TL;DR:

- Many Auckland first home buyers focus solely on saving a deposit, unaware that their debt-to-income ratio significantly impacts mortgage approval. Lenders prioritize DTI to assess whether borrowers can comfortably handle new payments alongside existing debts, making it a critical factor in the application process. Improving DTI through debt reduction and income documentation before applying greatly enhances your chances of success.

Many first home buyers in Auckland pour everything into saving a deposit, only to find their mortgage application stalls at a hurdle they never saw coming. Your deposit matters, but lenders are equally focused on a figure that tells them whether you can comfortably carry the loan you are asking for. That figure is your debt-to-income (DTI) ratio. Understanding how it works, what Auckland lenders expect, and how to improve yours before you apply could be the difference between getting the keys to your first home or going back to the drawing board.

Table of Contents

- What is the debt-to-income ratio and why does it matter?

- How lenders in Auckland use the debt-to-income ratio

- What is a ‘good’ debt-to-income ratio for first home buyers in Auckland?

- How to lower your debt-to-income ratio before applying

- The surprising truth about DTI and first home success

- How expert advice takes the risk out of DTI for buyers

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| DTI is critical for approval | Lenders rely on your debt-to-income ratio to assess if you can afford a home loan. |

| Aiming for a lower DTI | Target a DTI of four or below for better mortgage terms and approval chances. |

| Start improving DTI early | Reducing debt and boosting income months before you apply strengthens your application. |

| Expert help boosts odds | Mortgage advisers can guide you to optimise DTI and secure the right loan. |

What is the debt-to-income ratio and why does it matter?

The debt-to-income ratio is essentially a snapshot of your financial balance. It compares what you owe each month against what you earn, giving lenders a quick but powerful read on how much financial pressure you are already carrying. In simple terms, DTI is calculated as your total monthly debt obligations divided by your gross (pre-tax) monthly income, including existing debts and your projected mortgage payment.

The formula looks like this:

DTI ratio = Total monthly debt payments ÷ Gross monthly income

Let us look at a practical Auckland example. Suppose your gross monthly income is $8,000. You have a car loan repayment of $400 per month and a credit card minimum payment of $150 per month. You are applying for a mortgage with estimated repayments of $2,800 per month. Your total monthly debt is $3,350, which gives you a DTI of approximately 0.42, or 42%. Banks also express this as a ratio of 4.2 times income when they are thinking about total loan size rather than monthly repayments.

Understanding why lenders focus on DTI is just as important as knowing how to calculate it. A big deposit tells a bank you are disciplined and have skin in the game. But DTI tells them something deeper: whether your income can absorb a new mortgage payment without you struggling to cover everyday costs. This is why the mortgage approval process in New Zealand places such significant weight on this number alongside your deposit and credit history.

Here is what your DTI typically includes:

- Your anticipated mortgage repayment

- Car loans or vehicle finance

- Student loans or personal loans

- Credit card minimum monthly payments

- Any hire purchase agreements or buy-now-pay-later balances with regular obligations

- Any other recurring debt commitments

“A strong deposit is just one part of the picture. Lenders want to see that your income gives you enough breathing room to handle a mortgage payment alongside everything else you already owe.”

Keeping these categories in mind as you assess your own financial position is a smart early step before you move into mortgage pre-approval basics.

| Monthly income | Monthly debts | Projected mortgage | DTI ratio |

|---|---|---|---|

| $8,000 | $550 | $2,800 | 41.9% (4.2x) |

| $10,000 | $800 | $3,200 | 40.0% (4.0x) |

| $7,000 | $1,000 | $2,500 | 50.0% (5.0x) |

| $9,500 | $400 | $2,700 | 32.6% (3.3x) |

How lenders in Auckland use the debt-to-income ratio

Knowing what DTI is one thing. Understanding how Auckland lenders actually apply it during your application is where the real insight begins. New Zealand banks and non-bank lenders use DTI thresholds as a risk-management tool, and since the Reserve Bank of New Zealand introduced formal DTI restrictions, these thresholds have become more defined and more consistently applied.

Here is a step-by-step look at how your DTI gets evaluated when you submit a home loan application:

- Income verification. The lender reviews your payslips, tax records, or financial statements to confirm your gross income. This includes salary, wages, and any regular secondary income you can document.

- Debt disclosure. All existing credit commitments are added up. Lenders cross-check this against credit bureau records, so attempting to omit debts rarely works in your favour.

- Mortgage calculation. Your proposed loan amount is converted into an estimated monthly repayment at a test interest rate (often higher than the current rate) to stress-test your ability to cope with rate increases.

- Ratio calculation. Total monthly obligations are divided by gross monthly income to produce your DTI ratio.

- Threshold comparison. Your DTI is compared against the lender’s internal limits and any regulatory caps in place at the time of your application.

- Decision. If your DTI sits within acceptable limits, your application moves forward. If it exceeds those limits, you may face reduced borrowing capacity or a declined application.

The critical insight here is that higher DTI generally means less ability to absorb the new monthly loan payment, and this is precisely why lenders treat it as a primary filter. Different DTI outcomes translate into different lending experiences:

| DTI level | Likely lender response |

|---|---|

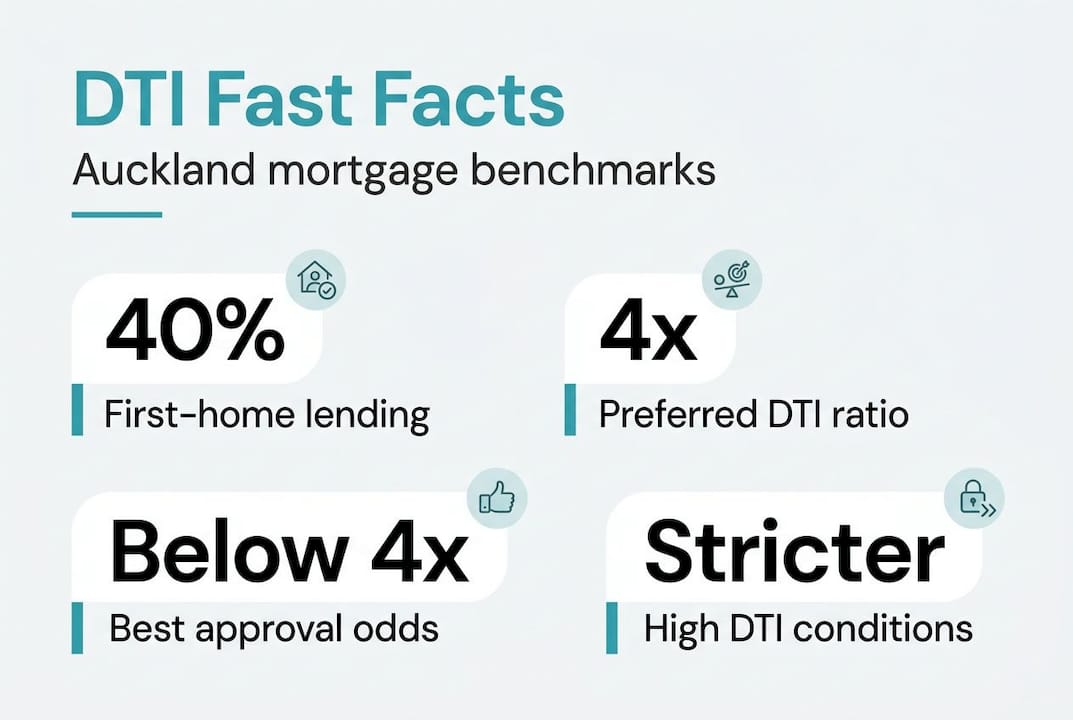

| Below 4x | Strong application, maximum borrowing options |

| 4x to 5x | Generally approvable, standard terms likely |

| 5x to 6x | Possible, but stricter conditions may apply |

| Above 6x | Very limited options, likely declined by major banks |

Understanding lender criteria for first home loans in Auckland gives you a real advantage, because each lender applies slightly different internal policies even within regulatory guidelines.

Pro Tip: Always disclose every debt and every income stream when working with a mortgage adviser. Lenders will find undisclosed debts through credit checks, and surprises at this stage can damage your credibility as a borrower and delay your application significantly.

What is a ‘good’ debt-to-income ratio for first home buyers in Auckland?

This is the question most buyers are really asking. And the honest answer is: lower is better, but the reality of Auckland’s housing market means many first home buyers are borrowing at relatively high multiples compared with buyers in other regions.

Recent data offers a clear benchmark. About 40% of first-home buyer lending in New Zealand was done to borrowers with a DTI ratio of between four and five. That is a significant proportion of approvals sitting in what most lenders would consider the upper-middle range. This tells you two things: you are not alone if your DTI falls in that band, and it is clearly a zone where lending still happens regularly.

What does this look like in practical terms? If your gross annual income is $120,000 (or $10,000 per month), a DTI of five means your total borrowing would be $600,000. A DTI of four means $480,000. Those are real numbers in the Auckland market, and they underline why understanding features of first-time buyer mortgages alongside your DTI positioning is so important.

Here is a breakdown of what the different DTI bands mean for you:

- Below 3x: Excellent position. Most lenders will be eager to work with you, and you will likely access the best rates and terms available.

- 3x to 4x: A solid, comfortable range. You have strong borrowing capacity and healthy flexibility.

- 4x to 5x: This is where the bulk of Auckland first home buyers land. Approval is achievable, but every other element of your application needs to be strong.

- 5x to 6x: Risk territory. Some lenders may proceed under strict conditions, but your choices narrow considerably.

- Above 6x: Very high risk. Most mainstream banks will not lend here, and specialist lenders will apply very tough terms.

Key insight: The Reserve Bank introduced DTI restrictions specifically to reduce systemic risk in New Zealand’s housing market. Most banks are now limited in how much lending they can do above a DTI of six for owner-occupiers.

Knowing where you sit is the first step in improving your eligibility and building a strategy that gets your application across the line.

How to lower your debt-to-income ratio before applying

The encouraging news is that DTI is not a fixed number. You have real power to improve it, and even modest improvements can shift your application from a borderline case to a confident one. The core principle is straightforward: reducing debts or increasing income ahead of your application will bring your DTI down.

Here are the most practical steps you can take right now:

- Pay down high-interest consumer debt first. Credit cards and personal loans are often the fastest debts to eliminate, and removing even one payment from your monthly obligations can shift your DTI meaningfully. Focus on accounts with small remaining balances that you can clear quickly.

- Close unused credit accounts. Even if you are not using a credit card, lenders factor in the available limit as a potential future obligation. Closing accounts you no longer need can reduce your assessed debt exposure.

- Avoid new debt entirely before applying. A new car loan or finance agreement taken out in the months before your application can undo weeks of preparation in a single decision.

- Document all of your income. Side income, rental income, or irregular bonuses may not always appear in your standard payslips. Working with a mortgage adviser to properly document and present additional income streams can lift your gross income figure, which directly lowers your DTI.

- Consider a co-borrower. Adding a partner or family member with income to your application increases the total gross income used in the calculation, which can significantly improve your ratio.

- Time your application carefully. If you recently paid off a significant debt, wait for that account to close and appear correctly on your credit file before applying.

For those who are actively improving home loan eligibility, the combination of debt reduction and income documentation often produces the fastest results. Even a three to six month focused effort before applying can make a material difference.

Pro Tip: Never take on new finance, including buy-now-pay-later agreements, in the six months before you apply for a home loan. Even small new obligations can raise your DTI at exactly the wrong moment. When you are preparing for a home loan, treat your financial profile as something you are actively managing, not just observing.

The surprising truth about DTI and first home success

Here is something we have observed working with Auckland first home buyers over many years: the buyers who struggle most are rarely the ones with the smallest deposits. They are the ones who focused so intensely on saving that they never addressed the debt they were carrying at the same time.

It is remarkably common to meet someone with a solid 20% deposit who is also carrying $30,000 in student debt, a car loan, and two credit cards. They feel ready. Their savings account looks impressive. But their DTI tells a different story, and lenders read that story very clearly.

The conventional wisdom says: save more, borrow confidently. But the practical truth is that $10,000 used to pay off an existing loan can do more for your mortgage application than the same $10,000 added to your deposit fund. Paying down debt lowers your monthly obligations, reduces your DTI, and increases the mortgage amount you can access. That is a three-way win that most buyers never consider.

We also find that many buyers underestimate how powerfully their financial behaviour in the twelve months before application shapes a lender’s decision. Not just the DTI number, but the story behind it. Did you bring down your debt thoughtfully? Have your spending patterns been consistent? These things show up in your file, and a good mortgage adviser knows how to present that context in a way that supports your application.

The approval tips for first-timers that actually make a difference are rarely the dramatic ones. They are usually the quiet, consistent financial decisions made over the six to twelve months before you apply. Your DTI is your most controllable lending metric. Treat it that way.

How expert advice takes the risk out of DTI for buyers

Navigating your DTI position on your own can feel like trying to read a map without knowing your starting point. That is where we come in.

At Mortgage Managers, we work with Auckland first home buyers every day, helping them understand exactly where they stand before they ever submit an application. We review your full financial picture, identify the debts worth prioritising, and help you present your income in the most complete and accurate way possible. Our team of experienced Auckland mortgage advisers is based in Hobsonville, giving us natural reach across West Auckland, the North Shore, and beyond. When you speak to our Auckland mortgage brokers, you get personalised guidance built around your actual numbers, not a generic checklist. When you are ready to move forward, you can apply for a mortgage with a team that already knows your position and has a strategy to support it.

Frequently asked questions

What debts are included in the debt-to-income ratio?

DTI includes all monthly debt obligations such as credit cards, student loans, car finance, and the projected mortgage repayment. Lenders look at your complete monthly obligation picture, not just your biggest debts.

Does having a higher income improve your DTI?

Yes, because DTI is debt divided by gross income, increasing your earnings while keeping debts the same will lower your ratio and strengthen your application considerably.

What DTI ratio do most Auckland banks prefer?

About 40% of first-home buyer lending is done at a DTI between four and five, but sitting below four gives you the most options and the strongest negotiating position with lenders.

Can I get a mortgage with a high DTI?

It is possible, but higher DTI generally means stricter lending conditions, lower borrowing limits, and fewer lender options willing to consider your application at all.

How quickly can I improve my DTI before applying?

Reducing debts or increasing income can produce a meaningful DTI improvement within three to six months, which is why planning ahead before you apply is so valuable.