TL;DR:

- The Loan-to-Value Ratio (LVR) indicates the percentage of a property’s value borrowed through a mortgage and influences borrowing limits and interest rates in New Zealand. The Reserve Bank (RBNZ) uses LVR restrictions to manage systemic lending risk, with thresholds varying for owner-occupiers and investors. Managing your deposit size, timing, and working with a mortgage adviser can help optimize your LVR and improve loan approval chances.

The Loan-to-Value Ratio (LVR) is defined as the percentage of a property’s value that you borrow through a mortgage, and it is one of the most consequential numbers in any New Zealand home loan application. Whether you are a first-home buyer in Auckland or an investor adding to your portfolio, your LVR determines how much you can borrow, what interest rate you will pay, and whether a bank will approve your loan at all. The Reserve Bank of New Zealand (RBNZ) uses LVR as a core macroprudential tool to manage lending risk across the entire banking system, making it far more than just a personal finance calculation.

What is LVR and how does it work in New Zealand?

LVR, or Loan-to-Value Ratio, is the ratio between your home loan amount and the lender’s assessed value of the property, expressed as a percentage. A lower LVR signals less risk to the lender because you have more equity in the property from the outset. A higher LVR means you are borrowing a larger share of the property’s value, which lenders treat as a greater financial risk. The RBNZ sets LVR restrictions that govern how much high-LVR lending banks can offer across their entire loan portfolios, not just to individual borrowers.

Understanding LVR is your first step toward making confident, well-informed decisions about property finance in New Zealand. It shapes your deposit target, your loan approval prospects, and the total cost of your mortgage over time. For first-home buyers especially, getting clarity on this single number can remove a great deal of uncertainty from the process.

How to calculate LVR for your home loan

The LVR formula is straightforward: divide your loan amount by the property value, then multiply by 100 to get a percentage.

Here is how the calculation works step by step:

- Identify the property value. This is the lender’s valuation, not necessarily the purchase price or the listing price you saw online.

- Determine your loan amount. Subtract your deposit from the purchase price to find how much you need to borrow.

- Apply the formula. Divide the loan amount by the property value, then multiply by 100.

- Interpret the result. An LVR below 80% is generally considered low risk for owner-occupiers. Above 80% moves you into high-LVR territory.

To make this concrete: if you are buying a home valued at $800,000 and you have a $160,000 deposit, your loan amount is $640,000. Dividing $640,000 by $800,000 gives 0.80, which multiplied by 100 equals an LVR of 80%. Sit just above that, say borrowing $680,000 on the same property, and your LVR climbs to 85%, placing you in a different lending category entirely.

One detail many buyers overlook is that banks use their own lender’s appraisal valuation, not the price you agreed to pay. If you offer $820,000 for a property the bank values at $780,000, your LVR is calculated on $780,000. That gap can push your LVR higher than you planned, potentially affecting your approval or your interest rate.

Pro Tip: Before making an offer on a property, ask your mortgage adviser to run an estimated LVR based on a conservative valuation. This protects you from a valuation shortfall that could change your borrowing position at the last moment.

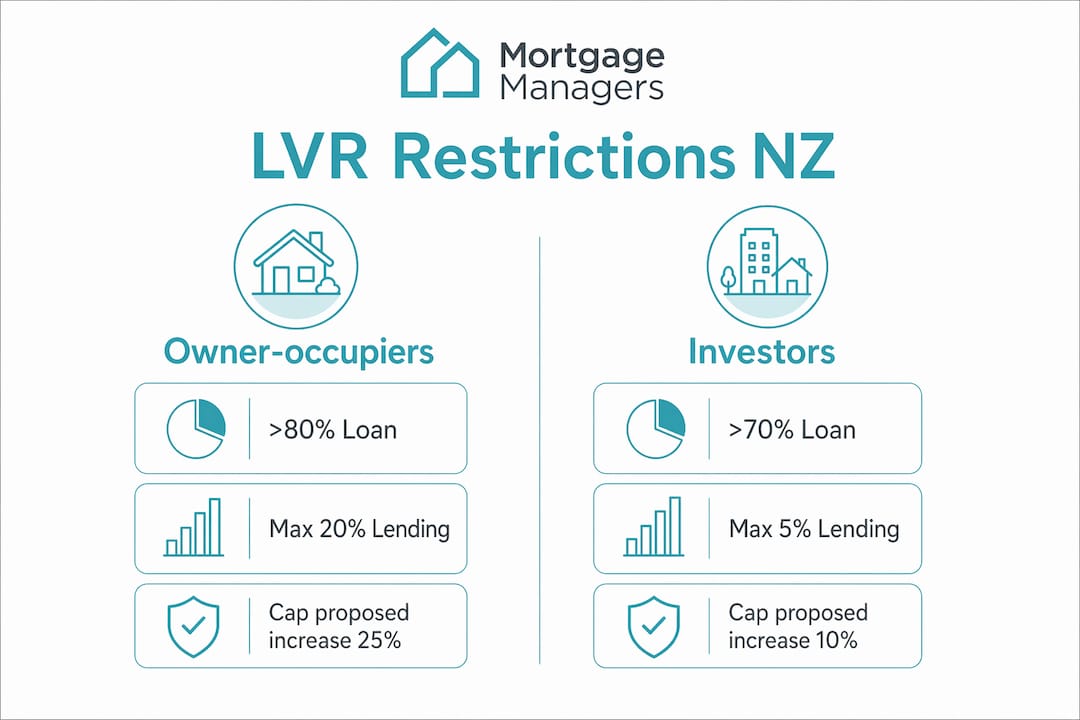

What are the current NZ LVR restrictions for buyers and investors?

The RBNZ applies LVR restrictions as portfolio-wide lending caps across the banking system, often described as “speed limits.” These are not outright bans on low-deposit lending. They limit how much of a bank’s new lending can fall into the high-LVR category over a set period, typically three or six months.

The current settings differ significantly between owner-occupiers and investors:

| Borrower type | High-LVR threshold | Maximum share of new lending |

|---|---|---|

| Owner-occupier | Above 80% LVR | 25% of new lending |

| Residential investor | Above 70% LVR | 10% of new lending |

For owner-occupiers, a loan is classified as high-LVR above 80%, and banks can direct up to 25% of their new lending to these borrowers. Investors face a stricter threshold. Any investor loan above 70% LVR is considered high-LVR, and banks are limited to just 10% of new lending in this category. This reflects the RBNZ’s view that investment lending carries greater systemic risk.

These restrictions apply only to new residential mortgage lending and are not applied retrospectively to existing loans. If you already have a mortgage, your current LVR does not trigger any regulatory action on the bank’s part.

“Easing LVR limitations while maintaining debt-to-income restrictions can improve credit access and market efficiency for borrowers.” — Reserve Bank of New Zealand via RNZ News

The RBNZ has recently proposed raising the owner-occupier cap from 20% to 25% and the investor cap from 5% to 10%. These changes are designed to give banks more flexibility to lend, particularly to first-home buyers who may have smaller deposits. You can read more about what these shifts mean in practice in this analysis of LVR restriction changes.

How does LVR affect your interest rate and deposit?

Your LVR directly shapes the cost and accessibility of your home loan. The practical consequences are significant and worth understanding before you set your deposit target.

- Interest rate pricing. Loans above 80% LVR often attract higher interest rates because lenders price in the additional risk of a smaller equity buffer. Even a modest rate difference compounds substantially over a 25 or 30-year mortgage term.

- Lenders mortgage insurance (LMI). High-LVR borrowers may be required to pay LMI, which protects the lender, not you, if you default. This cost is typically added to your loan, increasing your total debt.

- Loan approval likelihood. Borrowers above 80% LVR face tighter lender scrutiny. Banks assess income, expenses, and credit history more rigorously when the deposit is small, because the margin for error is narrower.

- Deposit size expectations. For owner-occupiers, a 20% deposit keeps you at exactly 80% LVR, the threshold below which most standard lending conditions apply. For investors, a 30% deposit is the equivalent benchmark, keeping LVR at or below 70%.

- Investor versus owner-occupier treatment. Investors face a lower high-LVR threshold and a tighter lending cap, meaning the deposit requirement is effectively higher for investment properties than for a home you plan to live in.

Consider two borrowers both purchasing $700,000 properties in Auckland. One has a $140,000 deposit (20% LVR of 80%), the other has $84,000 (12% LVR of 88%). The second borrower sits in high-LVR territory, likely faces a higher interest rate, and may need to pay LMI. Over a 30-year loan, that difference in rate and insurance cost can amount to tens of thousands of dollars.

Pro Tip: If your deposit puts you just above 80% LVR, it may be worth delaying your purchase by a few months to save the additional amount needed to cross below that threshold. The interest savings and reduced fees can outweigh the cost of waiting.

What steps can you take to manage LVR limits when buying property?

LVR restrictions are a real constraint, but they are not immovable. There are practical steps you can take to improve your position before and during the loan application process.

- Grow your deposit deliberately. Every additional dollar saved reduces your LVR. Setting a specific deposit target tied to a property price range gives you a clear savings goal rather than an abstract number.

- Time your application strategically. Because LVR caps are portfolio-wide speed limits, two borrowers with identical deposits can receive different outcomes depending on how much high-LVR lending a particular bank has already issued in that period. Applying earlier in a lending cycle, or approaching multiple lenders, can improve your chances.

- Work with a mortgage adviser. A qualified mortgage adviser knows which lenders have capacity for high-LVR lending at any given time. They can also identify whether you qualify for any exemptions, such as new build lending, which sometimes carries different LVR treatment. Mortgagemanagers specialises in exactly this kind of guidance for Auckland and New Zealand buyers.

- Understand the impact of valuation outcomes. If a bank’s valuation comes in below your purchase price, your LVR rises. Knowing this risk in advance allows you to negotiate the purchase price, increase your deposit, or choose a different property.

- Explore alternative lending pathways. If high-LVR lending is restricted at major banks, non-bank lenders may offer options, though typically at higher interest rates. A mortgage adviser can help you weigh whether this is appropriate for your situation.

For a detailed look at how LVR affects first-home buyers in NZ, Mortgagemanagers has put together specific guidance tailored to that audience.

Key takeaways

Your LVR is calculated by dividing your loan amount by the lender’s property valuation and multiplying by 100, and keeping it at or below 80% for owner-occupiers is the single most effective way to access better loan terms in New Zealand.

| Point | Details |

|---|---|

| LVR definition | LVR is your loan amount divided by the property value, expressed as a percentage. |

| Owner-occupier threshold | Loans above 80% LVR are classified as high-LVR, with banks capped at 25% of new lending in this category. |

| Investor threshold | Investor loans above 70% LVR are high-LVR, with banks limited to just 10% of new lending here. |

| Valuation matters | Banks use their own valuation, not the purchase price, so a shortfall can raise your LVR unexpectedly. |

| Timing and strategy | LVR caps are portfolio-wide speed limits, so timing your application and using a mortgage adviser can improve your outcome. |

LVR in New Zealand: what I have seen working with borrowers

Having worked with homebuyers and investors across Auckland and wider New Zealand for many years, the most consistent challenge I see is not that people do not understand LVR. It is that they underestimate how much the bank’s valuation can diverge from the purchase price, especially in a market where buyers are competing hard and sometimes paying above what the numbers support.

The RBNZ’s balancing act is genuinely difficult. Tighten LVR restrictions too much and you lock first-home buyers out of the market. Ease them too far and you risk the kind of overleveraged lending that creates fragility across the whole system. The recent proposal to raise the owner-occupier high-LVR share to 25% is a measured step, and I think it will make a real difference for buyers who are close to the 20% deposit mark but not quite there.

What I tell every borrower is this: your LVR is not fixed. It is a number you can influence through your deposit size, your property choice, and the timing of your application. The borrowers who get the best outcomes are the ones who treat LVR as a planning tool, not just a hurdle. If you are unsure where you stand, the right conversation to have is with a mortgage adviser who knows the current lending environment, not just the rulebook.

How Mortgagemanagers can help you work with LVR

LVR rules can feel like a moving target, particularly when bank lending caps shift throughout the year and valuations do not always align with what you have agreed to pay. Mortgagemanagers is a locally owned mortgage advisory business based in Hobsonville, Auckland, with advisers who work across West Auckland, the North Shore, and remotely throughout New Zealand. The team understands the current LVR environment and knows which lenders have capacity for your situation right now.

Whether you are a first-home buyer working toward that 20% deposit or an investor managing a 30% threshold, speaking with a mortgage adviser who can compare options across multiple lenders is the most direct way to improve your loan outcome. You can also connect directly with Auckland mortgage brokers at Mortgagemanagers to get personalised support tailored to your deposit, property goals, and timeline.

FAQ

What is LVR in simple terms?

LVR stands for Loan-to-Value Ratio and is the percentage of a property’s value that you borrow through a mortgage. A $400,000 loan on an $800,000 property equals an LVR of 50%.

What LVR do I need to avoid high-LVR restrictions in New Zealand?

Owner-occupiers need an LVR at or below 80% to avoid high-LVR classification, while residential investors need to stay at or below 70% under current RBNZ rules.

Does a high LVR mean my loan will be declined?

Not necessarily. Banks can still lend at high LVR, but they are limited in how much of their new lending can fall into that category. Your application may be approved depending on the bank’s current lending position and your overall financial profile.

Why does the bank use its own valuation instead of the purchase price?

Banks use their own appraisal valuation to protect against overpaying in a competitive market. If the bank values the property lower than your purchase price, your LVR is calculated on the lower figure, which can affect your approval and interest rate.

Can a mortgage adviser help me get a loan with a high LVR?

Yes. A mortgage adviser can identify which lenders currently have capacity for high-LVR lending, assess whether you qualify for any exemptions, and structure your application to give you the best possible chance of approval.