Over 40% of new home buyers in New Zealand rely on some form of low deposit mortgage, highlighting just how tough saving a full deposit has become. As australian property prices continue to influence housing trends across the region, many buyers are searching for flexible ways to break into the market. This guide sheds light on low deposit mortgage options in New Zealand, offering clear insights on eligibility, lender choices, and what potential borrowers must weigh before applying.

Table of Contents

- Defining Low Deposit Mortgages In Nz

- Eligibility Criteria And Deposit Requirements

- How Lvr Rules Affect Borrowers

- Lender Options And Loan Types Available

- Costs, Risks And Mortgage Insurance Explained

- Common Challenges And Mistakes To Avoid

Key Takeaways

| Point | Details |

|---|---|

| Low Deposit Options | Borrowers can access mortgages with deposits as low as 5%, which helps many first-home buyers enter the property market more easily. |

| Eligibility Criteria | Strong income proof, good credit history, and specific financial assessments are crucial for qualifying for low deposit mortgages. |

| LVR Regulations | Recent changes to Loan-to-Value Ratio rules have increased options for borrowers with smaller deposits, influencing borrowing capacity and accessibility. |

| Financial Risks | Lower deposits often involve higher interest rates and mandatory lenders mortgage insurance, increasing the overall cost of borrowing. |

Defining Low Deposit Mortgages in NZ

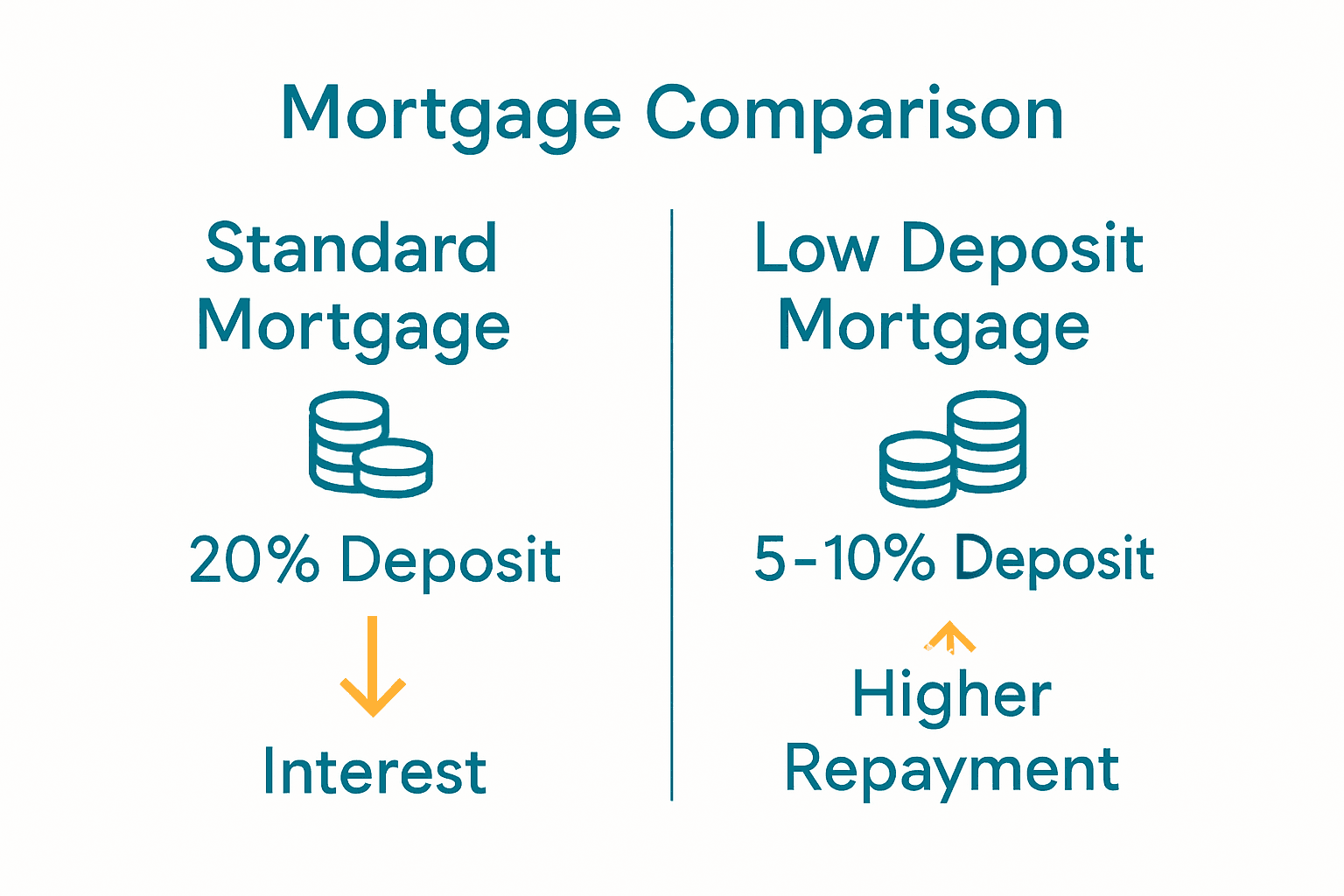

A low deposit mortgage represents a home loan option that allows borrowers to purchase property with a smaller upfront financial commitment than traditional lending requirements. According to Consumer.org.nz, first-home buyers in New Zealand typically need a deposit equal to at least 20% of the house value, though some lenders offer alternative pathways.

In practical terms, a low deposit mortgage enables potential homeowners to enter the property market with a deposit significantly lower than the standard 20% threshold – often ranging between 5% to 15%. These specialised home loans recognise that saving a substantial deposit can be challenging, especially for first-time buyers or those with limited savings. Lenders providing these mortgages will usually require additional risk mitigation strategies, such as lenders mortgage insurance or guarantor support, to offset the reduced initial investment.

The key characteristics of low deposit mortgages in New Zealand include:

- Deposits as low as 5-10% of property value

- Higher interest rates compared to standard mortgages

- Potential requirement for lenders mortgage insurance

- Stricter lending criteria and more comprehensive financial assessments

By understanding these specialised lending products, aspiring homeowners can explore more flexible pathways into property ownership. Our low deposit home loans guide provides comprehensive insights into navigating these unique mortgage options and understanding the potential opportunities and challenges they present.

Eligibility Criteria and Deposit Requirements

Navigating the eligibility landscape for low deposit mortgages in New Zealand requires understanding specific lending criteria and financial requirements. According to Kāinga Ora, the First Home Loan programme allows eligible first-home buyers to purchase a property with a deposit as low as 5%, subject to meeting stringent income and house price restrictions.

Financial institutions typically assess several key factors when evaluating low deposit mortgage applications. These include personal income, credit history, employment stability, existing financial commitments, and overall borrowing capacity. ANZ notes that while they generally recommend a 20% deposit, some lenders offer alternative pathways for borrowers with smaller upfront investments.

The core eligibility requirements for low deposit mortgages generally encompass:

- Proof of stable income and employment

- Clean credit history

- Demonstrated ability to service mortgage repayments

- Meeting specific income thresholds

- Purchasing a property within prescribed price limits

To successfully qualify for a low deposit mortgage, potential borrowers must prepare comprehensive documentation and demonstrate strong financial discipline.

Our guide on getting a home loan with a 5% deposit provides additional insights into navigating these specialised lending options and improving your approval chances.

Our guide on getting a home loan with a 5% deposit provides additional insights into navigating these specialised lending options and improving your approval chances.

How LVR Rules Affect Borrowers

Loan-to-Value Ratio (LVR) rules represent a critical mechanism through which financial regulators control lending practices and manage housing market risks. According to Reuters, the Reserve Bank of New Zealand introduced significant regulatory changes in May 2024, simultaneously easing existing LVR restrictions while implementing new constraints on housing finance to manage overall market stability.

These LVR regulations directly impact borrowers by determining how much they can borrow relative to a property’s value. Essentially, LVR rules mandate the minimum deposit required for home purchases, which traditionally meant most lenders demanded a 20% deposit. However, recent regulatory shifts are creating more flexible lending environments. Reuters reports that by December 2025, banks will be permitted to issue up to 25% of new loans to owner-occupiers with deposits under 20%, expanding opportunities for first-home buyers and property investors.

Key implications of LVR rules for borrowers include:

- Determines maximum borrowing capacity

- Influences interest rates and lending criteria

- Impacts first-home buyer accessibility

- Helps manage overall financial system risk

- Provides safeguards against potential market volatility

Understanding these evolving regulations is crucial for potential homeowners. Our guide on LVR restriction changes offers deeper insights into how these rules might affect your home-buying journey and financial planning strategies.

Lender Options and Loan Types Available

Navigating the low deposit mortgage landscape in New Zealand involves understanding the diverse array of lenders and loan products designed to support home buyers with limited upfront capital. Different financial institutions offer varying approaches to low deposit lending, ranging from traditional banks to specialised mortgage providers, each with unique eligibility criteria and loan structures.

The primary lender categories for low deposit mortgages typically include registered banks, credit unions, non-bank financial institutions, and government-supported programmes. These lenders offer multiple loan types tailored to different borrower scenarios, such as fixed-rate mortgages, floating-rate options, interest-only loans, and specialised first-home buyer products. Some institutions provide more flexible lending criteria for low deposit applicants, recognising the challenges faced by first-time homeowners in accumulating substantial savings.

Key loan types available for low deposit borrowers encompass:

- Floating rate mortgages

- Fixed-rate mortgages

- Split-rate mortgages

- Interest-only loans

- First-home buyer specific loans

- Government-assisted mortgage programmes

To gain comprehensive insights into the nuanced world of mortgage lending, our guide to home loan types offers an in-depth exploration of the various options available to New Zealand home buyers seeking low deposit mortgage solutions.

Costs, Risks and Mortgage Insurance Explained

Low deposit mortgages come with unique financial considerations that potential borrowers must carefully evaluate before committing to a home loan. According to Insights, when borrowing with less than a 20% deposit, homeowners typically incur Lenders Mortgage Insurance (LMI), which can significantly increase the overall cost of the loan by protecting the lender in case of borrower default.

The primary risks associated with low deposit mortgages extend beyond additional insurance costs. These loans often attract higher interest rates, reflecting the increased financial risk perceived by lenders. Borrowers must be prepared for potentially steeper monthly repayments and more stringent lending criteria. The reduced equity buffer means homeowners are more vulnerable to market fluctuations, potentially facing negative equity scenarios if property values decline.

Key financial considerations for low deposit mortgage borrowers include:

- Higher interest rates compared to standard mortgages

- Mandatory lenders mortgage insurance costs

- Increased monthly repayment amounts

- Greater exposure to market value fluctuations

- Potential limitations on future borrowing capacity

- Additional administrative and processing fees

To navigate these complex financial waters effectively, our mortgage protection cover guide offers comprehensive insights into managing the financial risks associated with low deposit home loans.

Common Challenges and Mistakes to Avoid

Navigating low deposit mortgages requires strategic financial planning and a comprehensive understanding of potential pitfalls. Canstar highlights that borrowers with limited deposits face significant challenges, including higher interest rates, additional fees like low equity premiums, and mandatory lenders mortgage insurance that can substantially increase overall borrowing costs.

Many first-time buyers inadvertently compromise their mortgage applications by overlooking critical financial preparation steps. Common mistakes include failing to thoroughly review credit histories, neglecting to build a robust savings track record, and underestimating the comprehensive financial assessment conducted by lending institutions. Borrowers often rush into applications without understanding the long-term implications of reduced deposit mortgages, potentially exposing themselves to higher financial risks and more restrictive lending conditions.

Key challenges and mistakes to avoid include:

- Neglecting to improve credit score before application

- Failing to save a consistent financial buffer

- Overlooking additional fees and insurance costs

- Underestimating ongoing mortgage maintenance expenses

- Not comparing multiple lender options

- Misunderstanding loan-to-value ratio implications

- Ignoring potential future income fluctuations

To develop a strategic approach to low deposit lending, our mortgage protection cover guide provides essential insights for navigating the complex landscape of home loan applications with minimal financial risk.

Take Control of Your Homeownership Journey with Expert Low Deposit Mortgage Support

Entering the New Zealand property market with a low deposit can seem overwhelming. Challenges such as meeting eligibility criteria, navigating complex LVR rules and managing the higher costs including lenders mortgage insurance create uncertainty. If the idea of securing a home loan with only 5 to 10 percent deposit feels daunting, Mortgage Managers is here to help. Our team of Auckland mortgage advisers understands the emotional weight of these hurdles and the need for a clear, personalised pathway.

Benefit from our expert guidance as we help you explore your options, improve your application strength and avoid costly mistakes. Whether you are a first-home buyer or looking to secure flexible lending solutions, start your journey today with reliable advice. Discover how we make low deposit home loans more accessible and achievable at Mortgage Managers. For detailed tips on managing mortgage risks, also check our mortgage protection cover guide and learn about getting a home loan with a 5% deposit. Take the first step now and turn your homeownership goals into reality.

Frequently Asked Questions

What is a low deposit mortgage?

A low deposit mortgage allows borrowers to purchase property with a smaller upfront investment, typically between 5% to 15% of the property’s value, compared to the traditional 20% deposit requirement.

What are the eligibility criteria for low deposit mortgages?

Eligibility usually includes proof of stable income, a clean credit history, demonstrated ability to service mortgage repayments, and meeting specific income and property price thresholds set by lenders.

What is Lenders Mortgage Insurance (LMI), and do I need it?

Lenders Mortgage Insurance is required when borrowing with a deposit of less than 20%. It protects the lender in case of borrower default and can significantly increase the overall cost of the loan.

What are the common mistakes to avoid when applying for a low deposit mortgage?

Common mistakes include neglecting to improve credit score, overlooking additional fees, underestimating ongoing mortgage expenses, and failing to compare options from multiple lenders.