TL;DR:

- In New Zealand, break fees are charges applied when borrowers repay or refinance fixed-rate mortgages early to compensate lenders for financial losses. These fees depend on remaining loan balance, rate differential, and time left, and are only accurately known through a lender’s direct quote. Proper planning, timing, and professional advice help borrowers manage or avoid these costs effectively.

A break fee is a charge applied by New Zealand lenders when you repay or refinance a fixed-rate mortgage before the agreed term ends, compensating the bank for its actual financial loss. Known formally as an Early Repayment Adjustment (ERA) or Early Repayment Charge (ERC), this cost catches many borrowers off guard. The Credit Contracts and Consumer Finance Act (CCCFA) governs how lenders calculate and disclose these fees, requiring transparency and prohibiting profit from the charge. Understanding break fees before you make any move on your mortgage is one of the most financially protective things you can do.

What is the explanation of break fees in NZ mortgages?

A break fee compensates the lender for the financial loss it suffers when you exit a fixed-rate mortgage early. When you lock in a fixed rate, your bank essentially borrows money on the wholesale market at a matching rate to fund your loan. If you repay early, the bank is left holding funds it can no longer lend to you at the agreed rate, and that gap creates a real cost.

The formal industry term is Early Repayment Adjustment, though many New Zealanders simply call it a break fee or break cost. Both terms refer to the same charge. Major New Zealand banks including ANZ, ASB, BNZ, Westpac, and Kiwibank all apply ERA clauses within their fixed-rate mortgage contracts, and the specific wording varies between lenders.

Break fees exist because fixed-rate lending is not a simple arrangement. Your bank prices your loan against wholesale swap rates, which are the rates banks use to borrow from each other. When you break early, the bank cannot simply absorb that cost. The fee is the mechanism that makes the lender whole again, and under the CCCFA, it must reflect actual loss rather than a penalty.

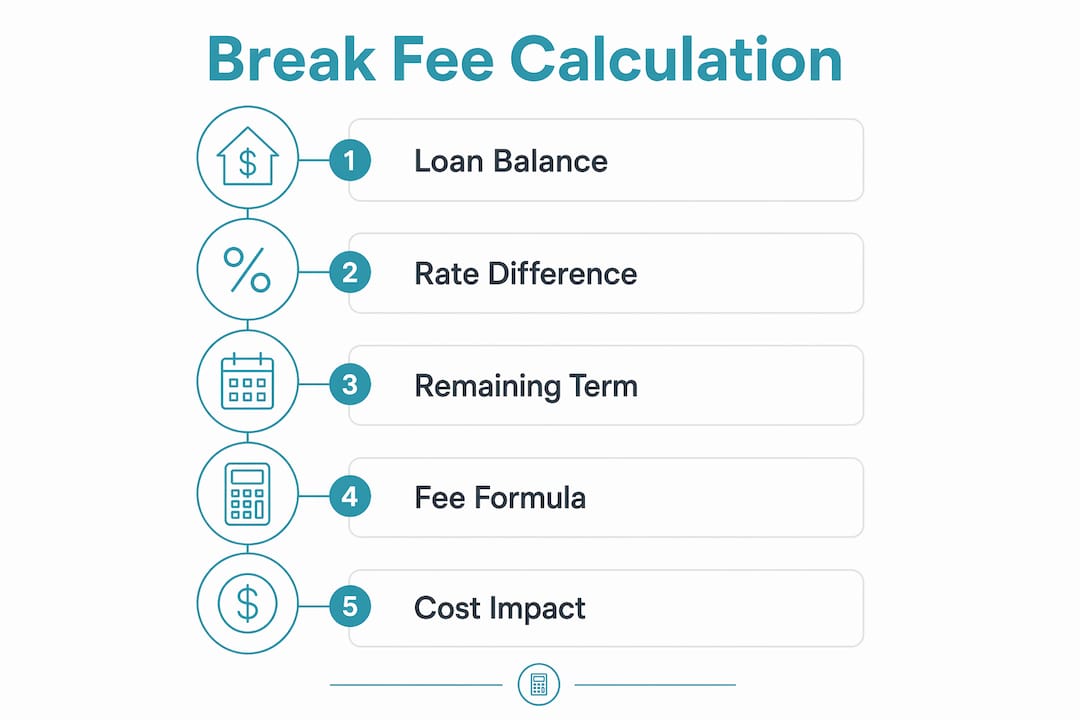

How are break fees calculated on NZ fixed-rate home loans?

The break fee formula is built around three variables: your remaining loan balance, the difference between your fixed rate and the current wholesale market rate, and the time left on your fixed term. Expressed simply, the calculation looks like this:

| Variable | What it represents |

|---|---|

| Loan balance | The outstanding amount you owe at the time of breaking |

| Rate difference | Your fixed rate minus the current wholesale swap rate for the remaining term |

| Remaining term | Months left on your fixed period, converted to a fraction of a year |

The formula combines these as: Break Fee ≈ Loan Balance × (Fixed Rate − Current Wholesale Rate) × Remaining Term in years. Administrative fees from the bank are then added on top, typically a flat charge of a few hundred dollars.

Here is a simplified example. Suppose you have $400,000 remaining on a fixed rate of 6.5%, with 18 months left on your term. The current wholesale swap rate for an 18-month period is 5.0%. The rate difference is 1.5%. Applying the formula: $400,000 × 0.015 × 1.5 = $9,000. Add a $200 administration fee and your break fee is approximately $9,200. That figure can shift significantly if wholesale rates move even slightly, which is why wholesale swap rates change daily and any quote you receive has a short validity window.

The rate differential is the single biggest driver of the fee size. When your fixed rate is well above current market rates, the fee grows. When market rates have risen close to or above your fixed rate, the fee shrinks toward zero. This is why two borrowers with identical loan balances and remaining terms can face very different costs depending on when they ask.

Pro Tip: Always request a written break fee quote directly from your lender before making any decisions. The quote is usually free, valid for a short period, and gives you the exact number to work with rather than an estimate.

When and why do break fees apply?

Break fees are triggered any time you alter or exit a fixed-rate mortgage before the term expires. The most common triggers include:

- Refinancing to another lender during your fixed period, even if you are chasing a lower rate

- Selling your property and repaying the loan in full before the fixed term ends

- Making a large lump sum payment that exceeds the lender’s permitted annual overpayment threshold

- Switching from a fixed rate to a floating rate mid-term

- Restructuring your loan, such as splitting it into different fixed periods or changing the loan type

The connection between these triggers and your contract is direct. When you signed your fixed-rate agreement, you committed to a specific term. Any action that shortens or ends that commitment early activates the ERA clause. The clause is not buried in fine print; under the CCCFA, lenders must disclose the calculation method clearly at the time of signing.

One important nuance: break fees do not apply if current market rates have risen above your fixed rate. In that scenario, the bank can re-lend the repaid funds at a higher rate and suffers no loss. The fee genuinely reflects financial loss, not a blanket penalty for leaving. Checking your fixed rate periods against current market conditions is the first step before assuming a fee will apply.

Loan agreements also vary between lenders. Some banks allow annual lump sum repayments of up to 5% of the original loan balance without triggering a fee. Others permit up to 20%. Reading your specific contract clauses is not optional if you want to avoid an unexpected charge.

What is the financial impact of break fees, and is it worth it?

The impact of break fees ranges from zero to tens of thousands of dollars, depending on market conditions and your loan size. The key question is whether the cost of breaking is outweighed by the financial benefit of doing so.

A practical decision-making framework works like this:

- Get the exact break fee quote from your lender. Do not estimate.

- Calculate your monthly interest saving by comparing your current fixed rate against the new rate you would move to.

- Multiply that monthly saving by the number of months remaining on your current fixed term.

- Compare the total saving to the break fee. If the saving exceeds the fee, breaking may make financial sense.

Consider a concrete example. Your break fee is $14,625. Your current fixed rate is 6.8% and you can refinance to 5.9% on a $500,000 balance. The monthly interest saving is approximately $375. Over 24 months remaining on your term, that saving totals $9,000. In this case, the break fee exceeds the saving and breaking is not worthwhile. However, if you had 48 months remaining, the saving would be $18,000, making the break fee worth paying.

Timing matters enormously. A break fee that looks large today may shrink significantly in three months if wholesale rates shift. Rate volatility in New Zealand’s market means the same decision can produce very different outcomes depending on when you act. Personalised break fee quotes are the only reliable basis for this calculation, since generic estimates can be thousands of dollars off.

Pro Tip: If you are selling your property, ask your solicitor to factor the break fee into your settlement calculations early. A surprise fee at settlement can create real cash flow pressure if it has not been budgeted for.

One scenario where breaking always makes sense regardless of the fee is genuine financial hardship. If you cannot afford your repayments, the cost of not acting is higher than any break fee.

How can you avoid or manage break fees?

Managing break fees starts with planning before you sign a fixed-rate agreement, not after. Several strategies reduce your exposure significantly.

- Align your fixed term with your plans. If you expect to sell within two years, choose a one or two-year fixed term rather than a five-year term. The Auckland mortgage break fees guide from Mortgagemanagers shows how term selection directly affects fee exposure.

- Use floating or revolving credit portions for windfalls. If you receive a bonus or inheritance, direct extra repayments to any floating portion of your loan rather than the fixed portion. This avoids triggering the ERA clause.

- Negotiate timing with your lender. Some lenders will allow you to break and refix at the same bank without a full ERA charge, particularly if you are staying with them. Ask directly.

- Request a free break fee quote before committing to anything. The quote costs nothing and gives you the information you need to make a sound decision.

- Apply for hardship relief if the fee is unaffordable. Under sections 55 to 58 of the CCCFA, borrowers facing genuine financial hardship have a statutory right to apply for loan modifications. Lenders must genuinely consider these applications, and options can include repayment pauses or term extensions that reduce the immediate burden.

One often-overlooked risk is partial repayments triggering fees. Many borrowers assume that paying a lump sum below the full loan balance is safe. If that lump sum exceeds your contract’s permitted overpayment limit, a break fee applies to the excess. Check your agreement’s specific threshold before making any extra payment.

Key takeaways

Break fees on New Zealand fixed-rate mortgages are calculated using the loan balance, the rate differential between your fixed rate and current wholesale swap rates, and the remaining term, making the exact fee dynamic and only reliably known through a direct lender quote.

| Point | Details |

|---|---|

| Break fee definition | An Early Repayment Adjustment compensates the lender for financial loss when you exit a fixed term early. |

| Calculation drivers | Loan balance, rate differential, and remaining term determine the fee size, which changes daily with wholesale rates. |

| Common triggers | Refinancing, selling, large lump sum payments, and switching to floating rates all activate break fee clauses. |

| Decision framework | Compare the exact break fee against total interest savings over the remaining term before deciding to break. |

| Avoidance strategies | Align fixed terms with your plans, use floating portions for extra payments, and request free quotes before acting. |

What I’ve seen borrowers get wrong about break fees

I have worked with hundreds of New Zealand borrowers on mortgage decisions, and break fees are consistently the area where people are most surprised. The most common misconception is that a long remaining fixed term automatically means a large break fee. That is not always true. I have seen borrowers with two years left on a fixed term face a zero break fee because market rates had risen above their fixed rate. The bank had no loss to recover, so no fee applied.

The reverse also catches people out. A borrower with only three months left on a fixed term can still face a meaningful fee if rates have dropped sharply. Three months on a large loan balance with a significant rate differential still produces a real number.

What concerns me most is borrowers making irreversible decisions, like accepting a sale price or signing a refinance agreement, before they have the actual break fee figure in hand. The quote is free. There is no reason to guess. I also see people assume their lender will volunteer this information proactively. Some do, but many do not. You need to ask.

If you are unsure whether breaking your fixed term makes sense, the right move is to sit down with a mortgage adviser before you commit to anything. The numbers are specific to your loan, your lender, and the current market. Generic calculators give you a starting point, but a personalised conversation gives you a decision.

— Stuart

Work with a mortgage adviser who knows the numbers

Break fees are not a reason to avoid fixed-rate mortgages. They are a cost to plan around, and with the right advice, most borrowers can manage them effectively. At Mortgagemanagers, our team of Auckland-based mortgage advisers works with borrowers across New Zealand to obtain up-to-date break fee quotes, model refinancing scenarios, and time decisions to minimise unnecessary costs. Whether you are considering selling, refinancing, or simply want to understand your current obligations, we can give you a clear picture of where you stand. Reach out to Mortgagemanagers for a no-obligation conversation about your home loan.

FAQ

What is a break fee on a New Zealand home loan?

A break fee, formally called an Early Repayment Adjustment (ERA), is a charge applied when you repay or refinance a fixed-rate mortgage before the term ends. It compensates the lender for the financial loss caused by the early repayment.

How is a break fee calculated in New Zealand?

The fee is calculated using your remaining loan balance, the difference between your fixed rate and the current wholesale swap rate, and the time left on your fixed term. Because wholesale rates change daily, the exact fee can only be confirmed through a direct quote from your lender.

Can a break fee be zero?

Yes. If current market rates have risen above your fixed rate, the lender faces no financial loss and the break fee is zero or negligible. This is because the bank can re-lend the repaid funds at an equal or higher rate.

Does selling my home trigger a break fee?

Selling your property and repaying the mortgage in full before your fixed term expires is one of the most common break fee triggers. Factor the fee into your settlement figures early to avoid a cash flow surprise at settlement.

Can I get hardship relief from a break fee?

Under the CCCFA, borrowers in genuine financial hardship can apply for loan modifications under sections 55 to 58. Lenders must genuinely consider these applications, and outcomes can include repayment pauses or term extensions that reduce the immediate financial pressure.