TL;DR:

- Loan portability allows homeowners to transfer their existing mortgage to a new property, preserving their interest rate and loan terms while avoiding break fees. It simplifies the moving process and maintains lender relationships, especially beneficial when avoiding fixed-rate break costs or when market rates are favorable. However, eligibility and costs vary by lender, making early consultation and professional advice essential for an optimal move.

Most homeowners assume that selling their property means wiping the slate clean on their mortgage and starting from scratch. A new loan, a new application, new fees, and possibly a worse interest rate than the one you’ve worked hard to secure. But there’s a feature many Kiwi lenders offer that can change this picture entirely: loan portability. Understanding how it works, when to use it, and when to avoid it could save you thousands of dollars and a great deal of stress the next time you decide to move.

Table of Contents

- What is loan portability and why does it matter?

- Loan portability in practice: How does it work in New Zealand?

- Comparing loan portability and refinancing: Which is better?

- Potential pitfalls and practical advice for loan portability

- Our take: What most Kiwis miss about loan portability

- Discover your best loan options with expert guidance

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Loan portability defined | You can move your mortgage to a new home without starting a new loan if your lender allows. |

| Compare with refinancing | Portability can save time and fees, but refinancing may be better in some circumstances. |

| Know the pitfalls | Not all lenders offer portability, and there can be extra costs or eligibility hurdles. |

| Expert help matters | A mortgage adviser can explain your best options and help you avoid common mistakes. |

What is loan portability and why does it matter?

Loan portability is exactly what it sounds like. It’s the ability to transfer your existing mortgage from the property you’re selling to the new property you’re buying, keeping the same loan structure, the same interest rate, and the same lender relationship intact. Rather than repaying your loan in full and applying for a brand new one, you simply move it across to your next home.

This matters more than most people realise. If you’re mid-way through a fixed-rate term, breaking it early can trigger a significant early repayment charge. These fees, sometimes called break fees, are calculated based on the difference between your current rate and prevailing wholesale rates, and they can easily run into thousands of dollars. Portability lets you sidestep this cost entirely.

“Loan portability is a standard lender feature promoted by mortgage advisers and some banks as a way to give borrowers greater flexibility when they need to move.”

Here’s a quick summary of the core benefits loan portability offers:

- Avoid break fees: Keep your fixed rate intact and bypass potentially large early repayment costs.

- Retain your interest rate: If you locked in a competitive rate before rates climbed, you keep the advantage.

- Preserve your lender relationship: No need to rebuild your credit history or negotiate from scratch with a new lender.

- Simpler process: Compared to refinancing, portability can be faster and less administratively demanding.

- Continuity of loan terms: Your loan balance, repayment structure, and term stay consistent.

Loan portability is most relevant when you’re upgrading to a larger home, relocating within New Zealand, or downsizing while wanting to avoid the disruption of a new mortgage application. It’s a feature worth knowing about before you start searching for your next property, not after you’ve already signed a sale and purchase agreement. If you’re curious about lender options beyond the traditional banks, exploring bank alternatives for home loans can also open up new possibilities.

Loan portability in practice: How does it work in New Zealand?

Now that the basics are clear, it’s time to see how loan portability actually works in the New Zealand context. The process is relatively straightforward in principle, but the details matter enormously, and each lender has its own policies, timelines, and eligibility requirements.

Here’s a general step-by-step overview of how it works:

- Find your new property and make an offer. Once you have a conditional agreement in place, contact your lender as early as possible to discuss portability.

- Request portability formally. Ask your lender whether your loan qualifies for portability and request the application or transfer documentation.

- Lender assessment. Your lender will reassess your financial position, the value of the new property through a valuation, and whether the new security (your new home) is acceptable to them.

- Approval and transfer. If approved, the loan is transferred to the new property. Any shortfall in purchase price versus loan amount may need to be topped up with additional borrowing or cash.

- Settlement. Both the sale and purchase settle, ideally simultaneously, with your mortgage moving across cleanly to the new property title.

Timing is where many people come unstuck. If there’s a gap between when you sell your current home and when you settle on the new one, you may need bridging finance to cover that period. This is a short-term loan that fills the gap, and it adds cost and complexity to the transaction. Ensuring your settlement dates align as closely as possible is one of the most important practical steps you can take.

It’s also worth noting that mortgage lender types vary considerably in their portability policies. Major banks often have structured portability processes in place, while smaller lenders may handle things differently or not offer portability at all. Before relying on portability as part of your moving strategy, check your loan documents or speak directly with your lender.

Pro Tip: Engage your lender or mortgage adviser at least four to six weeks before your expected settlement date. This gives enough time for valuation, legal processing, and any surprises that arise during the approval stage. If you want to better understand how different loan products compare, comparing home loans is always a wise first step before committing to any direction.

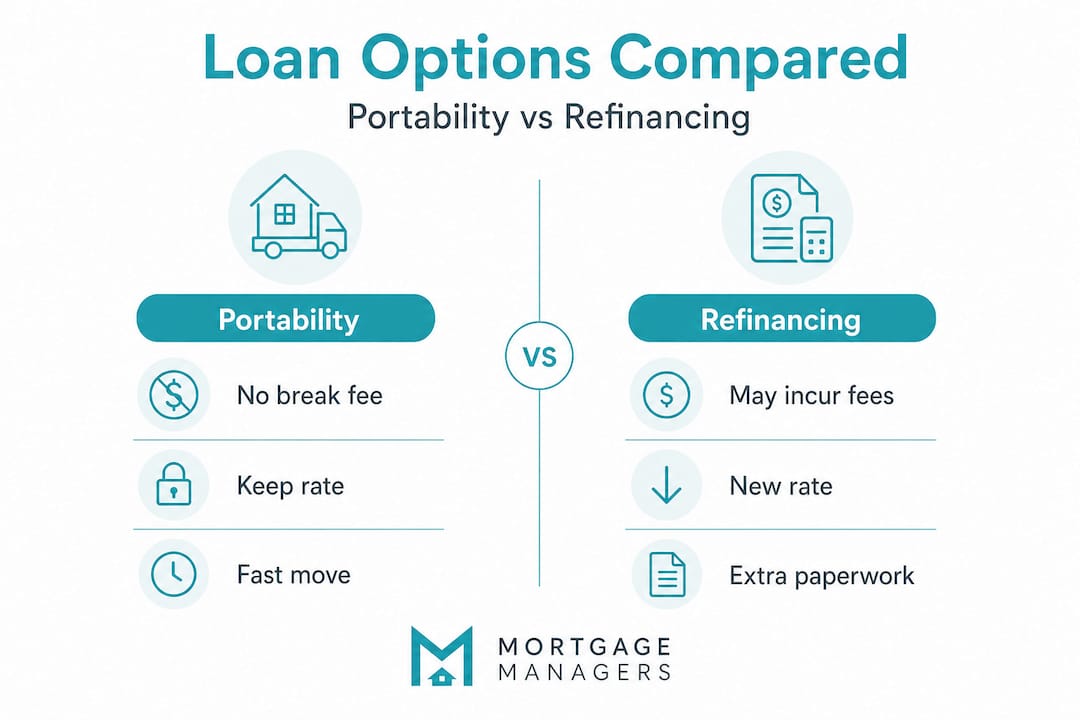

Comparing loan portability and refinancing: Which is better?

With an understanding of how portability works, it’s vital to compare it with the main alternative, refinancing, to determine the right move for your situation. Both options have genuine merits, and the best choice depends on your individual circumstances.

| Feature | Loan portability | Refinancing |

|---|---|---|

| Break fees | Usually avoided | Often applies if fixed rate |

| Interest rate | Stays the same | New rate negotiated |

| Application process | Simpler, same lender | Full application required |

| Flexibility | Limited to existing terms | Can restructure entirely |

| Time to settle | Can be faster | May take longer |

| Costs | Legal, valuation, admin fees | Legal, valuation, possible break fees |

| Lender relationship | Maintained | New lender relationship begins |

When does refinancing actually win? If your current interest rate is higher than what’s available in the market, or your financial situation has significantly improved, refinancing could land you a far better deal. It’s also worth considering if your current lender’s service or flexibility has been frustrating. A fresh start with a lender who better suits your needs can be a smart long-term move.

On the other hand, if you locked in a low fixed rate before recent increases, portability becomes genuinely valuable. Breaking a fixed rate to refinance could cost you far more in break fees than you’d save with a marginally lower rate elsewhere. It’s a maths exercise worth doing carefully, and refinancing a non-bank mortgage comes with its own unique set of considerations if you’re not with a traditional bank.

One common misconception is that portability is always the better choice simply because it sounds simpler. This standard lender feature has real advantages, but it can also lock you into a loan structure that no longer serves you well. If your fixed term is almost up, refinancing at that point could give you much better outcomes than porting.

Pro Tip: Always get written fee estimates from your lender before deciding between portability and refinancing. Ask specifically about break fees, valuation costs, legal fees, and any administration charges. Lay the numbers side by side before making any commitment.

Potential pitfalls and practical advice for loan portability

Even the best financial tools have catches, and loan portability is no exception. Knowing the common stumbling blocks before you encounter them is the difference between a smooth move and a stressful one.

Here are the most important pitfalls to watch for:

- Eligibility failures: Your lender will reassess your financial position when you apply for portability. If your income has dropped, your debts have increased, or the new property doesn’t meet the lender’s criteria, you may be declined.

- Valuation surprises: If the new property values lower than expected, your lender may not approve the full loan amount against it, leaving you with a funding gap.

- Bridging finance costs: When settlement dates don’t align, you may need bridging finance, which adds interest costs and complexity during the overlap period.

- Legal and administration fees: Portability is rarely free. Expect to pay for a new title search, property valuation, and lender administration charges even when you’re staying with the same bank.

- Not all lenders offer full portability: As noted in the Banking Supervision Handbook, there is no universal requirement for lenders to offer portability, and policies differ widely across the market.

Statistic callout: Loan portability is common among main banks in New Zealand but is not a guaranteed feature. Non-bank lenders, in particular, may have more restrictive policies or may not offer it at all.

When it comes to practical tips, there are several things that make a real difference. Start the conversation with your lender as early as possible, well before you’ve found a property. Confirm in writing what fees apply and what the eligibility criteria are. Keep your mortgage adviser and solicitor in close communication throughout the process, as they’ll often spot issues before they become problems.

If your portability application is declined, don’t panic. There are other options available. Exploring non-bank lenders in NZ may open up alternative financing structures, and in some cases, peer-to-peer lending or other creative approaches can bridge the gap. The key is having a knowledgeable adviser on your side who knows the full landscape.

Our take: What most Kiwis miss about loan portability

Here’s the honest truth, drawn from years of helping New Zealand homeowners navigate property moves: most people who approach us about loan portability have already made an assumption that it will work for them. They’ve heard it’s a great way to save on break fees, and they’ve decided that’s the end of the story.

But the devil is firmly in the detail. We’ve seen clients who were convinced portability was their best option, only to discover their fixed rate was expiring within weeks anyway. In those cases, the smarter move was to let the rate roll over and then refinance freely, without the constraints of an existing loan structure. Portability, in those situations, would have saved them nothing and limited their flexibility unnecessarily.

We’ve also seen the opposite: clients who didn’t know portability was an option and paid tens of thousands in break fees unnecessarily because they assumed they had no choice. Both scenarios are avoidable with the right advice at the right time.

The conventional wisdom that portability is a straightforward win oversimplifies a genuinely nuanced decision. Market conditions change, your financial profile changes, and the property you’re buying may not be what your lender considers ideal security. Simultaneous settlements are harder to coordinate than most people expect, and the costs involved in bridging can quietly erode the savings you hoped to make.

This is precisely why use mortgage brokers is such a relevant question for anyone in this position. A good broker doesn’t just help you apply for things. They read the fine print, model the numbers across multiple scenarios, and tell you when the conventional approach is actually going to cost you more. That kind of insight is genuinely difficult to replicate on your own, especially when you’re also dealing with the emotional and logistical demands of moving house.

Discover your best loan options with expert guidance

Navigating loan portability doesn’t have to feel like solving a puzzle on your own. Whether you’re upgrading, downsizing, or relocating, the right advice can make the difference between a seamless move and a costly one.

At Mortgage Managers, we work with Kiwis across Auckland and throughout New Zealand to make sense of exactly these kinds of decisions. Our team understands the nuances of different lenders’ portability policies, the timing challenges of simultaneous settlements, and how to structure deals that genuinely work in your favour. If you’re ready to talk through your options, our Auckland mortgage brokers are here to help. For truly tailored support, personalised mortgage advice from our team can map out the smartest path forward for your specific situation. Reach out today and take the guesswork out of your next move.

Frequently asked questions

Do all New Zealand lenders offer loan portability?

Loan portability is common among main banks but not universal. Some lenders, particularly non-bank providers, do not offer it or have more restrictive policies, so always check your loan documents first.

Does loan portability mean my repayments or interest rate stay the same?

In most cases your existing interest rate and loan term carry across to the new property, but if the new home’s value or your financial situation has changed, your lender’s assessment may result in adjustments to the loan structure.

What fees should I expect with loan portability?

You can generally expect legal fees, a new property valuation cost, and lender administration charges. These are typically lower than the break fees you’d face by exiting a fixed-rate loan early, but they are not zero.

Is loan portability available if I use a non-bank lender?

Some non-bank lenders do offer portability, but it is less common than with major banks. Always check the specific policy details, as availability and conditions vary across lender types significantly.