Most australian banks report that Hobsonville first home buyers are facing some of the highest average mortgage repayments in Auckland, stretching budgets tighter than ever. Feeling the pressure of steep monthly bills with little in savings can make home ownership seem out of reach. This guide shows you practical ways to review, restructure, and optimise your loan so you can reduce costs and find financial breathing room in your new Auckland home.

Table of Contents

- Step 1: Review Your Loan Terms And Options

- Step 2: Refinance With A Better Interest Rate

- Step 3: Extend Your Loan Repayment Period

- Step 4: Consolidate High-Interest Debts

- Step 5: Compare Results And Optimise Repayments

Quick Summary

| Key Insight | Explanation |

|---|---|

| 1. Review Mortgage Terms | Assess your loan agreement to uncover opportunities for reducing monthly repayments. |

| 2. Consider Refinancing | Look for better interest rates through refinancing to lower your ongoing mortgage costs. |

| 3. Extend Loan Repayment Period | Negotiating a longer term can substantially decrease monthly payments, aiding short-term cash flow. |

| 4. Consolidate High-Interest Debts | Combine debts into a lower-interest mortgage to simplify payments and reduce total interest. |

| 5. Compare and Optimise Payments | Use tools to compare strategies for reducing interest costs and optimising repayment frequency. |

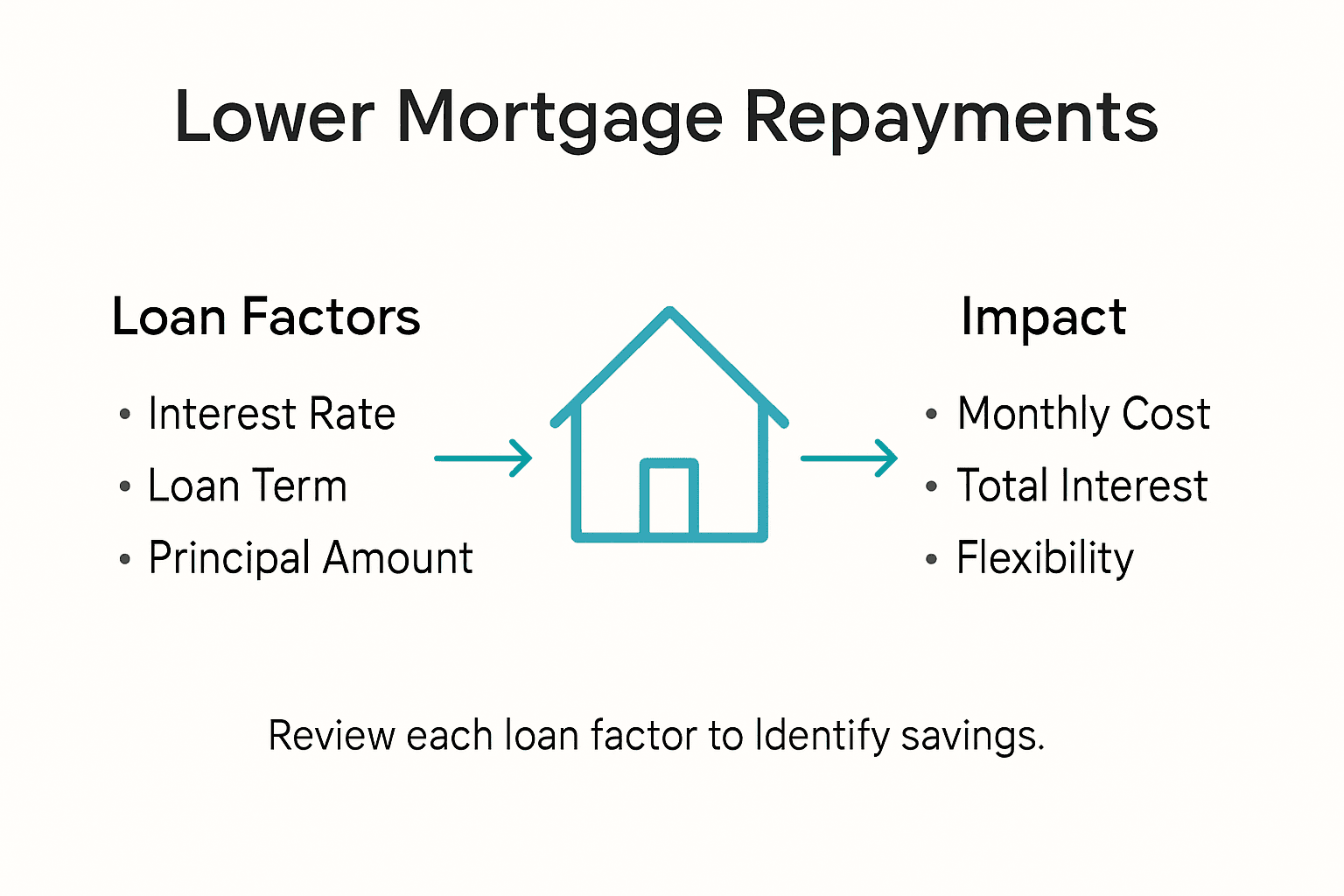

Step 1: Review your loan terms and options

Understanding and reviewing your current mortgage terms represents a critical first move towards potentially reducing your monthly repayments. Your home loan agreement includes multiple factors that directly impact what you pay each month, and strategically examining these can reveal significant savings opportunities.

Start by gathering all your existing loan documentation and carefully assessing key elements like your current interest rate, loan duration, and repayment structure. Pay close attention to whether you have a fixed or variable rate mortgage, as this will influence your options for potential adjustments. When reviewing your home loan now can help you identify immediate opportunities for reducing your financial burden. Look specifically at your loan term length your interest rate type and any potential refinancing possibilities that might lower your monthly commitment.

Your primary goal during this review is to determine whether your current mortgage still aligns with your financial situation and goals. Some homeowners might discover they qualify for lower interest rates or more favourable terms simply by conducting a thorough review and being prepared to negotiate with their lender. Consider consulting with a mortgage professional who can provide personalised insights into your specific financial landscape and potential savings strategies.

Use this table to identify which factors may influence your potential monthly savings when adjusting your mortgage:

| Loan Factor | Why It Matters | Typical Impact on Repayments |

|---|---|---|

| Interest rate | Determines cost of borrowing | Lower rate means smaller payments |

| Loan term length | Spreads payment over years | Longer term reduces payments |

| Repayment structure | Fixed vs variable, principal | Structure alters monthly outlay |

| Additional debts | Raises overall obligations | Consolidation may cut payments |

Top tip: Request a comprehensive loan statement from your lender and schedule a consultation with a mortgage adviser to explore your refinancing and restructuring options.

Step 2: Refinance with a better interest rate

Refinancing your mortgage offers a strategic pathway to significantly reduce your monthly repayments by securing a more competitive interest rate. This process involves replacing your existing home loan with a new one that has more favourable terms and potentially lower ongoing costs.

To begin refinancing, you will need to carefully compare current market rates and assess your eligibility. Explore comprehensive mortgage refinancing tips that can help you understand the nuances of this process. Start by checking your credit score and gathering all necessary financial documentation. Lenders will scrutinise your financial health when evaluating your refinancing application, so ensuring your credit profile is strong can help you secure the most attractive rates available. Look for lenders offering competitive rates and be prepared to negotiate based on your current financial standing and credit history.

Calculate the potential savings by comparing your current interest rate with available refinancing options. Factor in any associated fees such as application costs, valuation charges, and potential early exit penalties from your existing loan. While refinancing can offer substantial long term savings, it is crucial to perform a detailed cost benefit analysis to ensure the move makes financial sense for your specific circumstances.

Top tip: Request quotes from multiple lenders and use mortgage comparison tools to identify the most competitive refinancing options that align with your financial goals.

Step 3: Extend your loan repayment period

Extending your loan repayment period represents a strategic approach to reducing your monthly mortgage commitments by spreading your total loan amount over a longer timeframe. This method can provide immediate relief to your monthly budget by lowering the amount you need to pay each month.

To effectively extend your loan term, you will need to negotiate with your current lender or potentially refinance your mortgage. Understand the importance of mortgage repayments before making any significant changes. Typically, you can extend your loan term from the standard 25 or 30 year period to 35 or even 40 years. While this approach reduces your monthly payments, it is crucial to recognise that you will pay more in total interest over the life of the loan. Consider your long term financial goals and assess whether the short term reduction in monthly expenses aligns with your broader financial strategy.

Carefully calculate the potential savings and additional interest costs associated with extending your loan term. A longer loan term means smaller monthly payments but significantly more interest paid over the entire loan period. Speak with a mortgage adviser who can help you model different scenarios and understand the precise financial implications of extending your repayment period.

Top tip: Request a detailed amortisation schedule from your lender to understand exactly how loan term extensions impact your total interest payments.

Step 4: Consolidate high-interest debts

Consolidating high-interest debts can be a powerful strategy to reduce your overall financial burden and potentially lower your monthly mortgage repayments. By combining multiple high-interest debts into a single lower-interest loan, you can simplify your financial management and potentially save significant money over time.

Explore the key benefits of debt consolidation for Kiwi homeowners seeking financial relief. The process typically involves using your home loan as a vehicle to pay off existing high-interest debts like credit cards, personal loans, and other outstanding financial commitments. By rolling these debts into your mortgage, you can take advantage of lower mortgage interest rates and reduce the total amount of interest you are paying across multiple credit lines. This approach requires careful calculation and professional guidance to ensure you are genuinely improving your financial position.

When considering debt consolidation, conduct a thorough analysis of your current debt portfolio. Compare the interest rates of your existing debts against potential mortgage refinancing options. Calculate the total interest you are currently paying and contrast this with the projected interest under a consolidated loan structure. Be mindful that while consolidation can provide short term relief, it is crucial to address the underlying spending habits that may have contributed to accumulating high-interest debt.

Top tip: Consult a financial adviser who can provide personalised guidance on structuring your debt consolidation to maximise your long term financial health.

Step 5: Compare results and optimise repayments

Comparing and optimising your mortgage repayments is the final crucial step in reducing your overall financial burden. This process involves systematically reviewing and fine-tuning your loan strategy to ensure you are maximising your potential savings and financial efficiency.

Understand the key mortgage repayment strategies that can help you minimise your long term costs. Start by gathering detailed information about your current loan including interest rates, repayment frequencies, and total loan duration. Utilise online mortgage comparison tools to model different scenarios and understand how small changes in your repayment approach can significantly impact your overall financial outcome. Consider exploring options like fortnightly instead of monthly payments, which can help you pay down your principal faster and reduce total interest expenses.

Carefully analyse the potential savings from each strategy by comparing total interest paid, loan duration, and monthly cash flow implications. Pay close attention to the relationship between your repayment frequency, interest rate, and total loan cost. Some strategies might offer immediate monthly relief but could result in higher total interest over the loan term. The key is finding a balanced approach that provides short term financial breathing room while maintaining long term financial health.

Here’s a comparison of common strategies for reducing monthly mortgage repayments:

| Strategy | Immediate Monthly Impact | Long Term Effect | Key Consideration |

|---|---|---|---|

| Refinancing at lower rate | Substantially decreases | Reduces interest paid | May incur exit or setup fees |

| Extending repayment period | Moderately decreases | Increases total interest | Suits those needing cash flow relief |

| Debt consolidation into mortgage | Can noticeably decrease | Lowers combined interest costs | Risk of extending debt duration |

| Switching repayment frequency | Minimal, but more frequent | Can reduce overall loan term | Suited for consistent income flow |

Top tip: Create a detailed spreadsheet comparing different repayment scenarios to visualise potential savings and make an informed decision.

Take Control of Your Mortgage Repayments Today

Lowering your mortgage repayments as a first home buyer can feel overwhelming with so many factors to consider such as interest rates, loan terms, and debt consolidation. The challenge is real but you do not have to face it alone. Whether you want to refinance your mortgage, extend your repayment period, or consolidate high-interest debts, getting expert advice tailored to your unique situation is essential for making confident, informed decisions.

At Mortgage Managers, our Auckland-based mortgage advisers are dedicated to helping you unlock savings and optimise your repayments. We provide personalised strategies designed to reduce your monthly financial burden while aligning with your long-term goals. Don’t wait until your fixed term ends or payday feels tight. Visit Mortgage Managers now to access expert mortgage advice, explore how to restructure your home loan, and learn more about mortgage refinancing. Start your journey to smarter repayments and greater financial peace of mind today.

Frequently Asked Questions

How can I review my mortgage terms to lower repayments?

Start by gathering all your loan documentation and assessing key elements such as your current interest rate and loan duration. Look for opportunities to refinance or negotiate better terms with your lender and aim to complete this review within the next 30 days.

What are the benefits of refinancing my mortgage for first home buyers?

Refinancing can secure a lower interest rate, which directly reduces your monthly repayments. Compare current market rates and check your credit score; a strong score can help you qualify for better terms, potentially achieving savings of around 10% or more.

Is extending my loan repayment period a good option?

Extending your loan repayment period can lower your monthly payments by spreading the total cost over a longer term. However, keep in mind that this will increase the total interest paid over the life of the loan, so calculate the potential savings before proceeding with this option.

Can consolidating my high-interest debts really help reduce my monthly mortgage costs?

Yes, consolidating high-interest debts into your mortgage can lower your overall interest payments and simplify your financial management. Evaluate your current debts and consider this option if it can yield savings of at least 15% on your total monthly repayments.

What steps should I take to optimise my mortgage repayments?

To optimise your repayments, compare various strategies such as refinancing, extending your repayment period, or altering your repayment frequency. Create a detailed spreadsheet to model these scenarios and help visualise potential savings, aiming to make a decision within the next month.