Over 60 percent of New Zealand homebuyers now turn to mortgage brokers for expert guidance rather than going directly to a bank. With complex loan rules and shifting markets, finding the right path to homeownership can feel daunting, especially for australian residents or anyone unfamiliar with New Zealand’s processes. Discover how mortgage brokers offer tailored advice, better loan access, and practical solutions for Australians seeking a smooth path through New Zealand’s property finance landscape.

Table of Contents

- What Mortgage Brokers Do In New Zealand

- How Mortgage Brokers Secure Better Rates

- Support For Bad Credit And Low Deposit Loans

- Comparing Brokers To Direct Lenders In NZ

- Key Risks, Costs And Legal Obligations

Key Takeaways

| Point | Details |

|---|---|

| Role of Mortgage Brokers | Mortgage brokers in New Zealand guide homebuyers through the loan acquisition process, assessing financial situations to secure optimal financing solutions. |

| Securing Competitive Rates | Brokers leverage their market knowledge and negotiation skills to access better home loan rates than individual borrowers can typically obtain. |

| Support for Challenging Financial Situations | They assist clients with bad credit or low deposits by exploring alternative funding options not offered by traditional banks. |

| Regulatory Compliance and Risks | Mortgage brokers must adhere to strict professional standards and legal obligations, ensuring transparent communication and ethical conduct. |

What Mortgage Brokers Do In New Zealand

Mortgage brokers serve as crucial financial intermediaries in New Zealand, specialising in guiding homebuyers through complex loan acquisition processes. These professionals research mortgage options and assess financial situations to help clients secure optimal home financing strategies.

Their core responsibilities involve comprehensive financial matchmaking. Mortgage brokers meticulously analyse a client’s financial profile, investigating lending possibilities across multiple banks and financial institutions. They compare interest rates, loan terms, and eligibility criteria to recommend the most suitable home loan packages. By leveraging extensive professional networks and deep market knowledge, these experts can often access loan options that individual borrowers might not discover independently.

A typical mortgage broker’s workflow encompasses several critical steps. They evaluate borrowing capacity, compile necessary documentation, and facilitate loan applications while maintaining direct communication with banks, conveyancers, and other relevant financial professionals. Their strategic approach includes:

- Conducting thorough financial assessments

- Researching competitive loan products

- Negotiating favourable terms on behalf of clients

- Providing impartial financial advice

- Streamlining complex application processes

Ultimately, mortgage brokers in New Zealand transform what could be an overwhelming financial journey into a structured, manageable experience for homebuyers seeking their ideal property financing solution.

How Mortgage Brokers Secure Better Rates

Mortgage brokers leverage sophisticated strategies to secure more competitive home loan rates, acting as strategic financial negotiators for their clients. Their deep understanding of the lending landscape enables them to navigate complex banking relationships and uncover advantageous rate opportunities.

These financial professionals possess unique insights into lender practices that most individual borrowers cannot access. By maintaining comprehensive networks across multiple banks and financial institutions, mortgage brokers can compare and contrast loan packages, identifying nuanced rate variations that could potentially save homebuyers significant amounts over their loan’s lifetime. Their negotiation skills and market knowledge allow them to present borrowers’ financial profiles in the most compelling manner, increasing the likelihood of securing more favourable interest rates.

The rate-securing process involves several strategic approaches:

- Comprehensive market analysis of current lending rates

- Detailed assessment of individual borrower financial profiles

- Strategic presentation of borrower credentials to multiple lenders

- Negotiation of competitive interest rates and loan terms

- Ongoing monitoring of potential refinancing opportunities

Ultimately, mortgage brokers function as financial advocates, utilising their expertise to unlock more attractive home loan rates that might remain hidden to individual borrowers navigating the complex lending landscape independently.

Support For Bad Credit And Low Deposit Loans

Mortgage brokers play a critical role in supporting borrowers with challenging financial backgrounds, particularly those with bad credit or low deposit situations. They help clients structure complex loan applications and explore alternative funding options that traditional banks might typically reject.

For individuals with less-than-perfect credit histories, mortgage brokers become invaluable navigators through the complex lending landscape. These financial professionals understand that a low credit score or minimal savings doesn’t necessarily disqualify someone from homeownership. By leveraging extensive networks of non-bank lenders and specialist financial institutions, brokers can identify specialised loan products tailored to unique financial circumstances.

The support process for bad credit and low deposit borrowers typically involves several strategic approaches:

- Comprehensive credit history assessment

- Identifying specialist non-bank lending options

- Developing personalised credit improvement strategies

- Negotiating flexible loan terms

- Connecting borrowers with alternative financial solutions

Ultimately, mortgage brokers transform seemingly insurmountable financial barriers into realistic pathways to homeownership, providing hope and practical solutions for borrowers who might otherwise be excluded from traditional lending markets.

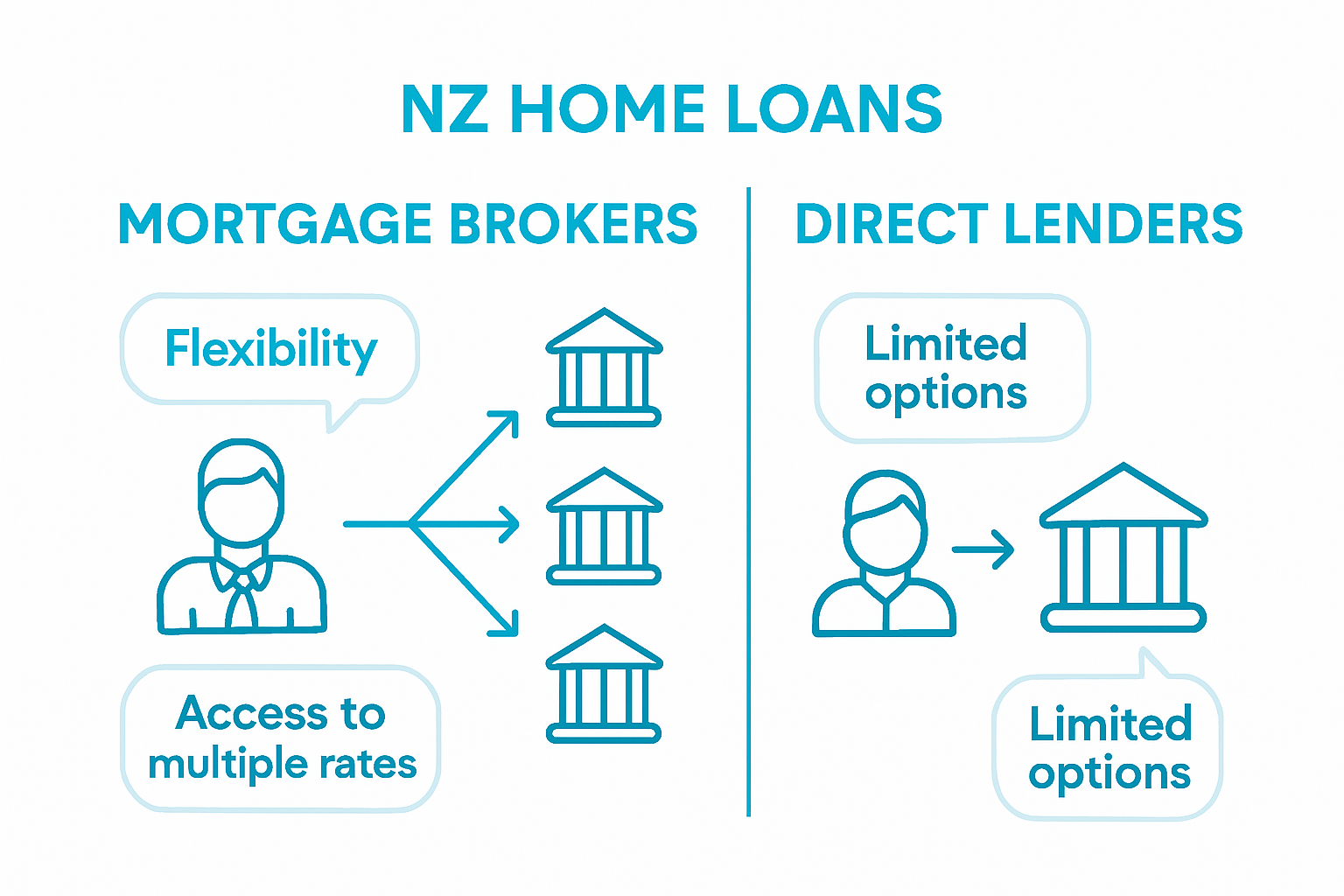

Comparing Brokers To Direct Lenders In NZ

Mortgage brokers and direct lenders represent two distinctly different approaches to securing home loans in New Zealand. Brokers enhance market competition by helping consumers shop around and understand various lending options, offering a more comprehensive and flexible alternative to traditional bank-direct approaches.

Unlike direct lenders who represent a single financial institution’s products, mortgage brokers act as independent financial intermediaries. They can access a wide range of loan products from multiple lenders, including banks, credit unions, and non-bank financial institutions. This approach provides borrowers with a more diverse selection of home loan options, potentially uncovering more competitive interest rates and more suitable loan structures that might not be available through a single direct lender.

Key differences between mortgage brokers and direct lenders include:

- Range of product offerings

- Breadth of financial network

- Personalised financial advice

- Flexibility in loan negotiations

- Cost of service

Ultimately, mortgage brokers provide a more nuanced, personalised approach to home lending, offering borrowers greater flexibility and access to a broader spectrum of financial solutions compared to the more limited, product-specific offerings of direct lenders.

Key Risks, Costs And Legal Obligations

Mortgage brokers operate within a complex regulatory landscape that requires strict adherence to professional standards and legal requirements. To practice legally in New Zealand, mortgage brokers must be registered as financial advisers under a Financial Advice Provider license, which involves comprehensive compliance and professional accountability.

The financial risks and legal obligations for mortgage brokers are multifaceted, extending beyond simple loan placement. Brokers must maintain professional indemnity insurance, comply with strict disclosure requirements, and ensure transparent communication about potential conflicts of interest. This includes providing clear, impartial advice that prioritises the client’s best financial interests, with potential legal consequences for misleading or inappropriate recommendations.

Key risks and obligations for mortgage brokers include:

- Maintaining professional registration and licensing

- Adhering to Financial Advice Provider regulations

- Providing transparent and honest financial advice

- Managing potential conflicts of interest

- Protecting client confidentiality

- Maintaining comprehensive professional documentation

- Participating in dispute resolution schemes

While mortgage brokers offer significant value to borrowers, they must carefully navigate a complex regulatory environment that demands ongoing professional diligence, ethical conduct, and a commitment to maintaining the highest standards of financial advice and client protection.

Discover How Mortgage Managers Unlock Better Home Loans for You

Navigating home financing in New Zealand can feel overwhelming especially when dealing with bad credit or low deposits or simply trying to secure better interest rates. The article highlights the crucial role mortgage brokers play in simplifying complex loan options and negotiating favourable terms. If you want personalised financial advice and access to a wide range of lenders beyond just one bank then Mortgage Managers is your ideal partner. We are a locally owned team of Auckland mortgage advisers based in Hobsonville ready to support you wherever you are in West Auckland the North Shore or across New Zealand.

Take control of your home loan journey now by working with experts who understand your challenges and goals deeply. Learn more about how we provide tailored solutions and competitive rates by visiting Mortgage Managers today. Find out why so many New Zealanders choose to use mortgage brokers to unlock better options and get started on securing your ideal home loan before the moment passes.

Frequently Asked Questions

What are the benefits of using a mortgage broker?

Using a mortgage broker provides access to a wider range of loan products and competitive interest rates. They help assess your financial profile and negotiate with lenders on your behalf, simplifying the home loan process and saving time.

How do mortgage brokers secure better home loan rates?

Mortgage brokers leverage their relationships with various lenders to identify advantageous rate opportunities. Their deep understanding of the market and negotiation skills allow them to present your financial profile compellingly, increasing the likelihood of obtaining better rates.

Can mortgage brokers assist with bad credit or low deposit loans?

Yes, mortgage brokers specialise in helping clients with bad credit or low deposits. They understand that such financial situations do not automatically disqualify borrowers and can connect you with alternative lenders and specialised loan products tailored to your needs.

How do mortgage brokers differ from direct lenders?

Mortgage brokers act as independent intermediaries, providing access to a larger range of loan products from multiple lenders. Unlike direct lenders, who offer products from a single institution, brokers help you compare options, negotiate terms, and provide personalised financial advice.

Recommended

- Mortgage Broker NZ: Complete Guide for Home Buyers

- Role of Mortgage Brokers NZ – What Home Buyers Gain

- People Use New Zealand Mortgage Brokers More Than Ever Before

- How to Choose a Mortgage Broker in NZ for the Best Home Loan – Mortgage Managers

- 7 Essential Tips for First Home Buyers in Melbourne – Onyx Removals