More than 40 percent of australian households worry about managing debt each month. Facing multiple payments and rising interest charges can quickly become overwhelming. By gaining a clear picture of your current financial situation, comparing available debt consolidation options, and preparing accurate documents, you can take practical steps toward lasting financial stability. This guide shows you how to organise your finances and approach debt consolidation with confidence.

Table of Contents

- Stage 1: Assess Your Current Financial Situation

- Stage 2: Compare Debt Consolidation Options In Nz

- Stage 3: Gather Required Documentation And Details

- Stage 4: Apply For A Debt Consolidation Loan

- Stage 5: Confirm Approval And Finalise Your Consolidation

Quick Summary

| Key Takeaway | Explanation |

|---|---|

| 1. Assess your financial situation | Gather documentation of your debts and income to understand your current financial health. |

| 2. Explore debt consolidation options | Evaluate various consolidation strategies to find the best fit for your financial circumstances. |

| 3. Organise required documentation | Compile all necessary financial records to support your debt consolidation application effectively. |

| 4. Submit loan applications accurately | Carefully complete applications to improve your chances of loan approval and favourable terms. |

| 5. Review and confirm loan approval | Ensure all loan terms match your expectations before signing and settling existing debts. |

Stage 1: Assess Your Current Financial Situation

Assessing your current financial situation is the critical first step in successfully navigating debt consolidation in New Zealand. This foundational process provides a clear snapshot of your financial health, helping you understand exactly where you stand and what strategies will work best for your unique circumstances.

Start by gathering comprehensive documentation of your current financial landscape. Collect recent bank statements, credit card bills, loan agreements, and any outstanding debt records. Carefully list each debt with its corresponding balance, interest rate, and minimum monthly payment. Financial tracking becomes easier with a systematic approach to documenting your finances. The New Zealand Ministry of Justice recommends thorough documentation when assessing financial capacity, which means being meticulous and honest about every financial obligation.

Calculate your total monthly income after taxes and compare it against your total monthly expenses and debt payments. This comparison will reveal your debt-to-income ratio a crucial metric that lenders and financial advisers use to evaluate your financial health. If your debt payments consume more than 36% of your monthly income, it signals that debt consolidation might be a strategic next step to regain financial stability. Remember that understanding your current financial situation is not about judgment but about creating a clear roadmap towards financial freedom.

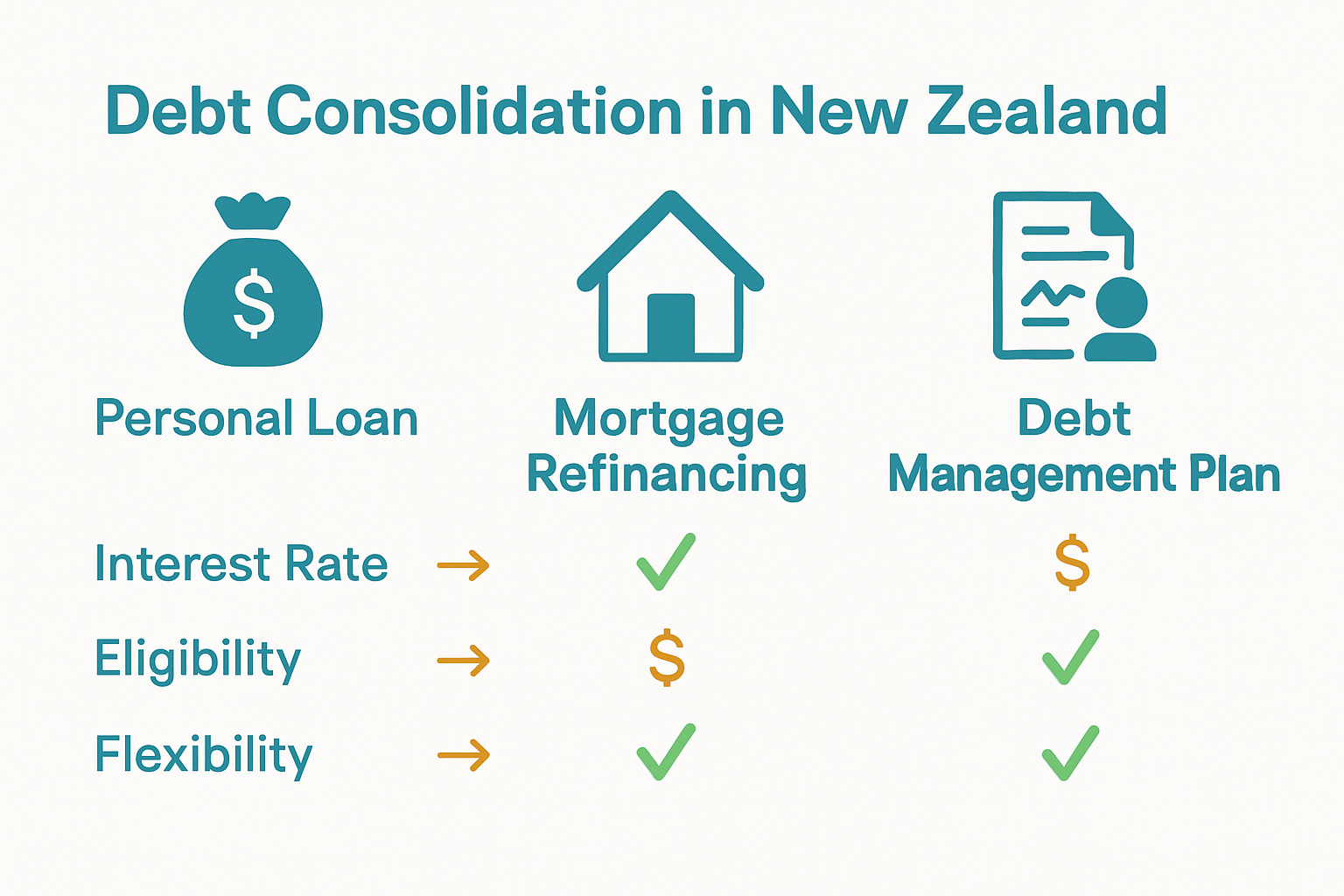

Stage 2: Compare Debt Consolidation Options in NZ

Comparing debt consolidation options is a strategic process that helps you select the most suitable financial solution for reducing and managing your overall debt. This critical stage involves carefully evaluating different approaches to consolidate multiple debts into a single more manageable payment structure.

Start by exploring various debt consolidation strategies available in New Zealand. Debt consolidation for home owners offers unique opportunities to leverage existing property equity. Consider personal loan options that can combine multiple high interest debts into one lower interest payment. Analyse key factors such as interest rates comparative fees loan terms and total repayment amounts. Some key options include balance transfer credit cards personal consolidation loans home loan top ups and debt management programs.

Carefully assess each option against your specific financial circumstances. Look beyond just the interest rate and examine establishment fees early repayment penalties and overall loan flexibility. Some consolidation strategies might seem attractive initially but could cost more in the long term. Your goal is finding a solution that reduces your total debt burden provides more manageable monthly payments and helps you progress towards financial stability without creating additional financial strain.

Stage 3: Gather Required Documentation and Details

Gathering the required documentation is a crucial step in your debt consolidation journey that ensures you are fully prepared to present your financial profile to potential lenders. This comprehensive process involves collecting and organising all necessary financial records that will support your debt consolidation application.

Start by compiling a comprehensive financial portfolio that includes recent payslips bank statements tax returns and identification documents. Calculating how much a debt consolidation loan will save you requires precise financial documentation. Gather statements for all existing debts including credit cards personal loans store cards and any other outstanding financial obligations. Ensure you have at least three months of recent financial records to demonstrate your income stability and current debt levels.

Prepare a detailed list of all your current debts including the creditor name outstanding balance interest rate and minimum monthly payment. This organised approach will not only streamline your debt consolidation application but also provide a clear snapshot of your financial situation. Lenders will appreciate your thoroughness and organisation which can potentially improve your chances of securing a favourable debt consolidation solution. Be transparent and accurate in your documentation to build trust with potential financial providers.

Stage 4: Apply for a Debt Consolidation Loan

Applying for a debt consolidation loan represents a strategic financial move to streamline your multiple debt obligations into a single manageable payment. This critical stage requires careful preparation and a methodical approach to increase your chances of loan approval and secure the most favourable terms.

Best personal loans for debt consolidation can significantly impact your financial recovery journey. Begin by submitting your loan application to selected lenders preferably those specialising in debt consolidation products. Prepare to provide comprehensive documentation including proof of income employment verification identification documents and a detailed list of current debts. Carefully complete each application with absolute accuracy ensuring all information matches your supporting documentation.

Each lender will conduct a credit assessment to evaluate your loan eligibility. Be prepared for potential credit checks and have a clear explanation ready about why you are seeking debt consolidation. Some lenders may request additional information or clarification about your financial circumstances. Maintain a professional and transparent approach throughout the application process. Your goal is to demonstrate financial responsibility and a genuine commitment to improving your financial health by consolidating your existing debts into a more structured and manageable repayment plan.

Stage 5: Confirm Approval and Finalise Your Consolidation

Confirming your debt consolidation loan approval marks a significant milestone in your financial recovery journey. This crucial stage involves carefully reviewing the final loan terms and ensuring everything aligns with your financial goals and expectations.

Mortgage brokers can help arrange sensible debt consolidation loans that match your specific financial needs. Carefully review the loan agreement paying close attention to interest rates repayment terms loan duration and any associated fees. Confirm that the new consolidated loan will indeed reduce your overall monthly payments and provide a clear path to financial freedom. Verify all documentation matches the terms you originally discussed with the lender and ensure you fully understand every aspect of the agreement before signing.

Once approved contact your previous creditors to settle the existing debts using the new consolidated loan funds. Request written confirmation that each debt has been fully paid and keep these documents for your personal records. This final step not only clears your previous obligations but also simplifies your financial landscape moving forward. Take a moment to celebrate this important step towards regaining control of your financial health and creating a more stable financial future.

Take Control of Your Debt with Expert Guidance from Mortgage Managers

Struggling to simplify multiple debts and lower your monthly repayments is a daunting challenge faced by many in New Zealand. The detailed debt consolidation process outlined in the article highlights how understanding your financial situation, comparing consolidation options and gathering proper documentation are vital steps towards regaining stability. This journey can feel overwhelming when doing it alone but Mortgage Managers can make it easier for you.

With years of experience as trusted Auckland mortgage advisers based in Hobsonville, Mortgage Managers specialise in arranging sensible debt consolidation loans tailored to your unique needs. We focus on finding solutions that reduce your repayments and keep your financial goals on track. Act now to benefit from personalised support and expert advice. Visit Mortgage Managers to start your debt consolidation journey with confidence and take the next step towards financial freedom. Learn more about how we help debt consolidation for home owners and discover the best personal loans for debt consolidation.

Frequently Asked Questions

What is the first step in the debt consolidation process?

Assessing your current financial situation is the first step in the debt consolidation process. Gather your recent bank statements, loan agreements, and debt records to create a clear snapshot of your financial health.

How do I compare different debt consolidation options?

To compare debt consolidation options, evaluate interest rates, fees, loan terms, and total repayment amounts. Make a list of available methods like personal loans or balance transfer credit cards, and assess them based on your specific financial situation.

What documentation do I need to apply for a debt consolidation loan?

When applying for a debt consolidation loan, prepare recent payslips, bank statements, tax returns, and a list of your current debts, including outstanding balances and interest rates. Compile this information to present a complete and organised financial profile to lenders.

How can I increase my chances of loan approval?

To increase your chances of loan approval, ensure your application is accurate and complete. Submit comprehensive documentation, maintain transparency about your financial situation, and explain clearly why you’re seeking debt consolidation.

What should I review before finalising my debt consolidation loan?

Before finalising your debt consolidation loan, review the agreement for interest rates, repayment terms, and any associated fees. Ensure that the new loan will reduce your monthly payments and confirm that everything matches the terms you discussed with the lender.

How do I settle my previous debts after loan approval?

After your loan is approved, contact your previous creditors to pay off the existing debts using the funds from your consolidated loan. Request written confirmation of debt settlements to keep for your records.