TL;DR:

- Rebates are post-purchase refunds paid after submitting a claim, unlike instant discounts at checkout. Cashback rewards are calculated as a percentage of the transaction amount, often appearing after an unpaid delay, and can be stacked from multiple sources. To maximize savings, consumers must stay organized, track deadlines, and avoid common pitfalls like missed submissions or expired rewards.

Most people assume a rebate or cashback is just another word for a discount. It isn’t. With rebates and cashbacks explained properly, you quickly realise these are post-purchase rewards that work very differently from a price cut at the register. Understanding that distinction matters because it changes how you shop, how you track your spending, and ultimately how much you actually keep in your pocket. This article breaks down exactly how each programme works, where New Zealanders can find them, how to stack them effectively, and the pitfalls that cause most people to miss out.

Table of Contents

- Key takeaways

- How rebates actually work

- Cashback programmes explained

- Cashback vs rebates: key differences

- Maximising your savings in New Zealand

- Common pitfalls that cost people their rewards

- Stuart’s perspective on making these programmes actually work

- How Mortgagemanagers helps you make more of your money

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Rebates are post-purchase | You pay full price first, then claim a partial refund after submitting proof of purchase. |

| Cashback has a delay | Rewards typically appear on your account between 1 and 90 days after a transaction clears. |

| Stacking multiplies savings | Credit cards, cashback portals, and card-linked offers can all pay out independently on the same purchase. |

| Programme funds can run dry | Public rebate schemes can exhaust budgets mid-cycle, so verify availability before you rely on them. |

| Fine print changes everything | Many cashback rewards are paid in points or gift cards, not cash, so always confirm redemption terms. |

How rebates actually work

A rebate is a conditional, post-purchase incentive. You pay the full retail price at checkout, then submit a claim afterwards to receive a partial refund. That refund might arrive as a prepaid card, a direct bank transfer, or a credit applied to a future purchase. Rebates are distinct from point-of-sale discounts and require you to take deliberate steps to receive the benefit.

The process generally follows these stages:

- Purchase at full price. You buy the product or service at its listed retail price.

- Collect proof of purchase. This usually means keeping your receipt, invoice, or order confirmation.

- Submit the claim. You complete a form online or by post within a specified window, often 30 to 90 days from purchase.

- Wait for processing. The issuer verifies your claim, which can take several weeks.

- Receive the refund. Payment arrives via the method stated in the programme terms.

Common rebate types in New Zealand include volume-based rebates (where you earn more as you buy more), promotional rebates tied to specific product launches, and government-backed incentive schemes. The New Zealand Government has previously offered rebates on energy-efficient appliances and electric vehicles, though these programmes operate on fixed budgets and can close without much notice.

Pro Tip: Always photograph your receipt and email it to yourself the day you make a rebate-eligible purchase. Waiting until submission day is the fastest way to lose the document you need most.

The key contrast with an upfront discount is that a rebate keeps the shelf price intact. For retailers and manufacturers, this protects their pricing structure. For you, it means you need to be organised to capture the saving.

Cashback programmes explained

Cashback works on a similar post-purchase principle, but the mechanics differ in a few meaningful ways. Rather than a fixed refund amount, cashback is calculated as a percentage of the transaction amount and paid after the transaction clearing period, typically between 1 and 90 days. The money does not come from the retailer discounting their price. It comes from merchant marketing budgets or bank interchange fees, which is why the shelf price stays the same.

Here is how the most common cashback delivery channels work:

- Credit card cashback. Your bank pays you a percentage of eligible spending, funded from interchange fees charged to merchants. Rates in New Zealand typically range from 0.5% to 2%, depending on the card and spend category.

- Cashback portals. Websites that negotiate commission agreements with retailers then pass a portion back to you when you shop through their link. The retailer pays the portal, and the portal pays you.

- Card-linked offers. You activate specific deals through your banking app, then simply pay with your registered card at the participating merchant. The cashback posts automatically.

- Buy-now-pay-later and fintech apps. Some newer platforms offer cashback as a loyalty incentive, funded from their own merchant partnerships.

One misconception worth addressing: cashback is deferred and conditional, not instant savings. The funds are often held during a return window, meaning if you return the item, the cashback is reversed. Budget around this timing rather than treating pending cashback as money you have already received.

Pro Tip: Activate card-linked offers before you shop, not after. Most platforms will not backdate a reward if you forgot to switch it on.

Another detail that catches people off guard is that many cashback rewards are paid in points, credits, or gift cards rather than liquid cash. Always verify what form the reward takes and whether it has an expiry date before you factor it into your savings calculations.

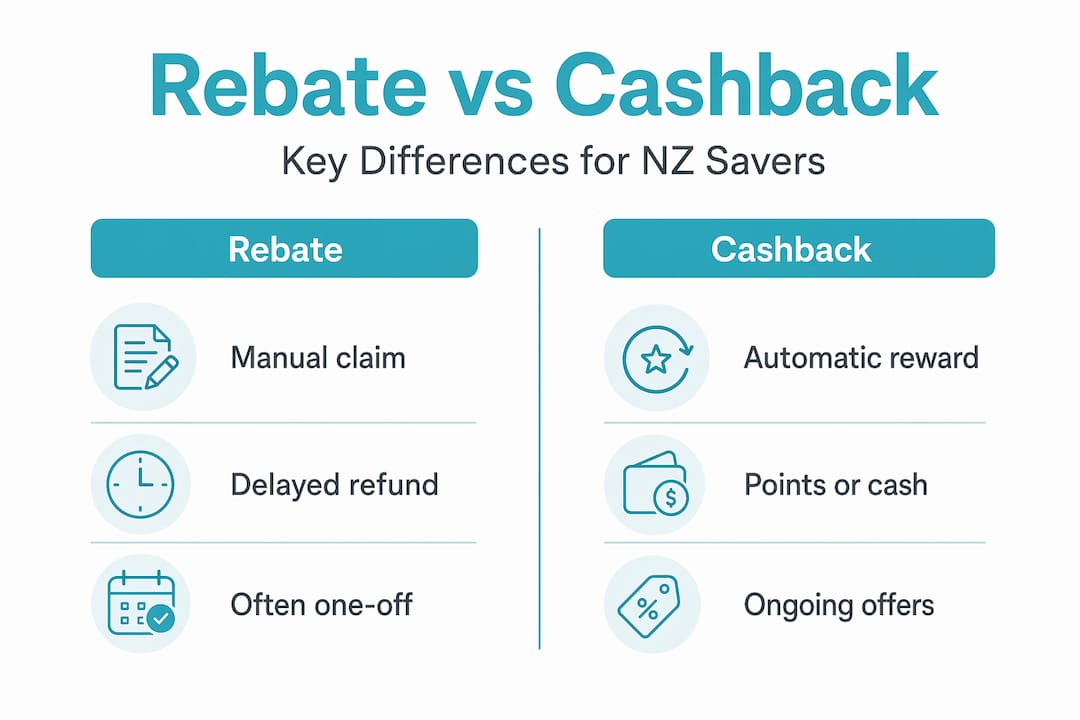

Cashback vs rebates: key differences

Both programmes protect retail pricing while incentivising purchases. Both pay out after the transaction. Beyond those two similarities, there are meaningful differences worth mapping clearly.

| Feature | Rebate | Cashback |

|---|---|---|

| Payment trigger | Manual claim submission | Automatic after transaction clears |

| Reward format | Prepaid card, bank transfer, or credit | Cash, points, gift card, or statement credit |

| Eligibility criteria | Proof of purchase, sometimes product registration | Active card, portal link, or offer activation |

| Typical timeframe | 4 to 12 weeks | 1 to 90 days |

| Common use cases | Appliances, vehicles, government incentives | Retail spending, groceries, travel, utilities |

| Funding source | Manufacturer or government programme budget | Merchant marketing budget or interchange fees |

Brands use cashback rather than discounts specifically to protect long-term brand equity. Offering a discount trains customers to wait for lower prices. Cashback rewards loyal buyers without signalling that the product is worth less.

A few practical points that apply to both:

- Both programmes are time-limited. Missing a submission window or an offer expiry date means the saving disappears entirely.

- Terms can exclude certain product categories, so check eligibility before assuming a purchase qualifies.

- Government rebate programmes and bank cashback offers can change at short notice, so rely on current information rather than what you read six months ago.

The terminology overlap is real. Some banks call their rebate schemes “cashback” even when a manual claim is required. When in doubt, look at the process: if you have to submit anything, it is a rebate regardless of what the programme is called.

Maximising your savings in New Zealand

The single most powerful thing you can do is stack your sources. Combining credit card cashback, portal cashback, and card-linked offers multiplies your total reward because each source operates independently and pays out separately on the same transaction. A 1.5% credit card cashback combined with a 5% portal rate on a $300 purchase adds up to a $19.50 saving before you have done anything unusual.

To make stacking work consistently, you need a system:

- Keep a submissions tracker. A simple spreadsheet with columns for purchase date, rebate name, submission deadline, and expected payout date is enough to stay on top of multiple claims.

- Check programme fund status. Public rebate programmes can exhaust funds rapidly, especially around peak buying periods. Confirm the programme is still funded before you make a large purchase based on the expected rebate.

- Use dedicated cashback apps. Several apps available to New Zealand users aggregate portal rates, track pending rewards, and send reminders about expiring offers.

- Read the redemption terms carefully. Confirm whether your reward is paid in cash or points, whether there is a minimum threshold before you can withdraw, and whether the reward has an expiry date.

A real-world example: a New Zealand household buying a new washing machine for $1,200 through a cashback portal (earning 3%) while paying on a rewards credit card (earning 1%) and claiming a manufacturer rebate ($80) could recover $164 in total. That is nearly 14% back on a purchase most people treat as a flat expense. The difference between capturing that saving and missing it entirely comes down to organisation, not luck.

Pro Tip: Set a calendar reminder for every rebate submission deadline the moment you make a qualifying purchase. Rebate windows are notoriously short, and the saving is only real if you claim it.

Understanding cash flow fundamentals also helps here. Cashback and rebates are delayed inflows, so treating them as guaranteed income before they arrive creates budget problems. Track them as pending, not received.

Common pitfalls that cost people their rewards

Most lost rebates and cashback rewards come down to a handful of avoidable mistakes. Manual tracking is often the primary failure point, with complex eligibility criteria making organised records the difference between a successful claim and a missed saving.

Watch out for these specific traps:

- Missing submission windows. Rebate claim periods are often as short as 30 days. If you miss the window, the opportunity is gone permanently.

- Ad blockers and browser switching. Cashback portals track your purchase via a browser cookie. Using an ad blocker, switching devices mid-session, or opening a new tab after clicking the portal link breaks the tracking and forfeits the reward.

- Incomplete proof of purchase. A receipt that does not show the product model number or purchase date is frequently rejected. Always retain the original detailed receipt, not just the payment confirmation.

- Activation failures. Many card-linked offers require you to activate the deal in your banking app before the transaction. An unactivated offer pays nothing, even if you shopped at the right merchant.

- Excluded products. Programme terms routinely exclude sale items, clearance stock, or specific product lines. Scan the exclusions list before assuming your purchase qualifies.

- Ignoring reward expiry. Points and gift card rewards often expire within 12 months. Rewards that sit unclaimed past their expiry date are forfeited regardless of the effort you put into earning them.

The fix for most of these is straightforward. Screenshot the activated offer. Note the portal click. Keep receipts. Set reminders. The technology now exists to manage all of this through a single app, and using it properly shifts the odds firmly in your favour.

Stuart’s perspective on making these programmes actually work

In my experience working with New Zealand clients on their broader financial picture, rebates and cashback are the most consistently underused savings tools available. Not because people do not know they exist, but because the gap between signing up and reliably capturing rewards is wider than most people expect.

I have seen clients who were technically enrolled in three or four cashback programmes but had never successfully redeemed a single reward. The culprit was almost always the same: no system. They activated offers occasionally, forgot to click through the portal, and let rebate deadlines slide. The programmes were fine. The process was broken.

What I have found actually works is treating your cashback and rebate activity like you would a small recurring bill. You schedule it, track it, and follow up on it. Fifteen minutes once a fortnight to check pending rewards, log new purchases, and submit any outstanding claims is enough to capture the majority of what you are owed.

The other thing worth saying plainly: do not let the pursuit of cashback and rebates drive poor purchasing decisions. A 5% cashback on something you did not need is still a net loss. The financial benefit only materialises when rewards are earned on spending you would have done anyway.

For New Zealanders looking at paying off their home loan faster, directing cashback rewards directly to your mortgage is one of the most effective low-effort ways to reduce interest over time. Small, consistent additional payments compound meaningfully over the life of a loan.

— Stuart

How Mortgagemanagers helps you make more of your money

Rebates and cashback are one piece of a larger financial puzzle. Getting the most from them means understanding how they fit alongside your mortgage, your budget, and your long-term goals.

At Mortgagemanagers, our Auckland-based mortgage advisers help New Zealanders across the North Shore, West Auckland, and beyond understand not just home loans, but the full range of financial tools available to them, including bank-run cashback offers on new mortgages that many borrowers never think to ask about. Some lenders offer cashback incentives worth thousands of dollars when you take out or refinance a home loan. Knowing which ones, and whether they suit your situation, is exactly where a good adviser earns their keep. If you want guidance tailored to your circumstances, reach out to the team at Mortgagemanagers today.

FAQ

What is the difference between a rebate and cashback?

A rebate requires you to pay full price and submit a manual claim for a partial refund, while cashback is calculated automatically as a percentage of your transaction and credited after the purchase clears. Both are post-purchase rewards, but rebates involve more steps on your part.

How long does cashback take to appear?

Cashback typically takes between 1 and 90 days to appear on your account, depending on the programme. The delay exists because most platforms hold the reward during the merchant’s standard return window.

Can I stack cashback from multiple sources?

Yes. Credit card cashback, portal rewards, and card-linked offers operate independently, meaning you can earn from all three on the same purchase without one reducing another.

Why is my cashback paid in points instead of cash?

Many programmes pay rewards in points, store credits, or gift cards rather than transferable cash. Always verify redemption terms before committing to a programme so you know exactly what form your reward will take.

What happens if a government rebate programme runs out of funds?

Public rebate programmes can exhaust their budgets mid-cycle and stop accepting new claims. Always confirm a programme is still funded before making a purchase based on an expected rebate payment.