TL;DR:

- Choosing between fixed and floating rates in New Zealand depends on your financial plans, risk tolerance, and property timeline. Fixed rates offer payment certainty and protect against rate rises, but may incur substantial break fees if you need to exit early, while floating rates provide flexibility with higher costs embedded in the rate. Most borrowers benefit from split loans that balance security and adaptability, emphasizing the importance of active review and personalized advice before locking in a rate.

Most people assume the cheapest-looking rate is the right rate. When it comes to fixed vs floating rates explained in the New Zealand context, that assumption can cost you thousands. The real question is not which rate is lower today, but which structure fits your life. Your plans to sell, refinance, or make lump-sum repayments matter just as much as the number on the rate sheet. This guide walks you through both options clearly, covers actual 2026 NZ rate figures, and gives you a practical framework to choose with confidence.

Table of Contents

- Key takeaways

- What fixed and floating rates actually mean

- Fixed vs floating: trade-offs, costs, and risks

- The 2026 NZ rate environment

- Choosing the right rate structure for your situation

- When fixed or floating makes the most sense

- Stuart’s take on choosing well

- How Mortgagemanagers can help you choose

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Fixed rates offer certainty | Your repayments stay the same for your chosen term, protecting you from rate rises. |

| Floating rates offer flexibility | You can repay extra or refinance at any time without facing break fees. |

| Break fees can be significant | Exiting a fixed rate early may cost thousands if wholesale rates have fallen since you fixed. |

| Floating rates carry a premium | In 2026, floating rates sit roughly 1%–2% higher than comparable short-term fixed rates. |

| Split loans balance both worlds | Many NZ borrowers split their loan to gain both payment certainty and flexible repayment options. |

What fixed and floating rates actually mean

Understanding fixed rates starts with one core idea: predictability. When you take a fixed-rate home loan, your interest rate is locked in for a set term with repayments that do not change during that period. In New Zealand, fixed terms typically run from 6 months up to 5 years, with 1-year and 2-year terms being the most popular among Kiwi borrowers.

Floating rates work differently. Your interest rate moves up or down as market conditions change, and floating rates usually adjust within 1 to 2 weeks of a Reserve Bank of New Zealand Official Cash Rate (OCR) decision. This means if the OCR drops, your rate and repayments can fall quickly. The reverse is equally true.

What drives these rates behind the scenes matters too. Fixed rates are not simply tied to the current OCR. Instead, fixed-rate pricing reflects future expectations via wholesale swap markets, which means they can shift independently of what the Reserve Bank decides this month. Floating rates, by contrast, are more directly linked to the OCR and bank funding costs.

Here is a snapshot of indicative NZ mortgage rates in 2026:

| Rate type | Indicative rate (2026) |

|---|---|

| Floating | ~6.99%–7.09% |

| 6-month fixed | ~6.29% |

| 1-year fixed | ~5.55% |

| 2-year fixed | ~5.39% |

| 3-year fixed | ~5.59% |

| 5-year fixed | ~5.89% |

Note: These are indicative figures. Rates vary between lenders and change regularly.

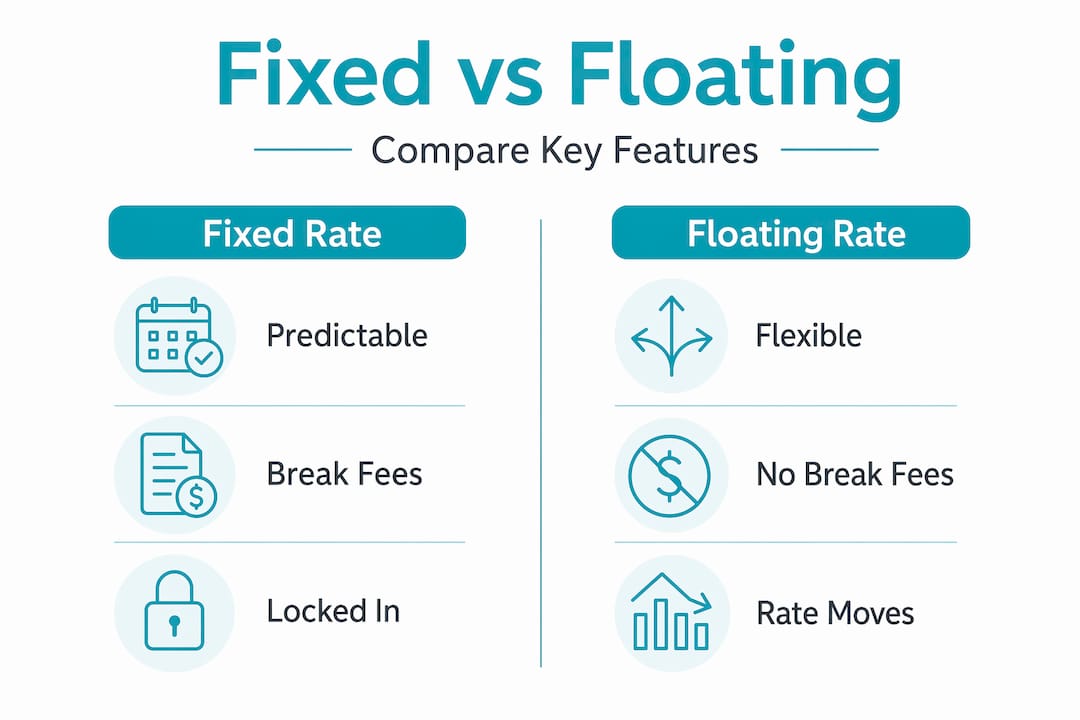

Fixed vs floating: trade-offs, costs, and risks

Here is a direct comparison of what each structure actually delivers:

| Feature | Fixed rate | Floating rate |

|---|---|---|

| Payment certainty | High. Repayments locked for the term. | Low. Repayments move with the OCR. |

| Flexibility | Low. Break fees apply for early exit. | High. Repay or refinance anytime. |

| Cost in 2026 | Generally lower rate. | Generally 1%–2% higher. |

| Best suited for | Budget certainty, long-term holders. | Lump-sum repayers, near-sale borrowers. |

| Break fees | Yes, can be substantial. | None. |

Break fees deserve more attention than most borrowers give them. When you exit a fixed-rate loan early, your bank calculates the fee based on the difference between your fixed rate and current wholesale rates for the remaining term. If rates have fallen since you locked in, that gap can mean a very large fee. If rates have risen, the fee is typically zero. This is not a small print detail. It is a real financial consequence that catches many borrowers off guard, particularly when property circumstances change unexpectedly. You can read more about how this plays out in practice with Auckland break fee examples.

Floating rates, by contrast, carry no break fee at all. That flexibility has a price attached to it, though, and that price shows up in the rate itself.

Pro Tip: If there is any chance you will sell, refinance, or receive a large inheritance or bonus within the next year or two, factor break fee exposure into your rate decision before you fix.

The 2026 NZ rate environment

The gap between fixed and floating rates is one of the most telling features of the current market. Floating rates sit roughly 1%–2% higher than comparable short-term fixed rates in 2026, reflecting what lenders charge for the flexibility premium embedded in floating products.

The Reserve Bank’s OCR reductions since 2023 have already begun feeding through into mortgage pricing, particularly at the shorter fixed-term end. One-year and two-year fixed rates have responded noticeably to these changes. Floating rates adjust quickly too, but because they carry that built-in premium, they remain more expensive day to day.

“Floating mortgages typically adjust quickly after OCR changes, while fixed rates reflect longer-term market expectations and shift less immediately.” — MoneyBalance Mortgage Rates 2026

This matters for your decision because if you believe rates will continue falling, you might assume floating is the smart play. The reality is more nuanced. Fixed rates at the shorter end already price in expected OCR cuts, so waiting for rates to drift down on a floating product may cost you more in the interim than simply locking in a low one-year or two-year rate now.

Rates also vary meaningfully between lenders. Two banks can offer different fixed rates for the same term on the same loan size. Shopping across lenders or working with a mortgage adviser who has access to multiple banks is one of the clearest ways to secure a better outcome.

Choosing the right rate structure for your situation

There is no single correct answer here, but there are clear decision factors that point you in the right direction.

-

Budget certainty. If your household runs on a tight monthly budget and a rate rise would genuinely strain your finances, a fixed rate removes that risk for the term you choose. Knowing your repayment amount for the next one to three years has real value.

-

Plans to sell or refinance. If you are likely to sell your home or switch lenders within the fixed term, you are exposed to break fees. The fixed vs variable interest decision shifts significantly if there is any near-term chance of exiting the loan.

-

Lump-sum repayments. Floating rates allow you to put extra money directly onto your mortgage at any time. This is a genuine floating rate benefit for borrowers who receive irregular income, bonuses, or commission. Borrowers planning large lump-sum repayments or early refinancing should favour floating or shorter fixed terms to avoid break fees erasing their savings.

-

Risk tolerance. Are you comfortable watching your repayments shift month to month? Some borrowers sleep better knowing their payment is fixed. Others prefer to ride rate movements and enjoy the upside when the OCR falls.

-

Split loans. Most NZ borrowers use a split loan structure, fixing one portion of the loan while leaving a smaller portion floating. This gives you repayment certainty on the bulk of your mortgage, while maintaining the freedom to make extra repayments or benefit from OCR cuts on the floating portion. It also staggers your refixing dates, so you are not renewing the entire loan at a potentially unfavourable time.

Pro Tip: When your fixed term approaches expiry, review rates 4 to 6 weeks early. You can often lock in a new rate before the current term ends, which protects you if rates rise in that window.

When fixed or floating makes the most sense

Pulling this together into a clearer picture, here is how different borrower situations generally align with each structure.

Fixed rates tend to suit borrowers who:

- Need payment certainty for household budgeting

- Plan to stay in the property for the full fixed term

- Are not expecting to make large extra repayments

- Want protection from potential rate rises over the next 1 to 3 years

Floating rates tend to suit borrowers who:

- Are planning to sell or refinance soon

- Receive irregular income and want to repay large sums without penalty

- Prefer to benefit immediately from OCR cuts without waiting for a fixed term to expire

- Have strong financial reserves and can absorb repayment variability

The cheapest mortgage option depends heavily on borrower behaviour during the fixed term. Large repayments or early exits can negate any savings from fixing at a lower rate. This is why understanding your own plans matters more than chasing the most attractive headline number.

Split loans remain a practical middle ground for most borrowers. They are not a compromise. For many Kiwi homeowners, they are the most thoughtful choice available, offering both protection and flexibility in a single structure.

Stuart’s take on choosing well

In my experience working with New Zealand borrowers, the biggest mistakes rarely come from picking the wrong rate type. They come from not thinking through the full term before signing. I have seen borrowers fix for three years because the rate looked appealing, only to sell 18 months later and face a break fee that wiped out all their savings from the lower rate. That is a painful and avoidable situation.

What I have found is that the floating rate vs fixed rate conversation is really a conversation about your financial timeline. Before you even look at the numbers, ask yourself honestly: do I know what my life will look like in two or three years? If the answer is “probably not,” shorter fixed terms or a split structure give you more room to adapt.

I also see borrowers overlook the value of reviewing their loan at fixed-term expiry rather than just rolling over on the bank’s default rate. Banks do not always offer their best rate at rollover. A proactive review, ideally with a mortgage adviser who can compare multiple lenders, regularly turns up better options. If you are curious about refinancing your NZ home loan, that review is often where the real savings are found.

My honest advice: do not treat rate selection as a set-and-forget decision. Treat it as something you revisit actively, with proper guidance.

— Stuart

How Mortgagemanagers can help you choose

Deciding between fixed and floating rates involves more than reading a comparison table. It involves your income patterns, your property plans, your risk comfort, and your lender options across the whole market.

At Mortgagemanagers, we work with borrowers across Auckland, West Auckland, the North Shore, and throughout New Zealand to make this decision clear and personal. As your mortgage advisers and personal shoppers, we compare rates from multiple banks, explain break fee exposure in plain language, and help you structure your loan in a way that actually matches how you live. Whether you want the certainty of a fixed term, the freedom of floating, or a split that gives you both, we will help you find the right fit. Reach out to the team at Mortgagemanagers to get started with advice that is tailored to your situation.

FAQ

What is the main difference between fixed and floating rates?

A fixed rate locks your interest and repayments for a set term, while a floating rate moves up or down with market conditions and the OCR. Fixed offers certainty; floating offers flexibility.

Why are floating rates higher than fixed rates in NZ?

Floating rates carry a flexibility premium because you can repay or exit the loan at any time without penalty. In 2026, floating rates are typically 1% to 2% higher than short-term fixed rates.

What are break fees and when do they apply?

Break fees apply when you exit a fixed-rate loan before the term ends. They are calculated based on the gap between your fixed rate and current wholesale rates for the remaining period, and can be substantial if rates have fallen since you fixed.

What is a split home loan?

A split loan divides your mortgage into a fixed portion and a floating portion, giving you repayment certainty on most of the loan while keeping flexibility on the rest for extra repayments or early payoff.

How do I know which rate type is right for me?

Your decision should be guided by your need for budget certainty, your plans to sell or refinance, and your ability to make lump-sum repayments. A mortgage adviser can help you weigh these factors against current market rates.