TL;DR:

- A table loan is the most common type of mortgage in New Zealand, offering fixed regular repayments that gradually pay off the principal and interest over 25 to 30 years. It provides certainty, predictable payments, and steady equity growth, making it ideal for first-time buyers. While other loan types exist, table loans remain popular because of their transparency and simplicity, supported by most lenders and recommended by industry professionals.

If you’ve started researching home loans in New Zealand, you’ve almost certainly come across the term “table loan” without anyone explaining what it actually means. Most lenders offer it as their standard product, most mortgage advisers recommend it, and yet many first-time buyers sign up without fully understanding how their repayments are structured or why they’re paying the amounts they are. This guide is your clear, no-nonsense walkthrough of table loans: what they are, how they work, how they compare to other options, and how to make them work harder for you.

Table of Contents

- What is a table loan?

- How table loans work: Repayments and structure

- Table loan vs other NZ home loan types

- Costs, fees and what to expect

- Tips for first-time buyers using a table loan

- Why most Kiwi first-home buyers are better off with table loans

- Get expert help choosing your table loan

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Standard mortgage type | Table loans are the main home loan structure for NZ first-home buyers, offering regular fixed repayments. |

| Stable repayments | Your payment amounts are predictable, making it easier to budget throughout your loan term. |

| Principal and interest | Every repayment gradually reduces your debt and interest, not just the interest alone. |

| Flexible options | You can often mix fixed and floating rates, and lenders may negotiate fees and payment structures. |

| Expert help available | Working with a mortgage adviser ensures you find the ideal loan for your situation and avoid costly mistakes. |

What is a table loan?

Think of a table loan as the reliable workhorse of New Zealand mortgages. It’s not flashy, and it doesn’t come with lots of bells and whistles, but it does exactly what most Kiwi homebuyers need it to do: it gives you predictable, regular repayments that steadily pay down what you owe over a set period of time.

A table loan is the most common type of home loan in New Zealand, featuring fixed regular repayments (weekly, fortnightly, or monthly) over a term of 25 to 30 years that cover both principal and interest.

In practical terms, this means you agree to repay a specific amount at the same regular interval for the life of the loan, and by the end of that term, your mortgage is fully paid off. No surprises. No large lump-sum payments lurking at the end.

Here are the core characteristics of a table loan at a glance:

- Fixed repayment amount: Your scheduled payment stays the same unless you change your interest rate, loan term, or make extra contributions.

- Regular payment frequency: You can choose weekly, fortnightly, or monthly repayments, depending on what suits your cashflow.

- Both principal and interest: Every repayment includes some of the amount you originally borrowed (the principal) plus the interest charged on that balance.

- Standard loan term: Usually 25 to 30 years for a home loan in New Zealand.

- Gradual ownership building: Each payment brings you slightly closer to owning your home outright.

For first-time buyers, understanding mortgage features for first-time buyers can make the process feel a lot less overwhelming. The table loan is the natural starting point for that understanding.

How table loans work: Repayments and structure

With the basics covered, let’s dig into how these loans function day-to-day when you’re making repayments.

The key concept here is amortisation, which is simply the process of spreading your loan repayments out over time so that the balance reduces gradually to zero. This is where table loans get their name. Your repayments are calculated using an amortisation table that maps out each payment across the life of the loan, showing exactly how much goes to interest and how much reduces the principal.

Here’s the part that surprises many first-time buyers: in the early years, the vast majority of each repayment goes towards interest, not the principal. As your balance decreases over time, the interest portion shrinks and the principal portion grows. Your repayment amount stays the same throughout, but the split between interest and principal shifts significantly.

To make this concrete, here’s an illustrative example based on a $600,000 loan at 6.5% interest over 30 years:

| Year | Monthly repayment | Interest portion | Principal portion | Remaining balance |

|---|---|---|---|---|

| Year 1 | $3,792 | $3,250 | $542 | $593,500 |

| Year 5 | $3,792 | $3,050 | $742 | $558,000 |

| Year 15 | $3,792 | $2,300 | $1,492 | $418,000 |

| Year 25 | $3,792 | $950 | $2,842 | $162,000 |

| Year 30 | $3,792 | $80 | $3,712 | $0 |

Note: Figures are illustrative and rounded for clarity. Always check with your lender or use a mortgage calculator for precise numbers.

As you can see, the shift is dramatic. In year one, only a small fraction chips away at what you actually owe. But by year 25, the bulk of each payment is reducing your principal. This is why how NZ home loans work and understanding loan terms matters so much for making smart decisions early on.

Pro Tip: Making even small extra repayments in the first five years of your loan can save you tens of thousands of dollars in interest over the life of your mortgage. Because early repayments directly reduce your principal, the interest savings compound significantly over time. Even an extra $50 per week can make a meaningful difference.

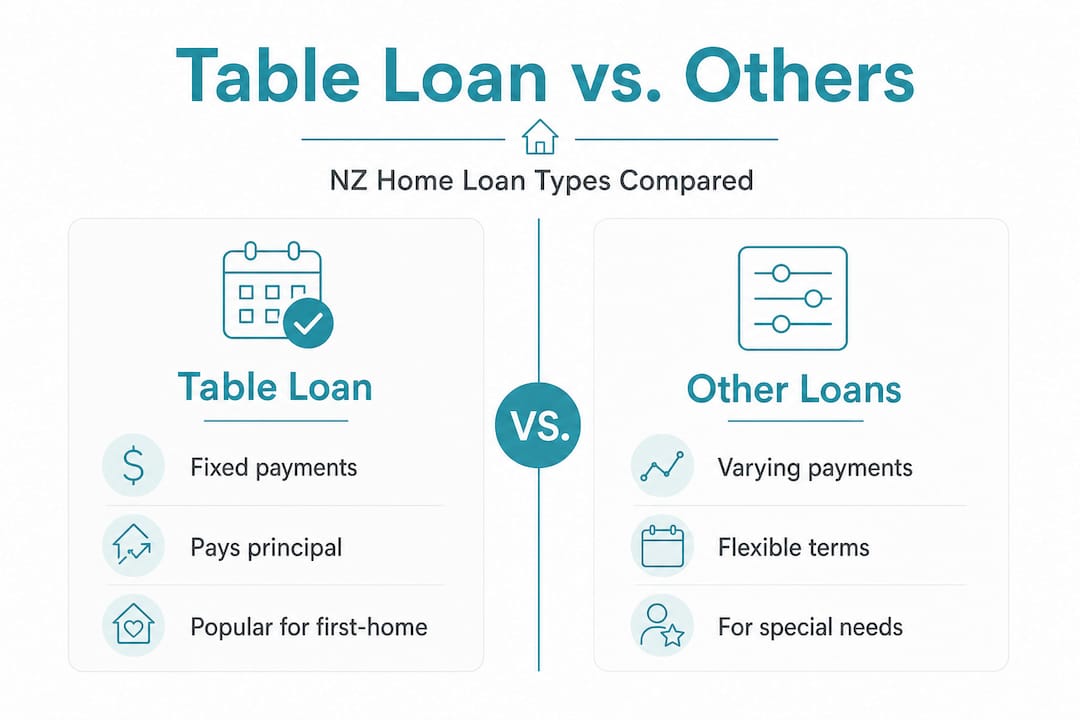

Table loan vs other NZ home loan types

Understanding how table loans are structured is useful, but how do they differ from other loan options you might be offered? Here’s how they stack up.

New Zealand lenders typically offer several loan structures beyond the table loan. It’s worth knowing the differences so you can make an informed choice.

| Loan type | How repayments work | Principal paid down? | Best for |

|---|---|---|---|

| Table loan | Fixed regular repayments covering principal and interest | Yes, from day one | Most buyers, especially first-timers |

| Interest-only | Pay only the interest for a set period | No, until reverts to P&I | Property investors, short-term cashflow management |

| Revolving credit | Mortgage linked to a transaction account; balance fluctuates | Only if you deposit surplus funds | Disciplined borrowers with variable income |

| Reducing balance | Fixed principal repayments plus reducing interest | Yes, but payments decrease over time | Uncommon in NZ; better for those who want lower long-term costs |

For most first-time buyers, the choice comes down to table loans versus interest-only or revolving credit. How interest-only loans work is worth understanding, but they’re generally not suitable for owner-occupiers building equity in their first home. Revolving credit can be powerful, but it requires real financial discipline to avoid spending what you’ve paid off.

The key advantages and disadvantages of table loans are worth laying out clearly:

- Certainty of repayments: You know exactly what you owe each week, fortnight, or month. This makes budgeting straightforward and reduces financial stress.

- Guaranteed equity building: Every repayment reduces what you owe, so your ownership stake in the property grows steadily.

- Wide availability: Virtually all New Zealand lenders offer table loans as their primary home loan product.

- Simplicity: There’s no complex management required, unlike revolving credit facilities.

- Less flexibility in the short term: Unlike a revolving credit loan, you can’t easily access extra repayments you’ve already made without refinancing or using a redraw facility (if your lender offers one).

- Higher early interest costs: Because interest is front-loaded, you pay a lot of interest before your balance reduces substantially.

For first-home buyers, table loans offer stability, and they’re often split between a fixed portion and a floating portion (for example, 80% fixed and 20% floating) to provide both payment certainty and some flexibility.

Pro Tip: A fixed and floating split can be a practical strategy if you want the security of knowing most of your repayment won’t change, while still having the ability to make extra lump-sum repayments on the floating portion without penalty. Talk to your adviser about what split makes sense for your situation. You can also explore compare loan structures and types of home loans in NZ to see which combination suits your goals.

Costs, fees and what to expect

Once you’ve decided on a loan type, it’s wise to see what fees and costs may come up when you apply or set up your table loan.

Many first-time buyers focus entirely on the interest rate when comparing loans, and while the rate is important, it’s not the full picture. There are a range of fees and costs to be aware of when setting up a table loan in New Zealand.

Here’s a breakdown of what you might encounter:

- Application or establishment fee: This is charged by the lender to process and set up your loan. Application fees typically range from $200 to $400, though some lenders charge nothing at all, and others may charge over $1,000.

- Legal fees: You’ll need a solicitor to handle the property purchase and loan documentation. Budget at least $1,500 to $2,500.

- Valuation fee: Lenders often require a registered valuation of the property, which can cost $500 to $900 depending on the property type and location.

- LIM report: A Land Information Memorandum from the local council provides important property information and typically costs $200 to $400.

- Lenders mortgage insurance (LMI): If your deposit is less than 20%, some lenders may require this as additional protection, though this is less common in New Zealand than in Australia.

- Ongoing account fees: Some lenders charge monthly or annual fees for maintaining your loan account.

Key figure to keep in mind: Application fees alone can vary from $0 to over $1,000 depending on the lender. This is a wide range, and it’s absolutely worth asking whether fees are negotiable before signing anything.

The good news is that many of these fees, particularly application fees, are negotiable, especially if you’re borrowing a substantial amount or if you’re working with a mortgage adviser who has an existing relationship with the lender. Never assume the fee listed is the fee you’ll pay.

Preparing for a NZ home loan well in advance means you won’t be caught off-guard by these costs when settlement day arrives. Factor them into your budget alongside your deposit from the very beginning.

Tips for first-time buyers using a table loan

Knowing the structure and cost, let’s wrap up with practical tips on making table loans work for you as a first-home buyer.

- Choose a repayment frequency that aligns with your pay cycle. If you’re paid fortnightly, set up fortnightly repayments. This naturally means you make 26 repayments per year instead of 24, which subtly accelerates your loan payoff without you noticing the extra effort.

- Consider splitting your loan between fixed and floating. As noted earlier, table loans for first-home buyers are often structured with an 80/20 fixed-to-floating split. The fixed portion gives you certainty; the floating portion gives you the ability to pay more when you can.

- Review your loan at least annually. Interest rates change, your income may increase, and your financial goals will evolve. A regular review means you’re always on the best deal available and your repayments reflect your current situation.

- Don’t ignore the floating portion. If you have a split loan, direct any surplus funds, like a bonus or tax refund, to the floating portion first. There’s no break fee, so extra payments hit your balance immediately.

- Explore government support options early. As a first-home buyer, you may be eligible for additional assistance. Checking the Welcome Home Loan for Auckland buyers is a great first step if you’re in the region.

Pro Tip: The single most impactful time to make extra repayments is in the first five years of your loan. Because your balance is at its highest during this period, any reduction in the principal saves you interest on a larger sum for a longer period. Even one extra regular payment per year during this phase can knock years off your loan term.

Why most Kiwi first-home buyers are better off with table loans

Let’s be candid about something: in the world of mortgages, there’s always a newer, supposedly smarter product being promoted. Revolving credit lines, offset accounts, interest-only structures with “investment upside,” and various other arrangements are all presented as ways to be financially savvy. But in our experience working with first-home buyers across Auckland and wider New Zealand, the classic table loan remains the best starting point for the vast majority of people, and for very good reasons.

Certainty is underrated. When you’re managing a new mortgage alongside all the costs of owning a home for the first time, knowing exactly what leaves your account each pay cycle is genuinely valuable. It removes one major source of financial anxiety from your life. Revolving credit and interest-only loans require a level of financial discipline and active management that most people, understandably, find hard to maintain alongside the rest of life.

There’s also a clear industry signal worth noting. BNZ is transitioning from its “tailored” home loan product to the standard table loan structure, citing simplification as the reason. This isn’t a coincidence. When one of New Zealand’s major banks decides the table loan is the cleaner, clearer product for borrowers, it reflects a broader industry recognition that simplicity genuinely serves customers better.

Conventional isn’t boring when it’s the right fit. The buyers who struggle most with their mortgages are often those who chose a more complex structure they didn’t fully understand. The table loan is transparent, well-regulated, and predictable. Understanding why you should compare home loans across lenders matters, but the structure itself is rarely worth overcomplicating for a first purchase.

Get expert help choosing your table loan

If you’re still unsure which loan structure is right for your first home, that’s where expert help makes a real difference.

At Mortgage Managers, we work with first-time buyers across Auckland, the North Shore, West Auckland, and remotely throughout New Zealand to find the right loan structure, secure competitive rates, and make sure you understand every part of what you’re signing. Our mortgage advisers for home loans act as your personal guide through the process, comparing options across multiple lenders so you don’t have to.

Understanding the role advisers play in home buying can genuinely save you thousands of dollars in fees, interest, and avoidable mistakes. We offer a free initial consultation, so there’s no cost to getting your questions answered. Reach out to the team at Mortgage Managers today and take the next step towards your first home with confidence.

Frequently asked questions

Can I pay off a table loan early in New Zealand?

Yes, you can pay off a table loan early, but check with your lender first as repayment conditions vary and there may be break fees on fixed-rate portions.

Is it better to split a table loan between fixed and floating rates?

Many first-home buyers benefit from splitting their loan, as an 80/20 fixed-floating split provides both payment certainty and the flexibility to make extra repayments without penalty.

Are table loans available from all New Zealand lenders?

Yes, virtually all major lenders offer table loans because a table loan is the most common type of home loan in New Zealand and is considered the standard product.

What fees should I expect when setting up a table loan?

Expect application fees from $200 to $400, though amounts range from nothing to over $1,000 and are often negotiable, plus legal and valuation costs on top.

Why are table loans called ‘table’ loans?

They’re called “table” loans because repayments are calculated using an amortisation table that maps the fixed payment schedule across the entire loan term.