovery. For home owners and individuals struggling with multiple high-interest debts like credit cards, personal loans, or hire purchase agreements, debt consolidation offers a strategic pathway to regain financial control.

Typically, debt consolidation works by taking out a new loan that covers the total amount of your existing debts. This new loan usually comes with more favourable terms, such as a lower interest rate or a longer repayment period. The key advantages include simplified repayment schedules, potential reduction in total interest paid, and the psychological relief of having a single, more manageable debt obligation. However, it’s crucial to carefully assess your individual financial situation and understand that debt consolidation is not a one-size-fits-all solution.

Pro Tip: Financial Reset Strategy: Before consolidating your debts, conduct a comprehensive review of your current financial obligations, interest rates, and repayment capabilities. This preparatory step will help you determine whether debt consolidation is truly the most beneficial approach for your unique financial circumstances.

Types Of Debt Consolidation Solutions In NZ

New Zealand offers several strategic debt consolidation solutions designed to help individuals manage and restructure their financial obligations more effectively. Microfinance options from community organizations provide innovative pathways for those seeking to consolidate their debts, with specialized loans that address unique financial challenges.

The primary debt consolidation solutions in New Zealand typically include personal loans, home loan refinancing, and specialised microfinance options. Personal loans from banks and financial institutions allow borrowers to combine multiple high-interest debts into a single loan with potentially lower interest rates. Home loan refinancing is particularly attractive for homeowners, as it enables them to leverage their property’s equity to consolidate outstanding debts, often securing more favourable repayment terms. Personal loan debt consolidation strategies can be especially effective for managing credit card balances, hire purchase agreements, and other unsecured debts.

Community-based microfinance solutions represent a unique approach to debt consolidation in New Zealand. Organizations like Good Shepherd and Ngā Tāngata Microfinance offer specialized loans that help individuals restructure their financial obligations. These programs typically provide interest-free or low-interest loans specifically designed to help people consolidate harmful debts into more manageable repayment structures. Such solutions are particularly valuable for individuals who might not qualify for traditional bank loans or need more flexible financial support.

Here is a comparison of New Zealand’s main debt consolidation options:

| Solution Type | Typical Use Case | Interest Rate Range | Key Benefit |

|---|---|---|---|

| Personal Loan | Unsecured debts, credit cards | Moderate to high | Quick approval and access |

| Home Loan Refinancing | Homeowners with equity | Lower than personal loans | Lower rates, higher limits |

| Community Microfinance | Financial hardship, low incomes | Often interest-free or low | Flexible, supportive terms |

Pro Tip: Financial Navigation Strategy: Before selecting a debt consolidation solution, carefully compare the total cost of consolidation, including interest rates, fees, and repayment terms. Create a comprehensive spreadsheet comparing different options to identify the most cost-effective path for your specific financial situation.

How Debt Consolidation Works Step By Step

Debt consolidation is a strategic financial process that transforms multiple complex debt obligations into a single, more manageable financial solution. The debt consolidation process typically involves several critical steps designed to simplify your financial landscape and potentially reduce overall interest expenses.

The step-by-step debt consolidation journey begins with a comprehensive financial assessment. First, you’ll need to compile a detailed inventory of all existing debts, including credit card balances, personal loans, hire purchase agreements, and any other outstanding financial obligations. This initial stage requires gathering precise documentation, such as current loan statements, interest rates, and monthly payment requirements. Next, you’ll evaluate your total debt volume and assess your current financial capacity to determine the most suitable consolidation strategy.

Once you’ve completed your financial review, the next phase involves selecting an appropriate consolidation method. This might include applying for a personal consolidation loan, refinancing your home loan, or exploring specialised microfinance options. The chosen approach will depend on factors like your credit history, total debt amount, current income, and existing assets. During this stage, financial institutions will conduct a thorough assessment of your financial profile, potentially requiring documentation such as proof of income, identification, and a comprehensive breakdown of your existing debt portfolio.

Pro Tip: Documentation Preparation Strategy: Before initiating the debt consolidation process, create a comprehensive financial folder containing all relevant documents. Include recent bank statements, loan agreements, proof of income, and a detailed debt summary to streamline your application and demonstrate financial preparedness.

Eligibility And Common Requirements In New Zealand

Debt consolidation eligibility in New Zealand varies depending on the specific financial institution and consolidation method. Microfinance loan eligibility criteria typically require applicants to demonstrate financial need and a clear capacity to repay their proposed loan, ensuring responsible lending practices.

Most financial institutions in New Zealand assess several key factors when determining debt consolidation eligibility. Credit history plays a crucial role, with lenders examining your past financial behaviour, including credit score, payment consistency, and existing debt levels. Typically, applicants must be at least 18 years old, have a stable income source, and provide proof of regular employment or consistent earnings. Some lenders may also require a minimum annual income threshold, which can range from $30,000 to $50,000, depending on the specific consolidation product and the total debt volume.

The documentation requirements for debt consolidation are comprehensive and designed to provide lenders with a complete financial profile. Applicants will generally need to supply several key documents, including recent payslips, bank statements from the past three to six months, identification documents, current loan statements, and a detailed breakdown of existing financial obligations. For those seeking specialised microfinance options, additional criteria might include demonstrating financial hardship or a genuine need for debt restructuring. Lenders will carefully evaluate your debt-to-income ratio, existing credit commitments, and overall financial stability to determine your suitability for a consolidation loan.

The following table summarises common eligibility requirements for debt consolidation loans in New Zealand:

| Requirement | Why It Matters | Typical Expectation |

|---|---|---|

| Age | Legal contract responsibility | 18 years or older |

| Income Stability | Ensures repayment ability | Proof of steady income |

| Credit History | Measures risk to lender | Good to fair credit score |

| Documentation | Verifies financial situation | Payslips, bank and loan statements |

Pro Tip: Financial Documentation Strategy: Create a comprehensive financial portfolio before applying for debt consolidation, including organised copies of all financial documents, a detailed debt summary, and a clear explanation of your current financial situation to streamline the application process and improve your chances of approval.

Risks, Costs And Alternatives To Consider

Comprehensive debt solution reviews highlight the nuanced landscape of debt consolidation, revealing that while this strategy can offer significant financial relief, it’s not without potential pitfalls. Risks associated with debt consolidation include potential increases in overall debt if underlying spending behaviours remain unchanged, additional fees for loan establishment, and the possibility of extending your total repayment timeline.

The financial costs of debt consolidation extend beyond simple interest calculations. Borrowers must carefully evaluate establishment fees, potential early repayment penalties on existing loans, and the long-term interest implications of extending debt repayment periods. Some consolidation loans might appear attractive initially but could result in higher total interest payments over the loan’s lifetime. Debt counseling alternatives provide a critical counterpoint, offering strategies that address root financial challenges without necessarily creating new debt structures.

Alternatives to debt consolidation include targeted financial counselling, debt management plans, and more aggressive debt repayment strategies. For New Zealanders facing complex financial situations, options like negotiating directly with creditors, implementing strict budget controls, or exploring government-supported financial mentoring programmes can provide meaningful alternatives. Each approach carries unique advantages and potential drawbacks, making it essential to conduct a thorough personal financial assessment before committing to any single strategy.

Pro Tip: Financial Diagnostic Strategy: Before deciding on debt consolidation, conduct a comprehensive personal financial audit. Calculate your total current interest expenses, project potential consolidation loan costs, and objectively assess whether the proposed solution genuinely improves your financial position or merely redistributes your existing debt burden.

Take Control of Your Debt with Expert Guidance from Mortgage Managers

Struggling to manage multiple debts can feel overwhelming but debt consolidation offers a clearer path to financial freedom by combining debts into one manageable payment. If you are a Kiwi looking to simplify payments, reduce your interest expenses, or explore smart refinancing options, understanding how to start is crucial. At Mortgage Managers, we specialise in helping New Zealanders like you navigate solutions such as home loan refinancing and personal loans designed specifically for debt consolidation.

Don’t wait until financial pressure mounts. Visit Mortgage Managers today to speak with experienced mortgage advisers based in Auckland who can tailor a strategy that fits your unique situation. Discover more about debt consolidation home loan options and personal loan debt consolidation strategies so you can regain control and move confidently towards a debt-free future.

Frequently Asked Questions

What is debt consolidation?

Debt consolidation is the process of combining multiple debts into a single loan, typically at a lower interest rate, to simplify management and reduce overall financial burden.

What are the key benefits of debt consolidation for Kiwis?

The main benefits include simplified repayment schedules, potential lower interest rates, reduced monthly payments, and improved financial clarity.

How does debt consolidation impact my credit score?

Debt consolidation can have a positive or negative impact on your credit score, depending on how you manage your new loan. Timely payments may improve your score, while missed payments could harm it.

What types of debt can be consolidated?

Common types of debt that can be consolidated include credit card balances, personal loans, hire purchase agreements, and other high-interest unsecured debts.