TL;DR:

- The debt-to-income ratio (DTI) measures the percentage of gross income used for recurring debt payments, determining mortgage eligibility. Lenders in New Zealand prefer a front-end ratio below 28% and a back-end ratio under 36%, but factors like savings and employment stability can offset higher DTIs. Improving DTI involves paying down debts, avoiding new credit, and documenting income accurately before applying.

If you have ever applied for a home loan and been puzzled by a lender’s questions about your debts and income, you have already encountered the debt-to-income ratio at work. This single financial measure, commonly abbreviated as DTI, carries enormous weight in whether your mortgage application succeeds or stalls. Understanding it before you walk into a bank or speak with a lender is one of the most practical steps you can take as a Kiwi buyer. This guide covers what DTI means, how to calculate yours accurately, what lenders in New Zealand look for, and what you can do to improve your position.

Table of Contents

- Key takeaways

- What is debt-to-income ratio and why does it matter?

- How to calculate debt-to-income ratio

- What is a good debt-to-income ratio for NZ loans?

- Common misconceptions about your DTI

- How to improve your DTI before applying

- My take on DTI and what it actually tells you

- How Mortgagemanagers can help with your DTI

- FAQ

Key takeaways

| Point | Details |

|---|---|

| DTI is a borrowing risk screen | It measures recurring debt payments as a percentage of gross monthly income, not take-home pay. |

| Two ratios matter | Front-end covers housing costs only; back-end covers all recurring debts combined. |

| NZ lenders use 28/36 benchmarks | Housing costs ideally below 28% and total debts below 36% of gross income. |

| Accuracy is non-negotiable | Using net income or including non-debt expenses will give you a misleading figure. |

| Improvement is possible | Paying down debt and avoiding new credit before applying can meaningfully lower your DTI. |

What is debt-to-income ratio and why does it matter?

The debt-to-income ratio definition is straightforward. It is the percentage of your gross monthly income that goes towards paying recurring debts. DTI measures your debt burden as two separate ratios: a front-end ratio covering housing-related costs, and a back-end ratio covering all your regular debt obligations combined.

The front-end ratio includes your mortgage or rent payment, property rates, and home insurance. The back-end ratio adds everything else on top, including credit card minimum payments, car loans, student loans, and any hire purchase agreements. The distinction between these two ratios matters because a lender looking at your housing affordability uses the front-end figure, while the full picture of your debt load comes from the back-end figure.

Why do lenders care so much about this number? Because higher DTI ties up more income in debt obligations, leaving less room to absorb unexpected costs like job loss, medical bills, or rising interest rates. Lenders use DTI alongside your credit score, income stability, and savings to form a complete risk profile. It is not the only factor, but it is consistently one of the first things assessed.

The importance of debt-to-income ratio goes beyond mortgage approval. Tracking your own DTI regularly gives you a clear, honest signal about your financial health. If more than a third of your gross income is already committed to debt repayments, adding a large mortgage on top is going to feel like wearing a financial straitjacket.

- Front-end DTI includes: mortgage or rent, property insurance, body corporate fees

- Back-end DTI adds: car loans, credit card minimums, student debt, personal loans, child support

- Not included: groceries, utilities, fuel, subscriptions, childcare

Pro Tip: If you are comparing your DTI to a friend’s, make sure you are both using gross income, not your after-tax pay. The gap between the two can be significant, and mixing them up produces figures that are nowhere near comparable.

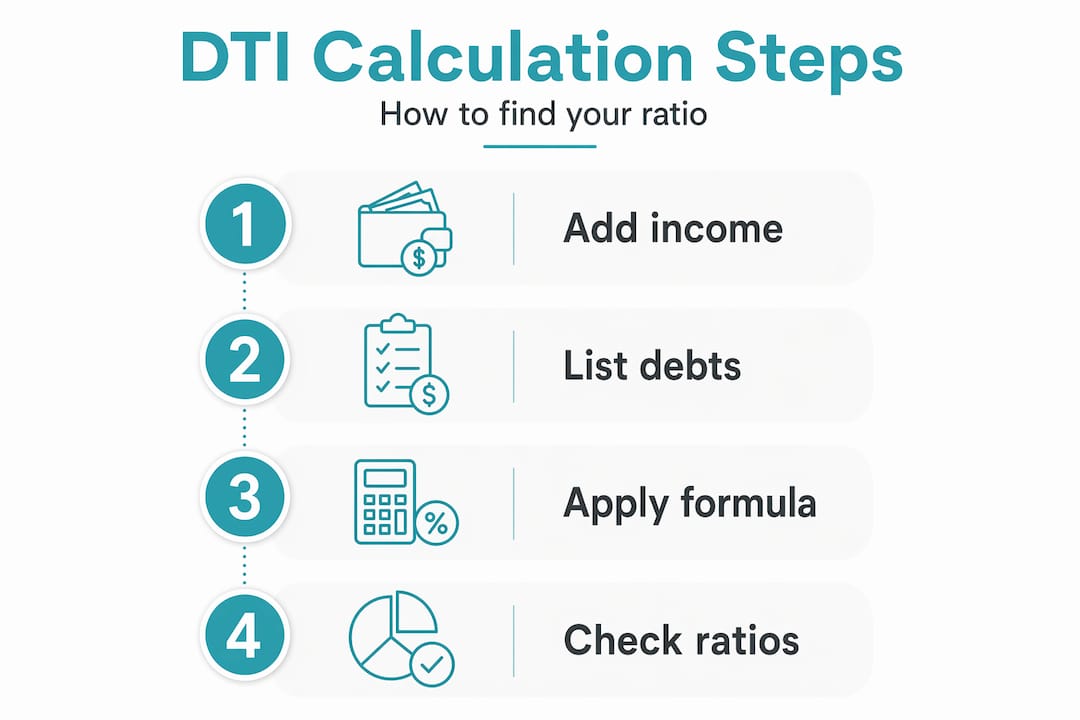

How to calculate debt-to-income ratio

Getting your DTI calculation right is critical, because lenders will run their own numbers and any gap between your estimate and theirs can create confusion or erode trust in your application. Here is how to do it properly.

Step 1: Add up your gross monthly income. This means income before tax. Include your salary, self-employment income (usually averaged over two years), rental income if applicable, and any regular bonuses your lender will accept as stable income. Do not use your bank account deposits as a proxy for this; they reflect net income after tax and KiwiSaver contributions.

Step 2: List every recurring debt obligation. Focus on minimum required monthly payments, not what you actually pay. Use gross income and minimum debt payments for this calculation, not estimates of your typical spending. Utilities, groceries, and childcare are excluded because DTI focuses on debts only, not living expenses.

Step 3: Apply the formula.

Total monthly debt payments ÷ Gross monthly income × 100 = DTI percentage

Step 4: Calculate both ratios. Run the formula once using only housing costs, then again with all recurring debts.

Here is a straightforward New Zealand example:

| Income and debt item | Monthly amount (NZD) |

|---|---|

| Gross monthly salary | $7,500 |

| Proposed mortgage repayment | $2,100 |

| Car loan minimum payment | $450 |

| Credit card minimum payment | $150 |

| Student loan repayment | $200 |

| Total monthly debts | $2,900 |

Front-end DTI: $2,100 ÷ $7,500 × 100 = 28%

Back-end DTI: $2,900 ÷ $7,500 × 100 = 38.7%

A DTI calculation like this shows this borrower is right on the edge of comfortable lending territory. You can also use an online payment calculator to help model different debt and income scenarios before you speak with a lender.

Pro Tip: Gather three months of payslips, your most recent tax return if self-employed, and statements for every loan and credit facility before you calculate your DTI. Lenders will ask for these documents anyway, and having them ready means your self-assessed figure will closely match what the lender calculates.

What is a good debt-to-income ratio for NZ loans?

New Zealand lenders generally follow benchmarks that will be familiar to anyone who has researched home loan eligibility. Lenders prefer housing costs below 28% of gross income and total debt obligations below 36%, though this is a guide rather than an absolute rule.

Here is how these thresholds translate across different lending scenarios:

| DTI range | Lender view | Likely outcome |

|---|---|---|

| Below 28% (front-end) | Strong position | Good access to competitive rates |

| 28 to 36% (back-end) | Acceptable | Approval likely with good credit and savings |

| 36 to 43% | Marginal | Increased scrutiny; compensating factors required |

| Above 43% | High risk | Approval unlikely without exceptional profile |

That said, DTI guidelines are not carved in stone. Borrowers with higher DTI may still receive approval if they present compensating factors. These might include:

- A large deposit (20% or more reduces lender risk considerably)

- Strong employment history and income stability

- Significant cash reserves beyond the deposit

- A co-borrower with a low individual DTI

- A clean credit history with no late payments or defaults

Every New Zealand lender sets its own credit policy, and what one bank declines, a non-bank lender or credit union may approve under different criteria. This is one reason working with a mortgage broker in NZ gives you genuine advantages. A broker knows which lenders are currently flexible on DTI thresholds and which are not.

Common misconceptions about your DTI

Many people arrive at a lender’s desk with a DTI figure that does not match what the lender calculates. The gap almost always comes from one of these mistakes.

Using net income instead of gross. If you earn $90,000 a year gross and calculate your monthly income as your fortnightly take-home pay doubled, you will underestimate your income and overstate your DTI. Always use gross income.

Including non-debt expenses. Your monthly grocery bill, power bill, and Netflix subscription are not debts. Irregular expenses are excluded from DTI so the ratio reflects stable, recurring obligations only. Including them pushes your DTI up artificially and gives you an unnecessarily alarming figure.

Forgetting the proposed mortgage payment. This is the most consequential mistake. New mortgage repayments are included in the back-end DTI during underwriting. If you calculate your current DTI without the prospective mortgage, you may feel comfortable, only to discover your ratio jumps 15 percentage points once the new loan payment is factored in.

Assuming DTI is the only thing lenders check. DTI is a risk screen, not a final verdict. Your credit score shapes your home loan alongside DTI, as do your savings, employment type, and the size of your deposit.

Pro Tip: Run your DTI calculation twice: once with your current debts and once with the proposed mortgage included. The second figure is what the lender will actually use, so it is the number you want to feel confident about before you apply.

How to improve your DTI before applying

If your back-end DTI sits above 36%, you still have real options. Improving your ratio before you apply can make the difference between a straight approval and a difficult conversation.

-

Pay down high-balance debts first. Credit card balances carry the highest interest and the minimum payments add up quickly. Reducing a card from $8,000 to $2,000 could drop your monthly minimum payment by $180 or more, directly lowering your DTI. Read more about debt repayment strategies tailored to NZ homeowners.

-

Consolidate loans where it makes sense. Merging two or three smaller loans into a single personal loan with a lower combined payment can reduce your monthly obligations. Be cautious here though. Extending your loan term to lower the payment may help your DTI now but costs more in interest over time.

-

Avoid opening new credit. A new car loan or credit card in the months before your mortgage application increases your debt obligations and can also trigger a credit enquiry that temporarily lowers your credit score. Hold off on any new borrowing.

-

Increase your documented income. If you have a second income stream, make sure it is documented and consistent enough for lenders to accept it. Two years of self-employment income records, for example, or a rental property with a lease agreement, can strengthen your income side of the equation.

-

Check your home loan eligibility before you set your property budget. Many buyers work backwards from a property price. Working forwards from your actual financial position, including your DTI, sets far more realistic expectations and avoids heartbreak at the finish line.

My take on DTI and what it actually tells you

I have worked with hundreds of New Zealanders preparing for home loan applications, and the one thing I wish I could say to every single one of them upfront is this: your DTI is a useful compass, but it is not the full map.

Too many applicants fixate on whether their DTI passes a threshold, and in doing so they miss the bigger question: does their overall financial position tell a story a lender wants to hear? I have seen clients with a 38% DTI sail through because they had 18 months of living expenses saved and a long, stable employment history. I have also seen clients with a 33% DTI struggle because their income was inconsistent and their credit file had a few blemishes.

The compensating factors lenders consider are real and they matter. A large deposit, stable income, low credit utilisation, and a clean repayment history can offset a DTI that sits slightly above the preferred range. Knowing which levers to pull, and how to present your financial profile in the strongest light possible, is where a mortgage adviser earns their value. Anyone can run a formula. A good adviser knows how to read what it actually means for your specific situation.

My advice? Use DTI as one tool in your financial readiness kit. Know your number, understand what moves it, and then get a professional to help you interpret it within the full context of your application.

— Stuart

How Mortgagemanagers can help with your DTI

Knowing your DTI is a strong start. Knowing what to do with that number is where most people benefit from professional guidance.

At Mortgagemanagers, we work with Kiwi buyers every day to assess their financial position honestly and build a home loan strategy that gives them the best possible chance of approval. Whether you are a first-time buyer trying to understand your DTI for the first time, or a property investor looking to optimise your borrowing capacity, our team of Auckland-based mortgage advisers is here to help. We strongly recommend getting mortgage advice early before you begin your property search. Understanding your DTI before you fall in love with a property means you search with confidence, not guesswork. Our advisers act as your personal shoppers for a home loan, comparing options across multiple lenders to find terms that suit your actual financial position. Reach out to Mortgagemanagers today for a no-obligation conversation.

FAQ

What does debt-to-income ratio mean?

Debt-to-income ratio (DTI) is the percentage of your gross monthly income used to cover recurring debt payments. It includes two measures: a front-end ratio for housing costs and a back-end ratio for all debts combined.

What is a good DTI ratio in New Zealand?

Most NZ lenders prefer a front-end DTI below 28% and a total back-end DTI below 36%. Ratios above 43% generally make approval difficult without strong compensating factors like a large deposit or stable income.

Does DTI include utilities and groceries?

No. DTI covers recurring debt obligations only, such as loan repayments and credit card minimums. Living expenses like utilities, food, and childcare are excluded from the calculation.

How does DTI affect mortgage approval?

DTI influences loan approvals and interest rates by signalling how much financial capacity you have after meeting existing debts. A lower DTI improves your chances of approval and access to competitive rates.

Can I get a mortgage with a high DTI?

Yes, in some cases. Applicants with compensating factors such as significant savings, reliable income, or a larger deposit may still qualify. Speaking with a mortgage adviser helps you understand your realistic options.