TL;DR:

- Many first home buyers in New Zealand mistakenly believe that having sufficient equity eliminates the need for a deposit, leading to costly misconceptions. Deposits consist of cash or approved funds contributed at purchase, while equity reflects outright ownership in a property and cannot simply be used interchangeably; lenders treat them differently. Understanding these differences, sources of deposits, and the impact of low-deposit schemes can significantly improve your mortgage application success.

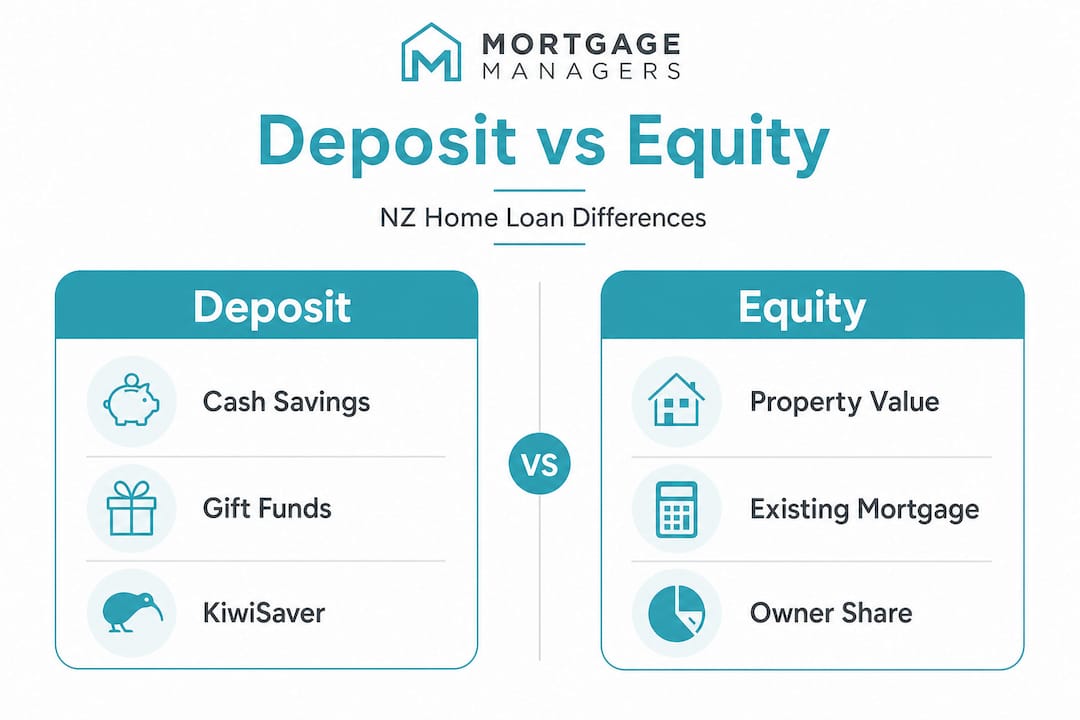

Many first home buyers in New Zealand arrive at the home loan conversation believing that if they have enough equity somewhere, they have their deposit sorted. It is one of the most common and costly misconceptions we encounter, and it can send your application in the wrong direction before it even begins. In NZ home lending, deposit is the cash or other approved funds you contribute to the purchase price, while equity is the portion of a property’s value you effectively own outright. These two terms are related, but they are not the same thing, and banks treat them very differently.

Table of Contents

- What does deposit mean when buying your first home?

- What is equity and how does it relate to deposits?

- Deposit vs equity: What’s the real difference for Kiwi buyers?

- What happens if your deposit is less than 20%?

- How to improve your position: Practical tips for first home buyers

- Why most first home buyers get tripped up by deposit and equity rules

- Get expert help to succeed on your home loan journey

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Deposit vs equity basics | Deposit is what you put down for your new home, while equity is your ownership in any existing property. |

| Standard deposit needed | Most NZ lenders expect a 20 percent deposit, but low-deposit options may be possible with extra conditions. |

| Low deposit costs | Borrowing with less than 20 percent deposit can include higher interest rates and fees until you build more equity. |

| Equity can assist | Existing property equity can sometimes help with a new deposit, but only within lender limits and not for all buyers. |

| Professional advice value | An expert adviser can clarify options, avoid mistakes, and help you maximise your deposit or equity strategy. |

What does deposit mean when buying your first home?

Now that we’ve challenged the confusion, let’s break down what “deposit” really means in practical terms for Kiwi first home buyers.

Your deposit is the money you bring to the table at the time of purchase. It is the portion of the property price you are paying upfront, with the mortgage covering the rest. For lenders, it is also a signal. When you contribute a meaningful deposit, you are demonstrating financial discipline and reducing the bank’s risk. The bigger your deposit, the less the bank needs to lend relative to the property’s value, which is measured by the loan-to-value ratio (LVR).

For most owner-occupied home purchases in NZ, lenders expect around 20% as the standard deposit, which brings the loan to an 80% LVR or lower. This threshold matters because it is where standard mortgage products, competitive interest rates, and the broadest range of lenders become available to you. Understanding deposit requirements NZ wide is a solid first step when planning your purchase.

Acceptable sources of deposit in New Zealand typically include:

- Personal savings held in a bank account

- KiwiSaver funds (subject to withdrawal eligibility rules)

- Government assistance such as the First Home Grant

- Gifted funds from a family member (subject to lender assessment)

- Proceeds from the sale of an existing asset

“A deposit is more than just a number on a page. It tells the lender that you are invested in this purchase and that you have the financial habits to follow through.”

Each of these sources carries its own documentation requirements. Your savings will need a clear paper trail. Gifted funds will need to be verified as a genuine gift rather than a loan. Our First Home Grant guide explains how government assistance can be applied toward your deposit, which is helpful if you are in the early stages of building up funds.

Pro Tip: Start pulling your deposit sources together at least six months before you plan to apply. Lenders want to see genuine savings history, not a large lump sum that appeared last week.

What is equity and how does it relate to deposits?

Understanding deposit is one side of the puzzle. Let’s look at equity, how it is built, and where it fits in home loan applications.

Equity is your ownership stake in a property. In simple terms, it is the difference between a property’s value and what you owe on it. For example, if your home is worth $400,000 and you have a $100,000 home loan remaining, your equity in that property is $300,000. That equity represents real financial value, and in some situations, it can be drawn upon to help fund another purchase.

However, using equity as a deposit is not as straightforward as it sounds. Banks usually limit how much of your existing home’s equity you can use when buying a new property, and there are clear rules around minimum equity retention. Typically, lenders want you to retain at least 20% equity in your existing property after releasing funds, meaning you cannot simply access every dollar of ownership you have built up.

Here is a quick comparison of how equity builds over time in a typical scenario:

| Property value | Outstanding loan | Equity | Equity % |

|---|---|---|---|

| $500,000 | $400,000 | $100,000 | 20% |

| $500,000 | $300,000 | $200,000 | 40% |

| $600,000 | $300,000 | $300,000 | 50% |

| $700,000 | $250,000 | $450,000 | 64% |

For true first home buyers who do not yet own any property, equity is generally not part of the equation unless:

- A family member is acting as a guarantor using their own property equity

- You are buying jointly with someone who already owns real estate

- A family trust arrangement applies

If you are curious about how this looks in practice, exploring examples of low deposit lenders can give you a clearer picture of how different structures are assessed.

Pro Tip: If a parent is considering using their home’s equity to help you purchase your first property, have a frank conversation with a mortgage adviser before assuming it will work. The rules around guarantor equity arrangements are specific and not all lenders treat them the same way.

Deposit vs equity: What’s the real difference for Kiwi buyers?

With definitions clear, let’s break down the main differences and common scenarios using a practical side-by-side comparison.

At their core, deposit and equity serve different functions in the home lending world. Your deposit applies directly to the transaction you are completing right now. It sets the LVR for the new loan and determines which products, rates, and lenders are available to you. Equity, by contrast, reflects your financial position in property you already own. These two things interact, but they are never simply interchangeable.

| Feature | Deposit | Equity |

|---|---|---|

| What it is | Cash or approved funds for new purchase | Ownership stake in existing property |

| When it matters | At time of new loan application | When leveraging existing assets |

| Who it applies to | All buyers, including first home buyers | Typically existing property owners |

| Lender treatment | Directly applied to purchase price | Released funds must still meet LVR rules |

| Flexibility | Several approved sources | Subject to minimum retention limits |

As ANZ notes, you should not treat equity as the same thing as deposit. Equity is your ownership stake in an existing property. Deposit is what gets applied to the purchase price for the loan you are applying for.

Here is how this plays out in three common scenarios:

- True first home buyers have no existing property equity. Your entire deposit must come from savings, KiwiSaver, grants, or family contributions.

- Existing owners upgrading may be able to release equity from their current home as part of the deposit for a new property, within lender limits.

- Family guarantor situations allow equity in a parent’s or relative’s property to support the loan, but this carries risk for the guarantor and requires careful structuring.

Understanding which scenario applies to you shapes the entire application strategy. For a detailed breakdown, our page on deposit requirements explained walks through the bank’s perspective in plain language.

What happens if your deposit is less than 20%?

You might be wondering, what if you cannot reach the 20% figure yet? Here is how banks and schemes handle smaller deposits, and what it means for you.

The honest answer is that getting a home loan with less than a 20% deposit is possible, but it comes at a cost. Special products and government-backed schemes can bring the deposit requirement down to as low as 5%, but eligibility is strict and the fine print matters. Kāinga Ora’s First Home Loan is one option that can reduce the deposit requirement to 5% for eligible borrowers, but income caps, property price limits, and lender participation all affect who can access it.

The most significant consequence of a low deposit is the addition of what is called a low equity margin or low equity premium. Low-deposit borrowing can trigger lender risk pricing such as low-equity margins or premiums, and these remain in place until your equity improves. In practical terms, this means your interest rate will be higher than the standard rate, potentially costing you thousands of extra dollars over the years until you build enough equity to have the margin removed.

Other important realities of low-deposit lending include:

- Not all banks offer low-deposit products, so your lender options are narrower

- Your application will face tighter scrutiny on income stability and spending habits

- Some lenders charge a one-off low equity premium as an upfront fee instead of a margin

- Removing the margin usually requires reaching 20% equity, which may need a formal property revaluation

Our low deposit mortgage guide covers the landscape thoroughly, and if you want to explore whether a 5% path is realistic for you right now, our page on 5% deposit home loan options is worth a look.

First home buyer low-deposit options come with eligibility restrictions, pricing constraints, and often ongoing cost loadings. Even when a 5% deposit is possible, it is not the same as no cost.

Pro Tip: Before going down the low-deposit route, do a cost comparison. Calculate the total extra interest you would pay over several years with a low equity margin, then weigh that against waiting 12 to 18 more months to save a larger deposit. Sometimes patience saves a significant amount of money.

How to improve your position: Practical tips for first home buyers

With the risks and pros/cons clear, let’s finish with a toolkit of practical ways to strengthen your application, whether your main path is deposit-based or equity-supported.

Building a stronger application starts with understanding what lenders actually want to see, then working backwards from that picture. The good news is that there are more options available to Kiwi first home buyers than ever before, and even when 5% is possible, it is not the same as “no cost”, which is why a strategic approach matters so much.

Here are the most practical ways to boost your deposit position:

- Maximise your KiwiSaver contributions by increasing your contribution rate, even temporarily, to accelerate fund growth

- Apply for the First Home Grant if your KiwiSaver contributions and income meet the criteria

- Reduce high-interest debt such as credit cards and buy-now-pay-later balances, which both frees up cash and improves your application profile

- Ask family members about gifted deposits and understand that lenders will ask for documentation confirming the gift is not repayable

- Set a defined savings target with a monthly budget that treats your deposit savings as a non-negotiable bill

When it comes to building equity in a property you already own or accessing a family member’s equity, consider these steps:

- Make extra repayments on your existing mortgage to build equity faster

- Invest in property improvements that increase the market value, supporting a revaluation

- Have a formal conversation with a mortgage adviser about whether a family guarantee is viable and what protections are needed

We have put together a dedicated resource on how to boost your deposit specifically for Kiwi buyers. There are also first-time buyer features worth understanding before you commit to any single product.

Pro Tip: Strengthen your application across every assessed dimension, not just the deposit. Steady income, clean banking history, and low existing debt all work together to build a picture of a reliable borrower.

Why most first home buyers get tripped up by deposit and equity rules

You have learned the frameworks and the details. Now here is what most articles do not tell you about the real-world experience for Kiwi buyers.

The biggest trap we see is buyers who focus entirely on reaching a deposit threshold without appreciating how conditional the rules around using that deposit actually are. Someone who has $80,000 in equity in a family member’s property is not automatically walking into a bank with an $80,000 deposit. The lender will ask how the equity is being structured, what the LVR on the existing property will be after the release, and whether the arrangement qualifies under their policy. Some lenders simply do not accept these arrangements at all.

There is also a common belief that released equity is treated the same as cash savings. It is not. Cash savings demonstrate financial discipline over time. Released equity demonstrates asset value, which is a different kind of evidence entirely. Banks look at both, but they apply different weight to each.

Low-deposit schemes are genuinely useful tools, but they are not a shortcut to the same outcome as a 20% deposit. You are borrowing at a higher rate, your flexibility to refinance or switch lenders may be reduced, and the extra cost can quietly add up over time. The buyers who navigate this successfully are the ones who go in with clear eyes, understand the trade-offs, and plan accordingly.

The most effective thing you can do early in your journey is sit down with a mortgage adviser, ideally before you start property searching, and map out your actual position. This is not about being told what you cannot do. It is about understanding what you can do and structuring your approach so your application gives you the best possible chance. Our Auckland first home buyer guide is a strong starting point if you are planning to buy in the region.

The smartest buyers we work with are not always the ones with the biggest deposits. They are the ones who understand what banks really want to see, and who optimise every aspect of their application accordingly.

Get expert help to succeed on your home loan journey

If you are ready to apply what you have learned, or if you simply need a tailored plan that accounts for your specific deposit and equity situation, our team at Mortgage Managers is here to help.

Our personal mortgage advisers understand the specific deposit and equity rules applied by each lender across New Zealand. We can help you access product comparisons, pre-qualify for low-deposit schemes, and structure your application in a way that genuinely reflects your strengths. Based in Hobsonville and servicing clients across Auckland and remotely throughout New Zealand, we offer practical, real-world guidance without the jargon. Start a conversation with us today through our mortgage application support page, and get answers tailored to your situation rather than generic information.

Frequently asked questions

Can I use KiwiSaver as a deposit or does it count as equity?

KiwiSaver funds are used as part of your deposit for a first home purchase, provided you meet the withdrawal eligibility criteria, not as equity. They count toward the cash contribution you are making to the purchase price.

What happens if my property value drops after settlement?

If your property’s value falls, your equity level decreases, and if it drops below the bank’s minimum threshold, you may face higher interest rates or be required to top up. Low-equity margins can be triggered when your equity falls below the lender’s threshold and remain until your equity improves.

Is it easier to get a home loan with high equity or a big deposit?

A bigger deposit is more helpful for first home buyers seeking to secure a loan on their first property, while high equity is more relevant when you already own real estate. Standard bank settings are still based around a 20% deposit or 80% LVR as the benchmark for most owner-occupied purchases.

How soon can I remove a low equity margin after buying with a small deposit?

Low equity margins can often be removed once your loan-to-value ratio reaches 80%, which may be demonstrated through extra repayments or a formal property revaluation. A low equity margin remains in place until your equity stake in the property reaches that 20% threshold.

Do banks treat a gifted deposit the same way as personal savings?

Lenders typically assess gifted deposits carefully and will require documentation confirming the funds are a genuine gift rather than a loan that must be repaid. This verification process exists because a repayable gift changes your actual liability position and affects how the bank calculates what you can afford.